Share This Page

Drug Price Trends for FLUORIDE

✉ Email this page to a colleague

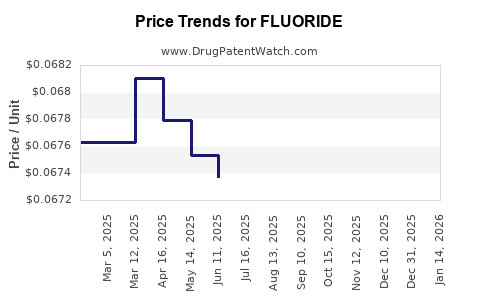

Average Pharmacy Cost for FLUORIDE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FLUORIDE 0.5 MG TABLET CHEW | 75826-0164-20 | 0.07282 | EACH | 2026-05-20 |

| FLUORIDE 0.25 MG TABLET CHEW | 75826-0163-20 | 0.07002 | EACH | 2026-05-20 |

| FLUORIDE 1 MG TABLET CHEWABLE | 75826-0165-20 | 0.06912 | EACH | 2026-05-20 |

| FLUORIDE 0.5 MG TABLET CHEW | 75826-0164-20 | 0.07194 | EACH | 2026-04-22 |

| FLUORIDE 1 MG TABLET CHEWABLE | 75826-0165-20 | 0.06787 | EACH | 2026-04-22 |

| FLUORIDE 0.25 MG TABLET CHEW | 75826-0163-20 | 0.06915 | EACH | 2026-04-22 |

| FLUORIDE 0.25 MG TABLET CHEW | 75826-0163-20 | 0.06927 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Fluoride Drug Market Analysis and Price Projections

Fluoride, primarily used as sodium fluoride or stannous fluoride, is a mineral compound with established applications in dental caries prevention and bone metabolism. The global market for fluoride-based pharmaceuticals is segmented by application, formulation, and distribution channel. Projected market growth is influenced by increasing awareness of oral hygiene, aging populations, and the prevalence of osteoporosis, alongside regulatory landscapes and competitive pressures from alternative treatments.

What is the current market size and projected growth for fluoride-based pharmaceuticals?

The global market for fluoride therapeutics, encompassing dental caries prevention and osteoporosis treatment, was valued at approximately $750 million in 2023. Market analysts project a compound annual growth rate (CAGR) of 4.5% to 5.2% over the next five years, reaching an estimated $975 million to $1.1 billion by 2028. This growth is driven by the consistent demand for caries prevention products and an expanding patient base for osteoporosis treatments.

Key Market Drivers

- Oral Hygiene Awareness: Increasing public education campaigns and widespread availability of fluoride toothpaste and mouth rinses sustain demand for dental applications.

- Aging Population: The rising global elderly population contributes to a higher incidence of osteoporosis, boosting the demand for fluoride-based bone resorption inhibitors.

- Chronic Disease Prevalence: Growing rates of conditions leading to bone mineral loss increase the therapeutic need for fluoride.

- Emerging Markets: Greater access to healthcare and rising disposable incomes in developing economies expand the addressable market for fluoride treatments.

Market Restraints

- Regulatory Scrutiny: Stringent approval processes for new formulations and indications can delay market entry and increase development costs.

- Competition: Availability of alternative treatments for osteoporosis, such as bisphosphonates and biologics, presents competitive challenges.

- Adverse Event Concerns: While generally safe, potential side effects like dental fluorosis at excessive doses and gastrointestinal issues with oral formulations necessitate careful dosage management.

What are the primary applications and their market share within the fluoride drug sector?

The fluoride drug market is dominated by two principal application segments: dental caries prevention and bone metabolism disorders (primarily osteoporosis).

Application Segment Market Share (2023 Estimate)

- Dental Caries Prevention: This segment represents the largest share, accounting for approximately 65% of the total market. This is primarily driven by the widespread use of fluoride in toothpaste, mouth rinses, and professional dental treatments.

- Bone Metabolism Disorders (Osteoporosis): This segment holds the remaining 35% of the market. Fluoride therapy, typically using sodium fluoride, is prescribed for its osteogenic properties in treating osteoporosis, although its use has evolved with the advent of newer osteoporosis medications.

The demand in the dental segment is characterized by high-volume, lower-cost products, while the bone metabolism segment involves prescription-based therapies with higher per-unit costs.

What are the major formulations and their respective market positions?

Fluoride is available in various formulations tailored to its intended application and route of administration.

Key Formulations and Market Presence

- Topical Applications (Gels, Varnishes, Foams, Toothpastes, Mouthwashes): These formulations dominate the dental caries prevention segment. They deliver fluoride directly to tooth surfaces, facilitating remineralization. The market for these products is highly competitive, with numerous brands and generic options available.

- Oral Formulations (Tablets, Capsules): Primarily used for systemic treatment of osteoporosis and, historically, for caries prevention in specific high-risk populations. Sodium fluoride tablets are prescribed by physicians. This segment is characterized by prescription pharmaceuticals.

