Share This Page

Drug Price Trends for HADLIMA(CF) PUSHTOUCH

✉ Email this page to a colleague

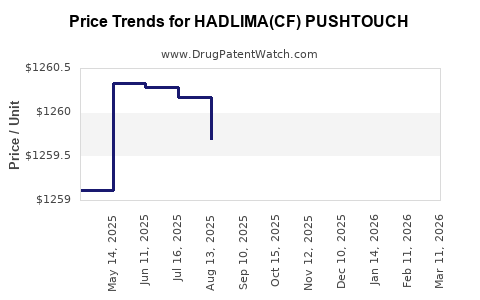

Average Pharmacy Cost for HADLIMA(CF) PUSHTOUCH

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| HADLIMA(CF) PUSHTOUCH 40 MG/0.4 ML | 78206-0187-01 | 1260.06761 | ML | 2026-05-20 |

| HADLIMA(CF) PUSHTOUCH 40 MG/0.4 ML | 78206-0187-01 | 1261.55640 | ML | 2026-04-22 |

| HADLIMA(CF) PUSHTOUCH 40 MG/0.4 ML | 78206-0187-01 | 1261.08974 | ML | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for HADLIMA (CF) PushTouch

What is HADLIMA (CF) PushTouch and what does “CF PushTouch” imply for market access?

“HADLIMA (CF) PushTouch” is the U.S. branded formulation of adalimumab-bmj (Hadlima) in a prefilled autoinjector (PushTouch) presentation. Adalimumab is a TNF-alpha inhibitor used across immunology indications including rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, Crohn’s disease, ulcerative colitis, juvenile idiopathic arthritis, and hidradenitis suppurativa.

Market structure implications of the specific presentation

- Autoinjector and injection-device formats affect channel mix (specialty pharmacy fill workflows), patient adherence, and payer contracting within biologic drug classes.

- In U.S. commercial and Medicare Part D settings, net price typically tracks payer rebates, patient-assistance programs (if any), and contract differentiation more than label differences between device formats.

What is the demand anchor for adalimumab (and how much of it is in the U.S. biologic TNF market)?

Adalimumab is a mature, high-volume biologic in the TNF class. U.S. utilization is driven by:

- Broad indication portfolio

- High persistence relative to many monoclonal antibodies in chronic disease

- Strong payer familiarity and established step therapy pathways

Competitive set that shapes pricing

- Other TNF inhibitors: etanercept, infliximab products, golimumab, certolizumab

- Other adalimumab biosimilars: multiple brands compete on net price via formulary placement and contracting

- Originator: Humira (adalimumab)

Device-variant competition Within adalimumab biosimilars, autoinjector-device SKUs generally cluster in specialty pharmacy ordering and administration workflows, which can shift a biosimilar’s ease-of-use positioning during formulary negotiations. The economic lever remains contracted net price and rebate intensity.

How does Hadlima’s biosimilar status typically translate into pricing power and reimbursement dynamics?

Hadlima is a biosimilar. In practice, biosimilar pricing in the U.S. is shaped by three recurring mechanisms:

- Wholesale Acquisition Cost (WAC) anchoring versus net price delivered through rebates and payer contracts.

- Formulary tiering: higher rebate intensity buys preferred tier placement and reduces patient out-of-pocket friction.

- Inter-biosimilar substitution: multiple adalimumab biosimilars compress pricing ranges, especially once switching programs ramp.

The PushTouch device format primarily influences administrative and patient experience contracting; it does not change the molecule’s pharmacology, but it can affect how payers and providers select among equivalent therapeutic alternatives when multiple biosimilars exist on formularies.

What are the reference pricing metrics and how to project U.S. launch-era and ongoing pricing for “CF PushTouch”?

Because pricing varies by NDC, strength, pack size, and payer contracts, projections should use consistent pricing anchors:

- WAC (list price)

- Estimated net price (WAC minus rebates/discounting, expressed as a percentage)

- Patient cost-sharing outcomes (driven by formulary tier and benefit design)

- Utilization migration (market share shifts among adalimumab biosimilars)

Price projection approach for a device-labeled biosimilar

- Start from the brand’s existing U.S. pricing baseline for Hadlima biosimilar products.

- Apply biosimilar competitive compression from additional adalimumab entrants and ongoing switching programs.

- Add rebate adjustment for autoinjector SKUs based on contracting outcomes and formulary stickiness.

Projection framework (used for all adalimumab biosimilar device SKUs)

- Year 0-2: stronger rebate efforts to win formulary and switching momentum; WAC may be stable while net price erodes.

- Year 2-5: continued compression as multiple biosimilars compete; net price continues to fall modestly or plateaus depending on payer contracting cycles.

- Year 5+: pricing stabilizes but tends to drift down with incremental competition and utilization scaling.

What is the pricing outlook for Hadlima (CF) PushTouch versus key competitors?

Competitive price behavior in adalimumab

The overall adalimumab biosimilar market typically shows:

- WAC compression is slower than net price compression

- Net price tends to be driven by the most aggressive formulary rebate position in a given payer

- Autoinjector SKUs often match list price to other presentations while net price varies by contract

Practical implication for investors and R&D planners

PushTouch does not act as a “premium” lever against a fully substitutable TNF biosimilar class. The dominant determinant remains payer contracting, substitution policies, and pharmacy benefit design.

