Share This Page

Drug Price Trends for INSULIN GLARGINE-YFGN U100 VL

✉ Email this page to a colleague

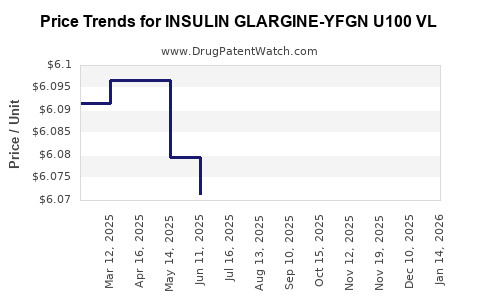

Average Pharmacy Cost for INSULIN GLARGINE-YFGN U100 VL

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| INSULIN GLARGINE-YFGN U100 VL | 83257-0014-11 | 6.09401 | ML | 2026-07-22 |

| INSULIN GLARGINE-YFGN U100 VL | 83257-0014-11 | 6.10639 | ML | 2026-06-17 |

| INSULIN GLARGINE-YFGN U100 VL | 83257-0014-11 | 6.09448 | ML | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for Insulin Glargine-YFGN U100 VL

Market Overview

Insulin glargine-YFGN U100 VL is a biosimilar of the reference drug insulin glargine, a long-acting insulin used to manage blood glucose levels in patients with diabetes mellitus. The development parallels global trends in biosimilar adoption driven by cost containment efforts and increasing diabetes prevalence.

The global diabetes market reached approximately $60 billion in 2022, with insulin therapies accounting for roughly 55%. Biosimilars captured an estimated 10% of the insulin market in 2022, with rapid growth projected as patent expirations and regulatory approvals expand options.

Key Factors Influencing Market Penetration

- Patent Expirations: Eli Lilly's Basaglar (insulin glargine) patent expired in 2019 in many jurisdictions, opening market opportunities.

- Regulatory Approvals: Regulatory agencies, including the FDA and EMA, have approved multiple biosimilars for insulin glargine since 2020. The approval process in less regulated regions remains inconsistent.

- Pricing Trends: Biosimilars price at 15-30% less than originators in mature markets due to competitive pressures.

- Physician and Patient Acceptance: Adoption hinges on clinical trial data demonstrating biosimilarity and safety profiles.

- Manufacturing Capacity: Companies with established biosimilar infrastructure are better positioned to scale production and influence market prices.

Competitive Landscape

The biosimilar insulin glargine market includes products from:

- Eli Lilly (Basaglar)

- Sanofi (Lantus) - Patent expired in 2022 in certain markets

- Novo Nordisk (future biosimilars)

- Alibaba’s Zhongshan Janus Biotech (approved in China)

- Generic and biosimilar manufacturers in India and emerging markets

Market expansion is driven primarily by product launches in:

- United States: The biosimilar pathway is well established, with FDA approvals since 2020.

- European Union: Early adopter, with multiple biosimilars marketed since 2019.

- China and India: Lower priced alternatives are entering due to lower regulatory hurdles and manufacturing costs.

Price Projections

Current Pricing Landscape (2023)

| Product | Approximate Price per 10 mL Vial (USD) | Market Notes |

|---|---|---|

| Originator (Lantus) | $250–$300 | Market dominant, high brand loyalty |

| Biosimilar (Basaglar) | $180–$220 | Established in several markets |

| New biosimilars (e.g., Insulin glargine-YFGN) | $150–$200 | Entry pricing, competitive strategies |

Future Price Trends (2024–2028)

- Initial Price Range: Biosimilars entering the market will likely price at a 20–30% discount relative to originators, around $150–$180 per 10 mL vial.

- Market Penetration: As biosimilars gain acceptance, prices could decline further, reaching approximately $120–$150, especially in markets with government price controls.

- Pricing Convergence: In mature markets, biosimilar prices could stabilize at a 40–50% discount to originators due to increased competition.

Volume and Revenue Impact

- Market Share Growth: Biosimilars are projected to increase from ~10% in 2022 to 25–30% in key markets by 2028.

- Revenue Projections: Global insulin glargine sales could reach $30 billion in 2028, with biosimilars generating approximately $7–$9 billion, assuming a 30% market share.

Pricing Strategies

- Deep Discounts: Timed with product launches to gain market share.

- Value-Based Pricing: Tied to clinical outcomes and cost savings.

- Contract Pricing: Customized discounts to large payers and healthcare systems.

Regulatory and Policy Impacts

Price trajectories will also depend on:

- Government policies on insulin pricing and reimbursement.

- Patent litigation delays that can influence biosimilar market entry.

- Quality standards and interchangeability approvals, which influence physician prescribing.

Key Takeaways

- Insulin glargine-YFGN U100 VL is positioned as a competitive biosimilar candidate with expected entry pricing of $150–$200 per 10 mL vial.

- Prices are likely to decline further as market share grows and competition intensifies.

- Long-term pricing will depend on regulatory approval timelines, reimbursement policies, and market acceptance.

- The global biosimilar insulin market is forecast to reach $7–$9 billion in revenue by 2028, representing a significant shift away from originator dominance.

- Entry timing and strategic collaborations will be critical for capturing market share.

FAQs

1. When is insulin glargine-YFGN U100 VL expected to reach the market?

Pending regulatory approval, product launch timelines vary by region. In China, approval is expected in 2023, with U.S. and Europe approvals possibly occurring in 2024.

2. What factors will influence pricing in emerging markets?

Regulatory policies, local manufacturing costs, government price controls, and payer-negotiated discounts.

3. How does biosimilar substitution impact prices?

Substitutions can accelerate price reductions and market share gains, especially in markets with generic substitution policies.

4. What are the potential barriers to market entry?

Regulatory delays, patent litigation, manufacturing capacity constraints, and physician acceptance.

5. How will biosimilar competition affect insulin prices long-term?

Prices are expected to decrease steadily as biosimilar options increase, with a narrower price gap to original products in mature markets.

Sources:

[1] IQVIA, "Global Biosimilar Market Data," 2022.

[2] Evaluate Pharma, "Insulin Market Outlook," 2022.

[3] FDA, "Approved Biosimilars," 2023.

[4] European Medicines Agency, "Biosimilar Approvals," 2023.

[5] IMS Health, "Diabetes Care Market Trends," 2022.

More… ↓