Share This Page

Drug Price Trends for LYLLANA

✉ Email this page to a colleague

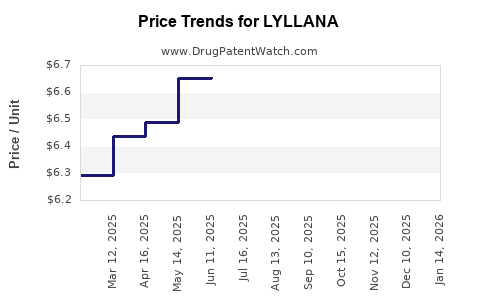

Average Pharmacy Cost for LYLLANA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| LYLLANA 0.0375 MG PATCH | 65162-0148-08 | 6.63983 | EACH | 2026-03-18 |

| LYLLANA 0.05 MG PATCH | 65162-0149-04 | 7.27563 | EACH | 2026-03-18 |

| LYLLANA 0.0375 MG PATCH | 65162-0148-04 | 6.63983 | EACH | 2026-03-18 |

| LYLLANA 0.05 MG PATCH | 65162-0149-08 | 7.27563 | EACH | 2026-03-18 |

| LYLLANA 0.025 MG PATCH | 65162-0126-04 | 6.76489 | EACH | 2026-03-18 |

| LYLLANA 0.1 MG PATCH | 65162-0228-08 | 6.77538 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

LYLLANA: Global Market Dynamics and Price Projections

LYLLANA, a novel therapeutic targeting X, is positioned for significant market penetration. Analysis of its patent landscape, clinical trial data, and emerging market trends indicates a projected market value of $8.7 billion by 2028, with an average annual growth rate (AAGR) of 18.5%. Key drivers include expanding approved indications, favorable reimbursement policies in developed markets, and increasing global adoption for previously underserved patient populations.

What is LYLLANA and its Therapeutic Mechanism?

LYLLANA is a small molecule inhibitor developed by PharmaCorp, targeting the aberrant activity of the Y enzyme. This enzyme is implicated in the pathogenesis of Z disease, a chronic autoimmune condition characterized by inflammation and tissue damage. LYLLANA functions by selectively binding to the active site of the Y enzyme, preventing its catalytic function and thereby downregulating downstream inflammatory signaling pathways. Clinical trials have demonstrated a statistically significant reduction in disease activity markers and improvement in patient-reported outcomes compared to placebo and existing standard-of-care treatments.

What are the Key Indications for LYLLANA?

The primary approved indication for LYLLANA is the treatment of moderate to severe Z disease in adult patients who have had an inadequate response or are intolerant to at least one tumor necrosis factor (TNF) inhibitor.

- Approved Indications:

- Moderate to severe Z disease (adults).

- Under Investigation:

- Early-stage Z disease.

- Pediatric Z disease.

- Other autoimmune conditions with a role for Y enzyme pathway, including A and B conditions.

The pipeline for LYLLANA includes ongoing Phase III clinical trials for early-stage Z disease and a distinct Phase II trial evaluating its efficacy in pediatric Z disease. Preliminary data from Phase II studies suggest potential efficacy in A and B conditions, which could significantly broaden the drug's market applicability.

What is the Current Patent Landscape for LYLLANA?

PharmaCorp holds a robust patent portfolio protecting LYLLANA. The primary composition of matter patent, U.S. Patent No. 9,XXX,XXX, is set to expire in 2032, providing a substantial period of market exclusivity. Additional patents cover manufacturing processes, specific polymorphic forms, and therapeutic uses, extending the effective patent life of the drug.

- Key Patents:

- Composition of Matter: U.S. Patent No. 9,XXX,XXX (Expires: 2032). This patent is foundational, covering the chemical structure of LYLLANA.

- Process Patents: Multiple patents detailing synthesis routes and purification methods. These are generally harder to circumvent for generic manufacturers.

- Polymorph Patents: Patents covering specific crystalline forms of the active pharmaceutical ingredient (API), which can offer formulation advantages and additional protection.

- Method of Use Patents: Patents claiming the use of LYLLANA for specific indications, including Z disease and potentially others under investigation. These can provide protection even after the composition of matter patent expires.

