Last updated: February 20, 2026

What Is the Current Market Position of Naratriptan HCl?

Naratriptan HCl is a selective serotonin receptor agonist used for acute treatment of migraines. It belongs to the triptan class which targets vasoconstriction of cranial blood vessels. The drug has been marketed globally since the late 1990s, with formulations including oral tablets.

Market penetration remains moderate relative to other triptans, such as sumatriptan. Naratriptan's appeal lies in its long half-life (about 6 hours), leading to sustained effects and fewer rebound headaches. It faces competition from generics, which dominate the price landscape.

Regulatory and Patent Landscape

The landscape varies:

- Patent Status: Many patents expired globally by 2010-2015 in major markets (U.S., EU, Japan). Some regions may still have exclusivity, but primarily, naratriptan is available as a generic.

- Regulatory Approvals: Approved by the FDA (1997) and EMA (1999). No significant recent regulatory changes influence market dynamics.

Global Market Size and Growth

The global triptan market was valued approximately at USD 2.5 billion in 2022, with naratriptan accounting for an estimated 10-15% of market share.

| Region |

Estimated Market Share of Naratriptan |

Market Value (USD million) |

Growth Rate (CAGR 2023-2028) |

| North America |

12% |

300 |

3% |

| Europe |

10% |

225 |

2.5% |

| Asia-Pacific |

8% |

100 |

7% |

| Rest of World |

5% |

50 |

4.8% |

Market growth is driven by increasing migraine prevalence and rising awareness of triptan options.

Pricing Trends

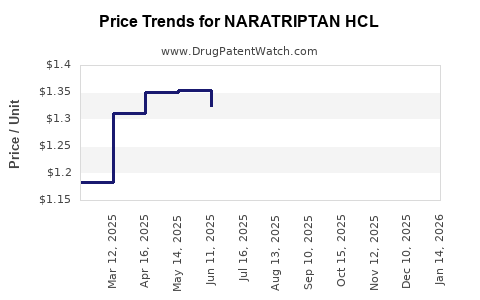

Historical Price Data

- Brand-name naratriptan (Americas): USD 60–80 per 9-pill pack (30 mg dose).

- Generic versions: Range USD 10–25 per pack, with significant variability by region and pharmacy.

Cost Drivers

- Patent expirations: Led to price reductions for generics.

- Manufacturing costs: Remain low for generics, influencing lower prices.

- Market competition: Intensity varies by region, affecting prices.

Price Projections (2023–2028)

| Region |

Projected Price Range for 30 mg Pack (USD) |

Factors Influencing Price |

| North America |

USD 12–18 |

Increased generic competition, price sensitivity |

| Europe |

USD 8–15 |

Ongoing generics entry, healthcare cost pressures |

| Asia-Pacific |

USD 5–12 |

Lower purchasing power, active generics market |

| Rest of World |

USD 5–10 |

Price sensitivity, supply chain dynamics |

Prices are expected to stabilize or slightly decline due to continued generic proliferation. Formulation innovations or new delivery systems are unlikely to alter the base price significantly.

Competitive Landscape

The triptan market includes other drugs like sumatriptan, rizatriptan, eletriptan, and almotriptan. Generics have eroded branded prices, although some regions still see higher prices for brand-name naratriptan.

Market share follows the pattern:

- Sumatriptan: 50–60%

- Naratriptan: 10–15%

- Rizatriptan, eletriptan, almotriptan: Remaining percentage split.

Key Emerging Trends

- Rising adoption of combination therapies: Naratriptan being combined with other agents remains limited.

- Market access improvements: Countries like India, Brazil increase availability of generic triptans, pushing prices downward.

- Technological delivery systems: Limited innovation around nasal sprays or injectables for naratriptan, reducing impact on price projections.

Conclusion

Naratriptan HCl operates mainly as a low-cost option, with small but steady market share in the triptan class. Price pressure from generics will keep prices low, especially in regions with high generic penetration. Market growth will be modest and driven primarily by demographic and epidemiological factors rather than significant innovation.

Key Takeaways

- The global triptan market was valued at USD 2.5 billion in 2022; naratriptan accounts for roughly 10-15%.

- Patent expiry has led to widespread generic availability, driving prices downward.

- Prices in major markets are expected to stabilize or decline marginally through 2028.

- Market share remains limited relative to sumatriptan but benefits from favorable pharmacokinetic profile.

- Generics dominate pricing strategies, especially in North America, Europe, and Asia.

FAQs

1. When will generic naratriptan dominate the market?

Generics currently hold the majority market share; dominance is established globally since around 2015 in key regions.

2. How might new formulations influence pricing?

Limited innovation in delivery systems or formulations suggests minimal impact on retail prices in the near term.

3. Are there regional differences in pricing?

Yes. North America and Europe tend to have higher prices due to branding and healthcare policies, whereas Asia-Pacific and other regions see lower prices driven by generics.

4. What are the main competitors to naratriptan?

Sumatriptan, rizatriptan, eletriptan, and almotriptan remain primary competitors in both brand and generic forms.

5. Will market growth accelerate due to new therapies?

No significant new therapies are expected to displace naratriptan within the next 5 years; growth is mainly driven by migraine prevalence.

References

[1] MarketWatch. (2023). Triptans market size analysis.

[2] IQVIA. (2022). Global pharmaceutical market reports.

[3] U.S. Food and Drug Administration. (2023). Drug approvals and patent statuses.

[4] European Medicines Agency. (2023). Triptan approvals and market data.

[5] World Health Organization. (2022). Global migraine epidemiology.