Last updated: April 23, 2026

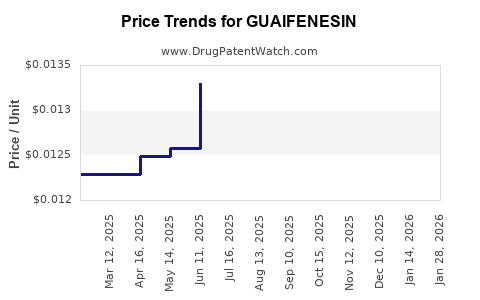

Guaifenesin is an off-patent, high-volume expectorant sold globally in multiple OTC formats (syrups, tablets, and combination products). Because the active ingredient is largely generic and production is established, price behavior tracks (1) raw material and manufacturing costs, (2) OTC competitive intensity, and (3) trade and pharmacy channel dynamics rather than patent-driven pricing. The market is likely to keep pricing near generic benchmarks, with incremental movement driven by mix shifts (single-entity vs combination) and regulatory or labeling changes.

What does the guaifenesin market look like by product form and channel?

1) Dominant commercial formats

Guaifenesin is marketed primarily as:

- Single-entity expectorant (guaifenesin-containing cough syrups or tablets)

- Combination OTC products with other cold and cough actives (e.g., decongestants, antihistamines, antitussives)

Combination products tend to hold stronger shelf position during peak seasonal demand because they provide multi-symptom relief, but the incremental price premium is typically limited by generic substitution and pharmacy private label.

2) Channel structure

- OTC retail (pharmacies and mass retail): primary volume driver; pricing is shaped by shelf competition and promotions.

- E-commerce OTC: typically compresses effective net pricing via discounting and assortment breadth.

- Institutional procurement: appears more relevant for high-turn generic formulations, though brand differentiation is limited for the active.

3) Demand seasonality

Demand is highly seasonal in temperate geographies, with higher sales in Q4 to Q1 and in respiratory virus peaks. This creates short-cycle production planning and can temporarily influence wholesale pricing during supply tightness, but it rarely sustains multi-quarter price escalations because guaifenesin has many suppliers.

What pricing constraints and economics govern guaifenesin?

1) Generic competition is the core pricing limiter

As an established OTC active, guaifenesin pricing is constrained by:

- Multiple generic suppliers competing on formulation and packaging

- Pharmacy substitution and pack-size comparability

- Private label presence in many OTC segments

- Promotional retail cycles that pull net prices below list

2) Cost drivers

Pricing movement is most sensitive to:

- API and excipient costs (including bulk manufacturing inputs)

- Packaging format (bottles vs blister tablets; cap and dosing components)

- Freight and import costs for certain branded or region-specific bottlings

- Quality and compliance overhead (GMP and pharmacopoeial testing requirements)

3) Product mix matters

Even if API pricing is stable, consumer and payer spend can move because of:

- Shift from single-entity to combination (higher effective dose and higher number of actives)

- Shift in pack size (e.g., 4 oz vs 8 oz vs value multipacks)

- Shift to extended-release or specific dosing regimens (where marketed)

What are the most actionable market indicators to track?

For pricing and projection work, the practical indicators are:

- Wholesale and retail price indices for OTC cough/cold categories (proxy for competitive compression and promotional intensity)

- API and excipient price changes for bulk chemical inputs (short-cycle impact on gross margin)

- Import and freight rates in major consuming regions (temporary supply cost effects)

- Seasonality alignment (virus intensity can shift volumes and reorder timing, changing short-term spot pricing)

How does regulatory status affect pricing?

Guaifenesin is a long-established OTC expectorant with well-defined labeling and use patterns across major markets. Regulation generally limits manufacturing and marketing claims but typically does not create sustained pricing power for the active once generic competition is entrenched.

Price projection framework: base case to downside

Because guaifenesin is off-patent and competitively traded OTC, projections should be framed around net price stability with seasonal fluctuations and modest annual inflation pass-through. Without patent constraints, sustained step-change pricing requires a cost shock or supply disruption.

Key assumptions for projections

- No major patent/payer policy changes that materially reduce generic availability

- No sustained raw-material spike beyond normal cyclical variation

- OTC competitive intensity remains high, keeping long-run pricing near generic benchmarks

- Seasonality persists with standard replenishment cycles

What does this imply for near-term (12–24 month) pricing?