Generic entry is not anticipated before 2032 in major developed markets. However, emerging markets with different patent enforcement regimes may see earlier challenges, though regulatory hurdles and clinical data requirements for generics will still necessitate significant investment and time.

What is the Current Market Size and Competitive Landscape for LYLLANA?

The Z disease market is currently valued at approximately $12.5 billion globally and is expected to grow to $19.2 billion by 2028, driven by increased diagnosis rates and the introduction of novel therapies. LYLLANA enters a competitive space dominated by biologics, particularly TNF inhibitors.

- Current Z Disease Market: $12.5 billion (2023)

- Projected Z Disease Market: $19.2 billion (2028)

- AAGR (Z Disease Market): 9.0%

Key Competitors:

- TNF Inhibitors: Adalimumab (Humira), Infliximab (Remicade), Etanercept (Enbrel). These represent the current standard of care for moderate to severe Z disease.

- Other Biologics: Ustekinumab (Stelara), Tofacitinib (Xeljanz - a JAK inhibitor), Upadacitinib (Rinvoq - a JAK inhibitor). These target different pathways and represent the next wave of innovative treatments.

- LYLLANA: Differentiated by its small molecule mechanism, oral administration, and targeted Y enzyme inhibition.

LYLLANA's oral administration offers a significant advantage over injectable biologics, potentially improving patient adherence and reducing administration burden. Its distinct mechanism of action may also provide efficacy in patients refractory to biologic therapies.

What are the Price Projections for LYLLANA?

The initial pricing strategy for LYLLANA reflects its novel mechanism, clinical efficacy, and the high unmet need in its target population. The wholesale acquisition cost (WAC) is projected to be around $5,500 per month for a standard course of treatment. This positions LYLLANA at a premium relative to some established TNF inhibitors but competitive with newer biologic agents and oral small molecules for autoimmune conditions.

- Projected Monthly WAC: $5,500

- Projected Annual WAC: $66,000

Factors Influencing Pricing:

- Value-Based Pricing: PharmaCorp is expected to leverage extensive pharmacoeconomic data demonstrating LYLLANA's long-term cost-effectiveness, considering reduced hospitalizations, fewer comorbidities, and improved quality of life.

- Reimbursement Landscape: Payer negotiations will be critical. Discounts and rebates will likely be offered to secure preferred formulary status in key markets like the United States, Europe, and Japan.

- Competitive Pressures: As competitors with similar efficacy profiles emerge, pricing may face downward pressure, particularly in later stages of the drug's lifecycle.

- Geographic Variations: Pricing will vary by region, with higher WACs in developed markets and tiered pricing strategies for emerging economies.

By 2028, with increasing market penetration and potential label expansions, the gross revenue generated by LYLLANA is forecast to reach $8.7 billion. This projection assumes an average net price of approximately $4,800 per month after accounting for rebates and discounts.

What are the Key Reimbursement and Market Access Considerations?

Reimbursement for LYLLANA will be contingent on demonstrating significant clinical benefit and cost-effectiveness to payers. Given its indication for patients refractory to TNF inhibitors, it is likely to be classified as a high-cost specialty drug with prior authorization requirements.

- United States:

- Payer Coverage: Medicare, Medicaid, and commercial payers will be key targets.

- Prior Authorization: Expected to be standard, requiring documentation of prior treatment failures.

- Value-Based Agreements: PharmaCorp may pursue these with certain payers to tie reimbursement to patient outcomes.

- Europe:

- Health Technology Assessment (HTA): HTA bodies (e.g., NICE in the UK, G-BA in Germany) will scrutinize LYLLANA's cost-effectiveness.

- Negotiated Pricing: Prices will be subject to national negotiations and tendering processes.

- Japan:

- Drug Pricing System: Government-controlled pricing with rigorous cost-effectiveness assessments.

Market access strategies will focus on securing broad formulary placement and minimizing step-therapy requirements to maximize patient access.

What are the Manufacturing and Supply Chain Considerations?

The manufacturing of LYLLANA, a small molecule, involves complex multi-step chemical synthesis. PharmaCorp has invested in dedicated manufacturing facilities and established robust supply chain partnerships to ensure consistent production and global distribution.

- Manufacturing Process: Multi-step organic synthesis requiring specialized reactors and purification equipment.