- Injectable Formulations: Less common for fluoride therapy, these may be used in specific clinical settings for systemic administration, but represent a niche market.

The market share of oral formulations is tied to the prescription rates for osteoporosis, while topical applications hold sway in the broader consumer dental health market.

Who are the key players in the fluoride drug market?

The fluoride drug market comprises a mix of large pharmaceutical corporations, specialized dental product manufacturers, and generic drug companies.

Leading Market Participants

- Colgate-Palmolive Company: A dominant player in the consumer dental segment, offering a wide range of fluoride toothpastes and mouth rinses.

- Procter & Gamble (P&G): Another major consumer goods company with significant market presence in oral care products, including fluoride-based toothpastes.

- 3M Company: Offers professional dental products, including fluoride varnishes and other topical applications for caries prevention.

- Merck & Co., Inc.: While not solely focused on fluoride, Merck produces pharmaceuticals for bone health that compete with or are used in conjunction with fluoride therapies for osteoporosis.

- Generic Pharmaceutical Manufacturers: Numerous companies produce generic versions of oral sodium fluoride supplements and prescription osteoporosis treatments, contributing to price competition.

The competitive landscape is fragmented in the consumer dental segment and more consolidated in the prescription oral therapy segment, albeit with increasing generic penetration.

What are the price trends and projections for fluoride-based pharmaceuticals?

Price trends for fluoride-based pharmaceuticals vary significantly based on formulation, application, and market positioning (prescription vs. over-the-counter).

Price Trend Analysis

- Dental Topical Applications (OTC): Prices for fluoride toothpastes and mouthwashes are generally stable, with minor annual increases driven by inflation and product innovation. Bulk purchasing and competition among manufacturers keep prices competitive. A standard fluoride toothpaste tube (e.g., 4.0-6.0 oz) typically ranges from $2.00 to $6.00. Fluoride varnishes for professional application have higher per-application costs, ranging from $20 to $50 per treatment.

- Oral Prescription Fluoride (Sodium Fluoride Tablets): These are prescription-based and their pricing is subject to insurance coverage and pharmacy markups. A prescription for 100 tablets of sodium fluoride (e.g., 2.2 mg or 5 mg) can range from $15 to $40, depending on the manufacturer and pharmacy. Pricing for prescription fluoride therapies used in osteoporosis management is higher, often in the range of $50 to $200 per month, depending on the specific drug and dosage.

- Price Projections:

- OTC dental fluoride products are expected to see continued price stability, with annual increases likely to remain below 2%.

- Prescription oral fluoride products may experience moderate price increases of 3% to 6% annually, driven by manufacturing costs and demand, particularly for osteoporosis treatments. Generic competition will continue to exert downward pressure on prices for established oral formulations.

- The introduction of novel fluoride delivery systems or combination therapies could lead to premium pricing for specific, highly targeted applications.

What is the impact of regulatory policies on the fluoride drug market?

Regulatory policies, enacted by bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), significantly shape the development, marketing, and pricing of fluoride drugs.

Regulatory Landscape and Impact

- FDA and EMA Oversight: Both agencies regulate fluoride-containing drugs, requiring rigorous clinical trials to demonstrate safety and efficacy for specific indications. For dental products, guidelines from organizations like the American Dental Association (ADA) also influence product acceptance and consumer trust.

- Approval Pathways: New drug applications (NDAs) for systemic fluoride therapies, particularly for osteoporosis, are subject to extensive review. Over-the-counter (OTC) dental products generally follow less stringent regulations but must adhere to labeling and safety standards.

- Dosage and Safety Guidelines: Regulatory bodies and public health organizations provide guidelines on optimal fluoride intake to prevent dental caries while minimizing the risk of fluorosis. This influences product formulations and recommended usage.

- Pricing Regulations: In some international markets, price controls and reimbursement policies enacted by national health authorities can affect the profitability and market access of prescription fluoride drugs. The U.S. market generally allows for greater pricing freedom, influenced by market demand and competition.

- Intellectual Property: Patent protection for novel fluoride formulations or delivery mechanisms is crucial for market exclusivity and can influence pricing strategies. Expiration of key patents leads to the introduction of generic alternatives, typically resulting in a substantial price drop. For instance, following patent expirations on certain branded osteoporosis treatments incorporating fluoride, generic versions have entered the market at significantly lower price points, often reducing costs by 50% to 70%.

What is the competitive landscape and outlook for market entrants?

The competitive landscape for fluoride drugs is bifurcated, with a highly saturated consumer dental market and a more specialized prescription market for bone health.

Competitive Analysis

- Dental Segment: This segment is characterized by intense competition among major consumer goods companies and dental product manufacturers. Differentiation is achieved through product features (e.g., whitening, sensitivity relief), branding, and marketing. Market entry for new OTC fluoride dental products requires substantial investment in consumer marketing and distribution.

- Bone Health Segment: Competition here involves pharmaceutical companies offering prescription treatments for osteoporosis. While fluoride has a long history, newer drug classes like bisphosphonates (e.g., alendronate) and biologics (e.g., denosumab) have gained significant market share due to different efficacy profiles and administration routes. Companies entering this space must demonstrate clear clinical advantages over existing therapies.

- Generic Competition: The market for oral sodium fluoride supplements and older osteoporosis medications is subject to robust generic competition. This limits the pricing power of manufacturers of off-patent products.

- Outlook for New Entrants:

- Dental: New entrants face challenges in gaining significant market share in the crowded OTC dental segment without substantial R&D for novel formulations or unique marketing strategies.

- Bone Health: Opportunities exist for companies developing improved fluoride delivery systems, combination therapies, or new indications. However, the high cost of clinical trials and the need to prove superiority or non-inferiority against established treatments are significant barriers. Strategic partnerships or acquisitions of existing technologies may offer a viable entry point.

What are the key distribution channels and their market penetration?

The distribution of fluoride drugs is segmented according to their regulatory status and intended application.

Distribution Channel Breakdown

- Retail Pharmacies & Supermarkets: The primary channel for over-the-counter (OTC) fluoride toothpastes, mouthwashes, and dental rinses. This channel accounts for a substantial volume of sales due to broad consumer access.

- Dental Professional Channels (Dental Offices, Clinics): This channel distributes professional-grade fluoride treatments such as varnishes, gels, and foams directly to patients by dentists and hygienists. It also includes sales of prescription-strength fluoride supplements for high-risk individuals.

- Prescription Pharmacies: Dispense prescription-only fluoride medications, primarily for the treatment of osteoporosis and severe caries risk.

- Online Retailers: A growing channel for both OTC and some prescription fluoride products, offering convenience and competitive pricing.

The penetration of these channels is directly correlated with the product type. OTC dental products have near-universal penetration through retail and online channels, while prescription therapies are concentrated in pharmacies and healthcare provider networks.

What is the outlook for research and development in fluoride therapeutics?

Research and development in fluoride therapeutics are primarily focused on optimizing delivery systems, enhancing therapeutic efficacy, and addressing safety concerns.

R&D Focus Areas

- Enhanced Delivery Systems: Development of novel topical formulations for sustained fluoride release in dental applications, aiming for increased protection against caries. This includes microencapsulation techniques and advanced varnish formulations.

- Combination Therapies: Research into combining fluoride with other active agents for synergistic effects in treating osteoporosis or managing complex oral health issues.

- Personalized Fluoride Therapy: Exploring genetic or risk-factor-based approaches to tailor fluoride supplementation or topical application for optimal caries prevention with minimal risk of fluorosis.

- Improved Osteogenic Properties: Investigating fluoride compounds or delivery methods that enhance bone formation and reduce bone resorption with a more favorable safety profile compared to older regimens.

- Addressing Systemic Exposure: Research aimed at minimizing systemic absorption from topical dental applications to further reduce the risk of fluorosis, particularly in young children.

While the fundamental role of fluoride in mineral health is well-established, R&D aims to refine its application for greater precision and improved patient outcomes.

Key Takeaways

The global fluoride drug market is projected to grow at a CAGR of 4.5% to 5.2% through 2028, driven by dental hygiene and osteoporosis treatment demand. Dental caries prevention constitutes the largest segment (65%), followed by bone metabolism disorders (35%). Topical applications dominate the market, with oral prescription formulations holding a significant share in bone health. Key players include Colgate-Palmolive, P&G, and 3M in dental, with pharmaceutical giants involved in prescription bone health. Price stability is expected for OTC dental products, while prescription therapies may see moderate increases. Regulatory oversight from agencies like the FDA and EMA critically influences market access and product development. The competitive landscape is fragmented in dental OTC and more specialized in prescription bone health, with generic competition exerting downward price pressure. Research and development are focusing on advanced delivery systems and combination therapies.

Frequently Asked Questions

- What is the projected market value for fluoride therapeutics in 2028?

- Which application segment holds the largest market share for fluoride drugs?

- What are the primary factors contributing to the growth of the fluoride drug market?

- How does regulatory approval impact the pricing of new fluoride-based drugs?

- What is a significant challenge for new companies looking to enter the prescription bone health segment of the fluoride market?

Citations

[1] Market Research Report on Fluoride Therapeutics. (2024). Global Market Insights, Inc. [2] Oral Health Market Analysis. (2023). Mordor Intelligence. [3] Osteoporosis Treatment Market Trends. (2024). Fortune Business Insights. [4] U.S. Food and Drug Administration. (n.d.). Drugs, Biologics, and Medical Devices. Retrieved from fda.gov [5] European Medicines Agency. (n.d.). Medicines. Retrieved from ema.europa.eu [6] American Dental Association. (n.d.). Fluoride Toothpaste. Retrieved from ada.org [7] Pharmaceutical Pricing and Reimbursement Landscape. (2023). IQVIA. [8] Patent Landscape Analysis: Dental and Bone Health Compounds. (2024). Clarivate Analytics.

More… ↓