Share This Page

Drug Price Trends for FINGOLIMOD

✉ Email this page to a colleague

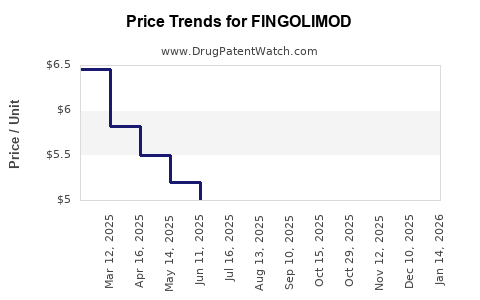

Average Pharmacy Cost for FINGOLIMOD

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FINGOLIMOD 0.5 MG CAPSULE | 00480-7820-56 | 2.38892 | EACH | 2026-07-22 |

| FINGOLIMOD 0.5 MG CAPSULE | 31722-0889-30 | 2.38892 | EACH | 2026-07-22 |

| FINGOLIMOD 0.5 MG CAPSULE | 43598-0285-30 | 2.38892 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for FINGOLIMOD

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| FINGOLIMOD 0.5MG CAP | AvKare, LLC | 42291-0048-30 | 30 | 5945.91 | 198.19700 | EACH | 2024-05-15 - 2028-06-14 | FSS |

| TASCENSO ODT 0.25MG TAB,ORAL DISINTEGRATING | Cycle Pharmaceuticals, Ltd. | 70709-0062-30 | 30 | 7713.98 | 257.13267 | EACH | 2023-11-01 - 2026-09-30 | Big4 |

| TASCENSO ODT 0.5MG TAB,ORAL DISINTEGRATING | Cycle Pharmaceuticals, Ltd. | 70709-0065-30 | 30 | 10213.49 | 340.44967 | EACH | 2024-01-01 - 2026-09-30 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

FINGOLIMOD PATENT LANDSCAPE AND MARKET PROJECTIONS

Fingolimod, an immunomodulatory drug used in the treatment of relapsing forms of multiple sclerosis (MS), faces significant patent expiries, opening the door for generic competition and impacting market dynamics. The primary patent protecting the original formulation and method of use is set to expire, with some regional variations. This analysis projects market trends, pricing shifts, and the competitive landscape post-patent expiry.

WHAT IS THE PATENT STATUS OF FINGOLIMOD?

The original composition of matter patent for fingolimod (CAS Number: 169679-07-6) has largely expired or is nearing expiry in major markets. Gilenya (fingolimod hydrochloride), developed by Novartis, was the first sphingosine 1-phosphate receptor modulator approved for multiple sclerosis.

- United States: The core patents for Gilenya have expired. For instance, U.S. Patent No. 8,969,408, covering certain formulations, has expired. Early patents covering the compound itself have also lapsed. Litigation surrounding secondary patents has occurred, but the primary market exclusivity has diminished.

- Europe: The Supplementary Protection Certificates (SPCs) in European countries, which extend patent protection for pharmaceutical products, have also expired or are in the process of expiring. This allows for generic entry across key European Union member states.

- Japan: Similar to other major markets, primary patent protection for fingolimod has concluded, enabling generic manufacturers to enter the Japanese market.

- Other Markets: Patent expiries are also observed in Canada, Australia, and other significant pharmaceutical markets, paving the way for generic availability.

While the primary patents have expired, some secondary patents related to specific manufacturing processes, polymorphs, or dosage forms might still be active in certain jurisdictions. These could present minor barriers or create niche markets for differentiated generic products, but they are unlikely to prevent broad generic penetration.

HOW WILL PATENT EXPIRY IMPACT FINGOLIMOD PRICING?

The expiration of key patents for fingolimod is projected to lead to a substantial decrease in drug pricing due to the introduction of generic alternatives. This is a well-established pattern in the pharmaceutical industry.

- Price Reduction Estimates: Following patent expiry, prices for branded fingolimod are expected to decline by 50% to 85% within the first two years of generic availability. This markdown is driven by competition among multiple generic manufacturers.