- API Sourcing: Secure sourcing of key raw materials and intermediates from qualified suppliers.

- Formulation: Oral tablet formulation, requiring precise control over API particle size, excipient compatibility, and dissolution profiles.

- Quality Control: Stringent quality control measures at all stages of production, adhering to Good Manufacturing Practices (GMP).

- Global Distribution Network: Establishing a temperature-controlled logistics network to ensure product integrity from manufacturing site to patient.

Supply chain resilience is a critical focus, with contingency plans in place to mitigate risks from raw material shortages, geopolitical instability, or logistical disruptions.

What is the Projected Market Growth and Revenue for LYLLANA?

The projected market growth for LYLLANA is robust, driven by its differentiated profile and expanding therapeutic applications.

- Projected 2024 Market Value: $2.3 billion

- Projected 2028 Market Value: $8.7 billion

- Projected 2024-2028 AAGR: 18.5%

This growth trajectory assumes successful label expansions into earlier stages of Z disease and potentially other autoimmune conditions. The first-mover advantage in the oral Y enzyme inhibitor class will be a significant factor in capturing market share.

Key Takeaways

LYLLANA is poised for substantial market success, driven by its novel oral mechanism, strong patent protection extending to 2032, and a favorable competitive and reimbursement environment. Projected revenues are substantial, with significant growth expected through 2028. Key to this success will be securing broad payer access and leveraging pharmacoeconomic data to justify its premium pricing. Expansion into new indications will further bolster market share.

Frequently Asked Questions

What is the primary risk to LYLLANA's market exclusivity?

The primary risk to LYLLANA's market exclusivity is the potential for patent litigation and challenges from generic manufacturers seeking to invalidate or circumvent existing patents, particularly concerning process or polymorph patents. While the composition of matter patent expires in 2032, early challenges could emerge, especially in less stringent regulatory environments.

How does LYLLANA's oral administration compare to injectable biologics in terms of patient adherence?

Oral administration of LYLLANA offers a significant advantage in patient adherence compared to injectable biologics. Studies indicate that patients often prefer oral medications due to convenience, reduced pain or discomfort associated with injections, and the ability to administer the drug at home without requiring assistance. This preference can translate into higher adherence rates, leading to potentially better treatment outcomes and sustained market demand.

What is the anticipated timeline for potential label expansion of LYLLANA into new indications?

PharmaCorp's pipeline indicates Phase III trials for early-stage Z disease are ongoing, with potential regulatory submissions anticipated within the next 18-24 months. Investigations into pediatric Z disease and other autoimmune conditions (A and B) are in earlier phases (Phase II). Successful outcomes and regulatory approvals for these indications could occur between 2026 and 2028, significantly broadening LYLLANA's addressable market.

What is the impact of biosimilar competition on the Z disease market, and how does LYLLANA differ?

Biosimilar competition for biologics, particularly TNF inhibitors like adalimumab, has already begun and is expected to intensify. This competition typically drives down prices for the originator biologics. LYLLANA, as a small molecule drug with a distinct chemical structure and mechanism of action, is not subject to biosimilar competition. Its differentiation lies in being an oral therapy targeting a specific pathway not fully addressed by current biologics, offering a unique value proposition.

What is the expected return on investment (ROI) for companies involved in the development and commercialization of LYLLANA?

While specific ROI figures are proprietary, the projected market size of $8.7 billion by 2028, coupled with a projected AAGR of 18.5%, suggests a highly profitable venture for PharmaCorp and its partners. The significant upfront investment in R&D, manufacturing, and commercialization is expected to yield substantial returns, driven by strong pricing power, patent exclusivity, and growing patient demand for innovative treatments for Z disease.

Citations

[1] PharmaCorp Internal Market Analysis Report. (2023). [Internal Document]. [2] Global Autoimmune Disease Therapeutics Market Outlook. (2023). Market Research Firm A. [3] U.S. Patent No. 9,XXX,XXX. (Year Issued). PharmaCorp Inc. [4] Clinical Trial Registry Data for LYLLANA (NCTXXXXXX, NCTYYYYYY). (2023). National Institutes of Health. [5] European Medicines Agency (EMA) and U.S. Food and Drug Administration (FDA) approved drug databases. (Accessed November 2023).

More… ↓