Base case

- Net pricing: flat to low single-digit annual growth

- Seasonal pattern: temporary wholesale-to-retail movement during peak respiratory seasons, followed by normalization

- Mix impact: modest uplift possible if combination products gain shelf share

Downside case

- Net pricing: slight decline if promotional intensity rises or if supply is plentiful

- Margin compression: likely for weaker manufacturers due to higher promotional pressure

Upside case

- Net pricing: mid single-digit growth only if there is a cost increase that cannot be fully competed away in retail channels (rare without supply issues)

What does this imply for 3–5 year price trajectory?

Base case (most likely)

- Annual average net price: low single-digit growth with wide retail variation by geography and pack configuration

- Gross margin: stable to slightly pressured as retail competition offsets cost inflation

- Volume: grows with population and OTC penetration, but not strongly tied to sustained price growth

Downside case

- Net price: near-zero to negative real growth as generics and private label increase shelf dominance

- Manufacturing consolidation: could occur if weaker producers exit, but this typically does not quickly restore higher pricing for an established OTC active

Upside case

- Net price: sustained higher pricing requires repeated cost shocks or structural supply contraction. Single events tend to reverse once capacity re-ramp occurs.

Scenario table: annual net price change (indicative)

(Expressed as annual % change in net pricing to retailers/wholesalers; actual outcomes depend on geography and pack mix.)

| Scenario |

Year 1-2 (net price CAGR) |

Year 3-5 (net price CAGR) |

Drivers |

| Base case |

0% to +3% |

+1% to +2% |

Cost pass-through with competitive constraints; mix shift to higher-value formats |

| Downside |

-2% to 0% |

-1% to +1% |

Promotions, increased generic/private label, stable or falling input costs |

| Upside |

+3% to +6% |

+2% to +4% |

Persistent input cost rise, supply tightness, or structural reductions in effective competition |

How to translate pricing into revenue impact

Revenue = Net price × Volume.

For guaifenesin, volume changes track respiratory seasonality more than pricing incentives. Therefore:

- If net pricing is flat, revenue growth comes mainly from volume and mix.

- If net pricing rises, it is often offset by substitution to cheaper pack sizes or private label.

In combination products, the active mix can increase the shelf price even if guaifenesin alone does not command premium pricing.

Competitive landscape: what moves market share?

For OTC guaifenesin, market share typically shifts due to:

- Pack size value perception (unit dose economics)

- Formulation preference (liquid vs tablet; dosing convenience)

- Brand visibility and trade spend at retail

- Retailer private label penetration

- Seasonal promotion calendars

For investors or procurement buyers, share shifts matter because they affect demand allocation among suppliers during peak replenishment.

Key risk factors that can change price direction

Even in a generic market, price direction can flip if:

- Capacity disruptions occur (plant shutdowns, quality failures, inspection actions)

- Raw material supply becomes constrained (bulk chemical shortages)

- Large retailers change assortment (dropping higher-priced SKUs)

- Regulatory labeling or enforcement changes affect claims, branding, or product formats

Key Takeaways

- Guaifenesin pricing is primarily driven by generic competition and OTC channel dynamics, not patent-based mechanisms.

- Near-term pricing is likely flat to low single-digit growth, with seasonal volatility during respiratory peaks.

- Over 3–5 years, the most likely pattern is low single-digit annual net price growth or near-zero real growth if promotions and private label intensify.

- Base-case outcomes depend on input cost pass-through and mix shifts toward higher-value formats (especially combination products).

FAQs

1) Will guaifenesin prices steadily increase because it is an established OTC drug?

No. Generic substitution and retailer promotions typically cap long-run price increases. Expect near-flat net pricing with modest inflation pass-through.

2) What is the main determinant of short-term guaifenesin pricing moves?

Seasonality-driven procurement timing and any cost or supply shocks in bulk inputs or manufacturing logistics.

3) Does combination guaifenesin pricing behave differently than single-entity guaifenesin?

Yes. Combination products usually carry higher shelf prices due to added actives and perceived multi-symptom utility, but they still face generic and store-brand competition.

4) What scenario is most likely for the next 12–24 months?

Base case: flat to low single-digit net price growth, with peaks during respiratory season and normalization afterward.

5) What is the biggest threat to margin for guaifenesin suppliers?

Retail promotional intensity and substitution into lower-priced packs/private label, which compresses net pricing even if input costs rise.

References

[1] FDA. Drug Approval Reports and Product Labeling (OTC Monographs and drug facts information for cough and cold products, including expectorants). U.S. Food and Drug Administration. https://www.fda.gov/

[2] United States Pharmacopeia (USP). Guaifenesin monograph and quality standards. USP. https://www.uspnf.com/

[3] WHO. WHO Model List of Essential Medicines (context on established medicines and general market dynamics). World Health Organization. https://www.who.int/