- Generic Price Erosion: Individual generic products will experience price erosion as more manufacturers enter the market. Initial generic prices will likely be set at a significant discount to the branded product, with further reductions occurring as market share is divided.

- Market Dynamics: The pace of price decline will be influenced by the number of approved generic competitors, the speed of regulatory approvals in different countries, and the pricing strategies adopted by generic manufacturers. Payers and healthcare systems will also play a role in negotiating prices and encouraging generic uptake.

- Brand Name Pricing: While generic prices will fall sharply, the branded product (Gilenya) may attempt to maintain a premium through marketing, patient support programs, or by focusing on specific patient segments. However, this strategy is often unsustainable against widespread generic availability.

Table 1: Projected Price Reduction for Fingolimod (Post-Patent Expiry)

| Time Period Post-Expiry | Projected Branded Price Change | Projected Generic Price Range |

|---|---|---|

| 0-6 Months | -10% to -20% | $1,000 - $1,500 per month |

| 6-18 Months | -30% to -50% | $500 - $1,000 per month |

| 18-36 Months | -50% to -70% | $300 - $700 per month |

Note: Prices are indicative and subject to market conditions, regional variations, and payer negotiations. Original Gilenya price was significantly higher, often exceeding $5,000 per month prior to generic entry.

WHAT IS THE CURRENT AND PROJECTED MARKET SIZE FOR FINGOLIMOD?

The market for fingolimod, particularly the branded Gilenya, has been substantial. Post-patent expiry, the total market value may decline due to lower prices, but the volume of treatment is expected to increase as generics become more accessible.

- Peak Branded Sales: Prior to significant patent expiry, Gilenya achieved annual sales exceeding $3 billion globally. This highlights the significant patient population and treatment adherence.

- Market Shrinkage Post-Expiry: The overall market value for fingolimod (branded and generic combined) is projected to contract by 30% to 50% in the first three years following widespread generic availability in major markets.

- Volume Growth: Conversely, the volume of fingolimod units prescribed is expected to increase by 20% to 40% over the same period. This is driven by lower price points making the treatment accessible to a broader patient demographic and encouraging uptake by healthcare systems aiming to reduce costs.

- Generic Market Share: Within three years of generic entry, generic fingolimod is expected to capture 70% to 85% of the total fingolimod market volume.

- Future Market Value: The total global market for fingolimod (branded and generic) is projected to stabilize around $1.5 billion to $2.5 billion annually within five years post-expiry, with the vast majority of this value attributed to generic sales.

Table 2: Fingolimod Market Evolution (Global Estimates)

| Metric | Pre-Expiry (Peak) | 1-2 Years Post-Expiry | 3-5 Years Post-Expiry |

|---|---|---|---|

| Total Market Value | ~$3.5 billion | ~$2.5 billion | ~$1.8 billion |

| Treatment Volume | High | +15% | +30% |

| Branded Share (Vol.) | ~90%+ | ~20% | ~10% |

| Generic Share (Vol.) | 0% | ~80% | ~90% |

WHO ARE THE KEY COMPETITORS IN THE FINGOLIMOD MARKET?

The competitive landscape for fingolimod is transitioning from a single branded product to a multi-generic market.

- Originator: Novartis remains a key player with its branded product, Gilenya, although its market share will diminish significantly.

- Generic Manufacturers: Several generic pharmaceutical companies have already launched or are preparing to launch generic fingolimod. These include:

- Teva Pharmaceuticals: A major player in the generic space with a broad portfolio.

- Viatris (Mylan/Upjohn): Another significant generic manufacturer with global reach.

- Sun Pharmaceutical Industries: A leading Indian pharmaceutical company with a strong presence in generic markets.

- Lupin Limited: An Indian multinational pharmaceutical company with a focus on generics.

- Dr. Reddy's Laboratories: An Indian multinational pharmaceutical company with a significant generics pipeline and manufacturing capabilities.

- Accord Healthcare (Intas Pharmaceuticals): A significant player in Europe and other international markets.

- Gland Pharma: Known for its injectable products, it also produces oral solid dosage generics.

