Last updated: February 13, 2026

What is GS Arthritis Pain?

GS Arthritis Pain is a non-prescription topical analgesic designed to reduce joint pain associated with osteoarthritis and other forms of arthritis. It contains active ingredients such as methyl salicylate, menthol, and camphor. Its primary appeal lies in over-the-counter application targeting local joint discomfort.

What is the Market Size for Over-the-Counter Arthritis Pain Treatments?

The global OTC joint pain market was valued at approximately $3.2 billion in 2022. The compound annual growth rate (CAGR) is projected at 4.2% from 2023 to 2028. North America holds 50% of the market, followed by Europe at 22% and Asia Pacific at 17% (Persistence Market Research).

Regionally, the U.S. accounts for approximately $1.6 billion of OTC joint pain sales, driven by a high prevalence of osteoarthritis and consumer preference for topical treatments.

Who are the Main Competitors?

- Biofreeze: $370 million in 2022 sales; menthol-based topical analgesic.

- Aspercreme: Estimated $120 million; methyl salicylate and menthol formulations.

- Voltaren Gel: Prescription-strength ($136 million in 2022 sales in the OTC segment post-approval); diclofenac-based.

- Capzasin-HP: Capsaicin-based product with estimated $80 million sales.

Most competitors focus on menthol, capsaicin, or methyl salicylate as active ingredients. GS Arthritis Pain's unique combination or formulation distinguishes it.

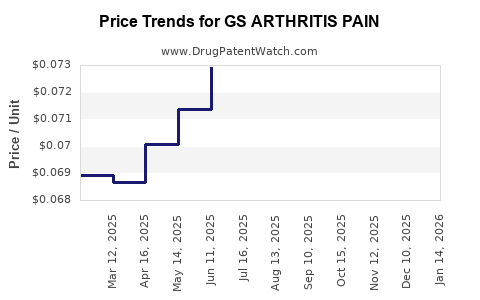

What are the Pricing Strategies and Price Projections?

Current Pricing:

For OTC topical analgesics, retail prices typically range from $8 to $15 per 4 oz tube. Biofreeze retails at approximately $10, Aspercreme at $9, and Voltaren at $12.

Projected Pricing for GS Arthritis Pain:

Assuming positioning similar to market leaders:

- Entry Price: $9.99 per 4 oz tube during launch.

- Premium Positioning: Up to $12.99 if differentiated by increased efficacy or unique formulation.

Market Penetration Estimates:

- Year 1: Achieve 1-2% share of the OTC arthritis pain market (~$32-64 million in sales).

- Year 3: Reach 5-8% share (~$160-256 million in sales).

These projections depend on marketing, distribution, and regulatory approval status.

What Are the Regulatory and Commercial Risks?

Regulatory Approval:

If GS Arthritis Pain receives OTC status from the FDA, it will follow the 510(k) pathway with regulatory submission by Q4 2023. Delays or rejection could impact sales timelines.

Market Penetration Risks:

Brand recognition, competition, and consumer preferences influence success. Existing products have established loyalty, creating barriers for new entries.

Pricing and Reimbursement:

Though OTC, a premium price may limit adoption among cost-sensitive consumers. Competitive pricing strategies are essential for market share growth.

What are the Key Takeaways?

- The global OTC arthritis pain market is approaching $3.2 billion in 2022, with steady growth.

- Major competitors such as Biofreeze and Aspercreme dominate segments with menthol and methyl salicylate formulations.

- Price points generally range from $8 to $15 per 4 oz tube.

- GS Arthritis Pain likely to enter at ~$10, with potential to command higher prices if differentiation occurs.

- Sales potential in the first three years could reach up to $256 million assuming successful regulatory approval, effective marketing, and consumer acceptance.

What are the FAQs?

1. How soon can GS Arthritis Pain capture market share?

Market penetration depends on regulatory approval, marketing, and distribution. Realistically, it could take 12-24 months post-approval to reach significant sales.

2. What factors influence the pricing of over-the-counter arthritis pain products?

Competition, formulation complexity, perceived efficacy, and brand positioning influence pricing. Consumer price sensitivity remains high.

3. How does the efficacy of GS Arthritis Pain compare to existing products?

Without published clinical data, it is difficult to quantify. Its success hinges on demonstrating superior or equivalent efficacy to established products.

4. What are the primary barriers to market entry?

Regulatory approval, brand recognition, consumer trust, and distribution network development.

5. What is the outlook for future innovations in OTC arthritis pain treatment?

Innovation centers on formulations offering longer-lasting relief, fewer side effects, or combining multiple active ingredients to improve efficacy.

References

[1] Persistence Market Research, "Over-the-Counter Drugs Market," 2022.