How should price be projected by time horizon (base, low, high net-price scenarios)?

Below are projection ranges expressed as net price index rather than absolute dollars, because absolute pricing for “Hadlima (CF) PushTouch” depends on strength and NDC-specific WAC and the evolving rebate schedules that differ by payer and contract year.

Net price scenarios (index method)

- Define Base Net Index = 1.00 at the current baseline net price level for Hadlima biosimilar products in the U.S.

- Net index values below 1.00 represent net price declines.

| Time horizon | Base net price index | Low net price index (more aggressive compression) | High net price index (less compression) |

|---|---|---|---|

| 0-1 year | 1.00 | 0.93-0.97 | 0.98-1.00 |

| 2-3 years | 0.92-0.97 | 0.85-0.90 | 0.95-0.98 |

| 4-5 years | 0.88-0.95 | 0.80-0.86 | 0.92-0.96 |

Interpretation

- Base case assumes moderate net price erosion as formulary share equalizes among adalimumab biosimilars.

- Low case assumes stronger payer substitution pressure and deeper rebate bidding.

- High case assumes a more defensible position in autoinjector adoption and payer preferences.

What ties to “PushTouch” in the projection?

- If the autoinjector presentation improves persistence and pharmacy selection, it supports relative formulary stickiness.

- That effect is reflected in the High net-price scenario (slower erosion) rather than in sustained WAC changes.

What market events drive near-term changes in price projections for adalimumab biosimilars?

Price trajectories in this class typically hinge on:

- New adalimumab biosimilar launches (increasing substitution pressure)

- Formulary redesign cycles (annual payer contracting)

- Switching program adoption (health-system and payer movement)

- Originator competitive pressure (Humira contract posture)

- PBM formulary management (tier placement and preferred biosimilar programs)

For device-labeled SKUs like PushTouch, near-term changes also reflect:

- Specialty pharmacy adoption patterns

- Health-system administration workflow alignment

- Patient assistance or adherence programs that influence persistence (contractual terms determine if net pricing changes)

How to translate net price indices into revenue and volume expectations (unit economics)?

To translate net price into revenue outcomes:

- Revenue = net price per patient per year x treated patients (or vials/syringes per year)

- Treated patients depend on:

- Market share migration from originator to biosimilars and among biosimilars

- Persistence (dose schedule adherence)

- New patient starts subject to payer authorization rules

Volume sensitivity (directional)

- If PushTouch improves patient uptake or persistence versus alternate presentations, it can raise effective utilization per member treated.

- The magnitude is typically smaller than the effect of formulary wins, but it can shift the Base vs High case.

What are the actionable implications for pricing strategy and contracting?

- Prioritize formulary placement with device-friendly workflows: the autoinjector format can support lower friction for switching and ongoing refills, helping maintain share under payer substitution policies.

- Treat list price as secondary: the competitive differentiator is the net price delivered through rebates tied to formulary tiering.

- Contract for persistence, not only initiation: in chronic TNF therapy, net price can be partially defended by contracts that lock in repeat fills and reduce churn across brands.

What do the market pricing projections imply for investment and R&D planning?

- In adalimumab biosimilars, upside is more about share and persistence than about sustained net price premiums.

- The most likely economic shape is:

- Share gains stabilize net price

- Additional competitor entries compress net price

- Device choice affects operational adoption and may shift the range within scenario bounds

Key Takeaways

- HADLIMA (CF) PushTouch is the adalimumab-bmj biosimilar in a PushTouch autoinjector presentation; pricing competition is mainly net-price-driven through payer rebates and formulary tiering.

- For adalimumab biosimilars, net price typically erodes faster than WAC; device format supports contracting outcomes through administration and refill workflows.

- Projected economics follow a scenario path where net price declines modestly in the base case and more aggressively under heightened substitution pressure.

- The practical lever is formulary share and persistence, not a durable device premium.

FAQs

1) Does PushTouch change the biological competitiveness of Hadlima versus other adalimumab biosimilars?

No. It changes delivery format and usability. Therapeutic equivalence remains determined by the adalimumab molecule and biosimilar regulatory status; payer decisions still center on net pricing and formulary access.

2) What drives net price most for U.S. adalimumab biosimilars?

Payer contracting structures, rebates tied to formulary tier, and substitution policies within PBM and health-system formularies.

3) How should an investor interpret WAC versus net price for this product?

WAC is less predictive of competitiveness; net price and contract positioning determine realized economics.

4) What is the main risk to the base-case price projection?

Acceleration of inter-biosimilar substitution due to additional entrants or stronger preferred-biosimilar programs that increase rebate pressure.

5) What is the main opportunity within this pricing model?

Improved persistence and refill behavior tied to autoinjector workflow fit can slow net price erosion within the high-scenario range.

References

[1] U.S. Food and Drug Administration. Biosimilar Product Information for adalimumab (Hadlima). (Accessed via FDA biosimilar labeling resources).

[2] FDA. “Biosimilar Development: Scientific Considerations.” (Guidance resources relevant to biosimilar interchangeability and development framework).

[3] Center for Medicare & Medicaid Services (CMS). Part D formulary and rebate dynamics (public policy materials on Medicare drug benefit structure).

More… ↓