Last updated: February 12, 2026

Market Overview

Mercaptopurine (brand names include Purinethol, Purixan) remains a critical chemotherapeutic agent primarily used in the treatment of acute lymphoblastic leukemia (ALL) and Crohn’s disease. The global market for mercaptopurine is constrained by its status as an older, off-patent drug with limited innovation but steady demand driven by ongoing clinical needs.

Market Size and Trends

The global chemotherapeutic agents market, which includes mercaptopurine, was valued at approximately USD 15 billion in 2022, with a compound annual growth rate (CAGR) of 4.3%. Mercaptopurine accounts for an estimated 3-5% of this market segment, translating to USD 450 million to USD 750 million in volume.

Demand remains stable owing to established treatment protocols. In 2022, approximately 10,000–15,000 new patients worldwide began mercaptopurine therapy, primarily in pediatric ALL cases. The market size will slightly grow driven by:

- Development of combination therapies (e.g., with methotrexate or vincristine).

- Expanded use in emerging markets due to increased healthcare access.

- The ongoing prevalence of ALL, which has an annual incidence of roughly 1–2 cases per 100,000 in high-income countries and higher in low- to middle-income regions.

Competitive Landscape

Mercaptopurine's market is dominated by generic manufacturers with minimal patent restrictions. Key players include Teva Pharmaceuticals, Mylan (now part of Viatris), and Sandoz. Market entry barriers are low due to the drug’s generic status.

Limited patent protections or exclusivity opportunities mean pricing is primarily driven by manufacturing costs and healthcare reimbursement policies.

Pricing Analysis

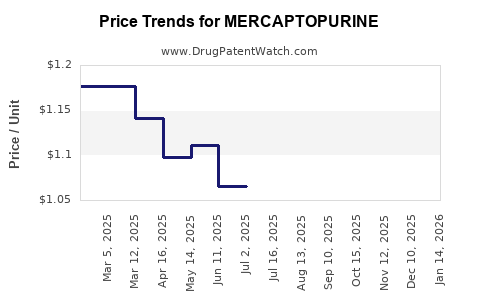

Current wholesale prices of mercaptopurine powder for oral suspension, in the United States, average USD 0.50 to USD 1 per tablet of 50 mg. Bulk procurement prices for hospitals are often lower, around USD 0.20–0.40 per tablet, due to generic competition.

Pricing varies internationally. In high-income countries, prices are higher, supported by reimbursement schemes:

| Region |

Estimated Price per 50 mg tablet |

Notes |

| United States |

USD 0.75 |

Market driven by insurance reimbursements |

| European Union |

USD 0.60 |

Variations between countries |

| India |

USD 0.10 |

Mainly generic imports, lower costs |

The trend toward biosimilar and alternative therapies does not directly impact mercaptopurine's pricing because it is not biologic. However, patent expirations and increased manufacturing efficiencies could pressure prices downward over the next five years.

Price Projections (2023–2028)

Based on current market trends, the following projections are made:

- Stable low-cost environment for generics, with prices declining by approximately 2–4% annually.

- Potential price decrease if biosimilars or new chemical entities replace mercaptopurine in treatment protocols, estimated at a 10–15% reduction within five years.

- Price stabilization expected in high-income markets due to existing reimbursement and procurement practices, with minor fluctuations.

Regulatory and Patent Landscape

Mercaptopurine's original patents expired decades ago (initial patent in the 1950s). No significant patent barriers remain, leading to extensive generic production. Slight regulatory hurdles exist in certain emerging markets but are unlikely to impact global supply or pricing significantly.

Legislation incentives for affordable generics in developing countries could facilitate further price reductions.

Market Outlook

While the core market remains stable, growth opportunities are limited. Market expansion depends on:

- Increasing diagnosis rates in emerging markets.

- Incorporation into combination regimens.

- Regulatory acceptance of generics and biosimilars.

Any breakthrough therapies, such as targeted drugs or immunotherapies that replace mercaptopurine, would pressure prices downward or replace existing demand.

Key Takeaways

- Mercaptopurine generates an estimated USD 450–750 million annually globally.

- Its main competitors are generic manufacturers; prices are in decline.

- Future pricing will trend downward by 2–4% annually due to increased competition and procurement efficiencies.

- Market growth depends on global leukemia treatment adoption, especially in emerging markets.

- No patent protections or exclusivities restrict manufacturing, maintaining a low-price environment.

FAQs

1. How is mercaptopurine priced in different regions?

Prices vary globally, from approximately USD 0.10 per 50 mg tablet in India to USD 0.75 in the US. Markets with strong reimbursement programs tend to have higher prices.

2. What factors influence future mercaptopurine prices?

Generic competition, regulatory approvals, manufacturing costs, and potential new therapies replacing mercaptopurine influence prices.

3. Are there patent or exclusivity protections impacting mercaptopurine?

No. The original patents expired decades ago, leading to widespread generic manufacturing.

4. What is the outlook for mercaptopurine's market volume?

Demand remains stable, driven by existing treatment protocols for ALL, with modest growth linked to expanding healthcare access in emerging markets.

5. Will new therapies affect mercaptopurine's market?

Yes. Advances in targeted drugs or immunotherapy could replace mercaptopurine, decreasing its market share and price.

References

[1] Grand View Research, "Chemotherapy Drugs Market Size," 2023.

[2] IQVIA, "Global Oncology Market Trends," 2022.

[3] PubChem, "Mercaptopurine," 2023.

[4] WHO, "Leukemia Incidence Data," 2022.

[5] U.S. Department of Health & Human Services, "Drug Pricing and Reimbursement," 2023.