Drug Price Trends for FULPHILA

✉ Email this page to a colleague

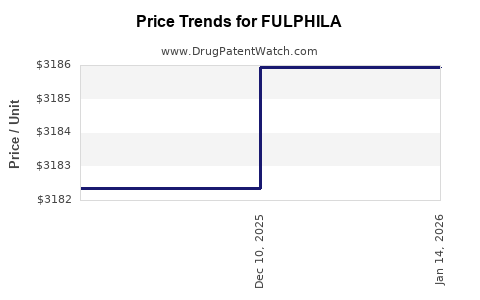

Average Pharmacy Cost for FULPHILA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FULPHILA 6 MG/0.6 ML SYRINGE | 67457-0833-06 | 3185.93667 | ML | 2026-01-21 |

| FULPHILA 6 MG/0.6 ML SYRINGE | 83257-0005-41 | 3185.93667 | ML | 2026-01-21 |

| FULPHILA 6 MG/0.6 ML SYRINGE | 67457-0833-06 | 3185.93667 | ML | 2025-12-17 |

| FULPHILA 6 MG/0.6 ML SYRINGE | 83257-0005-41 | 3185.93667 | ML | 2025-12-17 |

| FULPHILA 6 MG/0.6 ML SYRINGE | 67457-0833-06 | 3182.34667 | ML | 2025-11-19 |

| FULPHILA 6 MG/0.6 ML SYRINGE | 83257-0005-41 | 3182.34667 | ML | 2025-11-19 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for FULPHILA

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| FULPHILA 6MG/0.6ML INJ,SOLN,SYR | Biocon Biologics, Inc. | 83257-0005-41 | 1X0.6ML | 1315.51 | 2024-03-01 - 2029-02-28 | FSS | ||

| FULPHILA 6MG/0.6ML INJ,SOLN,SYR | Biocon Biologics, Inc. | 67457-0833-06 | 1X0.6ML | 1315.51 | 2024-03-01 - 2029-02-28 | Big4 | ||

| FULPHILA 6MG/0.6ML INJ,SOLN,SYR | Biocon Biologics, Inc. | 67457-0833-06 | 1X0.6ML | 1315.51 | 2024-03-01 - 2029-02-28 | FSS | ||

| FULPHILA 6MG/0.6ML INJ,SOLN,SYR | Biocon Biologics, Inc. | 83257-0005-41 | 1X0.6ML | 1315.51 | 2024-03-01 - 2029-02-28 | Big4 | ||

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |