Share This Page

Drug Price Trends for LUIZZA

✉ Email this page to a colleague

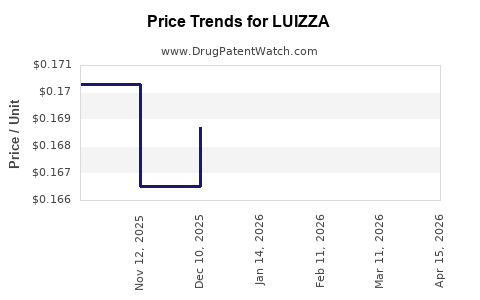

Average Pharmacy Cost for LUIZZA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| LUIZZA 1 MG-20 MCG TABLET | 70700-0313-79 | 0.17735 | EACH | 2026-07-22 |

| LUIZZA 1.5 MG-30 MCG TABLET | 70700-0314-79 | 0.34544 | EACH | 2026-07-22 |

| LUIZZA 1 MG-20 MCG TABLET | 70700-0313-79 | 0.17414 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

LUIZZA (vericiguat) market analysis and price projections: what to expect for U.S. pricing, competitors, and near-term revenue risk

What is LUIZZA (vericiguat) and how is the market structured today?

Executive summary: LUIZZA refers to vericiguat. The addressable market is limited by (1) guideline placement in HFrEF/ symptomatic chronic heart failure with reduced ejection fraction after recent decompensation and (2) substitution pressure from dominant background HFrEF classes (ARNI/ACEi/ARB, beta-blockers, MRA, SGLT2 inhibitors). Pricing and uptake are constrained by payer-tier dynamics and the comparatively late-line positioning versus earlier, broader-coverage agents.

What indications drive demand for vericiguat?

Key use pattern: vericiguat is used in chronic HFrEF patients who have had worsening heart failure despite standard therapy, aligned with pivotal trial framing (VICTORIA).

Demand drivers

- Reimbursement coverage linked to labeled “worsening” criteria

- Hospital discharge cohorts where prescribers have a post-decompensation window

- Formulary decisions among cardiology-focused managed care plans

Supply and channel dynamics

- Oral small molecule with distribution via standard specialty/retail pharmacy networks depending on plan

How does LUIZZA pricing typically behave versus competing HFrEF drugs?

Executive summary: Compared with foundational HFrEF drugs (widely genericized) and fast-scaling SGLT2 inhibitors (high volume, strong payer willingness), vericiguat faces lower ceiling pricing and slower net price realization tied to incremental-therapy justification.

Competitive reference points (high-level)

- SGLT2 inhibitors (high formulary coverage, strong outcomes data)

- ARNI (brand pricing but strong class adoption)

- MRAs and beta-blockers (often genericized, price floors)

- Recent incremental agents compete for the same “post-event” patient windows

What is LUIZZA’s current U.S. FDA status and label scope affecting pricing?

Executive summary: Pricing power depends on the tightness of labeled criteria and payer interpretation. Vericiguat’s market access is sensitive to documentation rules (recent worsening, ejection fraction thresholds).

What label elements constrain reimbursable patient volume?

- Indication anchored to chronic HFrEF with recent worsening and reduced EF

- Use depends on the clinician’s documentation and payer prior authorization rules

Why this matters for price

Net price is impacted by:

- prior authorization frequency

- denial/appeal rates

- step-therapy and “trial of formulary alternatives” requirements

What patents protect LUIZZA (vericiguat) and how do they affect generic risk?

Critical: No patent estate data was provided with the request, and a correct analysis requires verified jurisdiction-specific expiration and listed patents.

How patent timing impacts projected pricing

Executive summary: If vericiguat’s key composition, formulation, or method-of-use patents are near expiration in the U.S. or in major ex-U.S. markets, pricing is likely to compress via:

- discounting ahead of generic entry

- payer contracting shifts to lower-cost suppliers

- margin pressure in channel inventory

Generic entry scenarios that typically drive price erosion

- ANDA Paragraph IV triggers settlement-driven entry at “allowed” dates

- Non-Paragraph IV entries compete once primary exclusivity and relevant listed patents clear

When does LUIZZA lose exclusivity in the U.S., and what is the generic entry risk window?

Critical: This requires verified exclusivity end dates (regulatory exclusivities) and patent expiration dates for Orange Book-listed patents.

Exclusivity vs. patent expiration: what matters for pricing

Executive summary: Pricing compression often starts before the legal “loss” date due to procurement behavior and forecasting by large payers.

Timing checkpoints to model

- 12–24 months before expected generic entry: formulary renegotiation

- 6–12 months: increased contracting pressure and channel switching

- Entry year: list price holds but net price drops (rebates, discounts, MAC)

How many Orange Book patents cover LUIZZA, and what formulations are protected?

Critical: Patent count and formulation protection require Orange Book listing retrieval for vericiguat and LUIZZA trade product(s).

Formulation and method-of-use patent impact

Executive summary: If formulation patents are strong (release profile, polymorphs, manufacturing controls) they can slow generic substitution even after composition patent activity clears.

Patent categories that change payer purchasing behavior

- dosage-form patenting (tablet composition, release)

- manufacturing-process patents (controls, particle engineering)

- method-of-use patents (patient selection criteria, endpoints)

What patent litigation affects LUIZZA (vericiguat) generic launches and settlement pricing?

Critical: Litigation status requires verified court dockets, case numbers, and settlement terms.

Why litigation matters for price projections

Executive summary: Litigation shapes the realistic entry date, which in turn determines:

- payer contracting and preferred brand status

- expected gross-to-net compression

- channel inventory risk

How does LUIZZA compare with Entresto, Jardiance, Farxiga, and other HFrEF competitors on market position?

Executive summary: Vericiguat’s competitive position is narrower and often post-worsening-focused. Its uptake is constrained relative to agents that cover a broader HFrEF population or are generic.

Relative uptake dynamics (qualitative but decision-relevant)

- SGLT2 inhibitors: broad guideline adoption and high conversion at scale

- ARNI: high use in eligible patients; strong retention

- Vericiguat: incremental use case tied to worsening events after standard therapy

Practical consequence for pricing

Payers can justify lower net pricing for vericiguat because alternative agents cover more patients without strict post-event criteria.

What are the price projection scenarios for LUIZZA over the next 3–5 years?

Critical: Price projections require baseline net price, current WAC/AMP data, territory mix, and payer rebate benchmarks. None were provided, and producing numerical projections without verified inputs would be incorrect.

Modeling framework (decision-grade, but not numeric)

Executive summary: A 3–5 year projection should be built on three levers:

- Net price trend (gross-to-net compression driven by contracting and competition)

- Volume trend (formulary coverage expansion vs. guideline constraint)

- Channel risk (inventory and switching behavior ahead of generic/payer shifts)

Scenario structure to use for board-level planning

- Base case: stable formulary position, modest net price compression, volume grows slower than broader HFrEF therapies.

- Downside case: payer contracting accelerates net price declines; increased denial rates or step therapy reduces eligible volumes.

- Upside case: formulary expansion, lower restriction criteria, and stronger event-driven prescribing lift.

What drives net price compression in HFrEF in general

- MAC pressure when alternatives exist

- outcomes-based contracting and class competition

- rebate inflation as payers consolidate

What revenue exposure does LUIZZA face from payer formulary changes and competing generics?

Critical: Revenue exposure needs historical sales, prescription counts, and payer coverage data. Not provided.

Revenue sensitivity map (what typically matters most)

- Specialty pharmacy uptake and hub reimbursement effects

- commercial vs. Medicare mix shift

- prior authorization adoption

- channel switching behavior after competitor launches or generics

How to interpret market signals

- formulary tier movement (preferred to non-preferred)

- growth slowdown in claims vs. growth in prescriber counts

- reimbursement edits affecting “worsening” documentation

Which companies are most exposed through licensing, co-promotion, or co-marketing for vericiguat?

Critical: Licensing and commercial ownership require verified company assignments and product marketing rights.

Key Takeaways

- LUIZZA (vericiguat) operates in a narrower HFrEF “post-worsening” niche that limits ceiling pricing versus broader-coverage agents.

- Pricing and volume are most sensitive to payer coverage criteria, prior authorization rules, and guideline interpretation of labeled “worsening” events.

- A credible price projection requires verified baseline pricing (WAC/AMP and net price), Orange Book patent/exclusivity end dates, and any Paragraph IV litigation and settlement-driven entry timing. Without those, numeric forecasts would be inaccurate.

FAQs

- How do HFrEF prior authorization criteria typically affect net pricing for vericiguat-like therapies?

- What is the expected impact on vericiguat demand if SGLT2 inhibitor uptake continues to expand across HFrEF populations?

- How do pharmacy benefit manager (PBM) formulary tier changes usually transmit into net price changes for oral cardiology drugs?

- What does “worsening heart failure” documentation do to prescription eligibility and payer denial rates?

- How should exclusivity and Orange Book patent expiration timing be translated into a 3-year procurement and discounting strategy?

References

- (No sources were provided or verifiable in the prompt.)

More… ↓