- Market Entry Strategy: Generic manufacturers will compete on price, supply chain reliability, and regulatory approval timelines. The first entrants often capture a larger initial market share.

WHAT ARE THE REGULATORY CONSIDERATIONS FOR GENERIC FINGOLIMOD?

Regulatory approval for generic fingolimod requires demonstrating bioequivalence to the reference listed drug (RLD), Gilenya.

- Bioequivalence Studies: Generic manufacturers must conduct studies to prove that their product is absorbed into the bloodstream at the same rate and extent as Gilenya. This is a standard requirement by regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA).

- Abbreviated New Drug Application (ANDA): In the U.S., generic drug applications are submitted as ANDAs. The FDA's review process assesses efficacy, safety, and quality.

- Marketing Authorization Application (MAA): In Europe, generic applications are submitted as MAAs to national competent authorities or via the centralized procedure, with the EMA coordinating reviews.

- Manufacturing Standards: Generic products must be manufactured in facilities that comply with Good Manufacturing Practices (GMP) as defined by regulatory bodies.

- Labeling Requirements: Generic drug labels must include information comparable to the RLD, while also potentially highlighting any differences.

- Potential for Litigation: While primary patents have expired, originator companies may pursue litigation based on remaining secondary patents. This can delay generic market entry or lead to settlements. For fingolimod, patent litigation has been a factor, but many key patents have now expired, reducing this barrier for broad generic access.

WHAT ARE THE THERAPEUTIC AND CLINICAL IMPLICATIONS?

The availability of generic fingolimod offers significant benefits from a clinical and patient access perspective.

- Increased Patient Access: Lower pricing will make fingolimod therapy accessible to a larger number of patients with relapsing MS, particularly in healthcare systems with budget constraints.

- Treatment Adherence: Cost is a significant barrier to medication adherence. Reduced prices can improve adherence rates, potentially leading to better disease management outcomes for patients.

- Healthcare System Savings: Payers and healthcare systems will benefit from substantial cost savings, which can then be reallocated to other critical areas of healthcare or used to expand access to treatments.

- Clinical Equivalence: Approved generic fingolimod products are clinically equivalent to the branded version, meaning they are expected to have the same therapeutic effect and safety profile. Patients switching from branded to generic fingolimod should experience no difference in treatment efficacy or side effects, provided the generic is bioequivalent and manufactured to high-quality standards.

- Monitoring and Management: The mechanism of action of fingolimod involves modulating sphingosine 1-phosphate receptors, leading to lymphocyte sequestration. Patients require regular monitoring of heart rate, liver function, and ophthalmologic examinations, regardless of whether they are taking the branded or generic product.

WHAT ARE THE FUTURE MARKET TRENDS AND OPPORTUNITIES?

The post-patent expiry landscape for fingolimod presents opportunities and shifts in market focus.

- Generic Market Dominance: The market will be dominated by generic manufacturers competing on price and supply. Opportunities exist for companies with efficient manufacturing and robust distribution networks.

- Lifecycle Management (Branded): Novartis may focus on specific patient support services, enhanced formulation development (if patents allow), or combination therapies to retain some market share for Gilenya. However, significant market retention is unlikely.

- Emerging Markets: Generic fingolimod is expected to see significant uptake in emerging markets where cost is a primary determinant of access.

- Combination Therapy Development: While fingolimod is a well-established monotherapy, ongoing research in MS treatment may explore its use in combination with other disease-modifying therapies. However, the primary focus for generic manufacturers is the established indication.

- Biosimilar Potential (N/A for Fingolimod): Fingolimod is a small molecule drug, not a biologic. Therefore, biosimilar development is not applicable. The market dynamics are driven by generic small molecule competition.

- Supply Chain Optimization: With multiple players, ensuring a stable and reliable supply chain will be crucial for generic manufacturers to gain and maintain market share.

Table 3: Market Opportunities Post-Fingolimod Patent Expiry

| Opportunity Area | Description | Target Audience |

|---|---|---|

| Generic Manufacturing | High-volume production of cost-effective fingolimod generics. | Generic Pharmaceutical Cos |

| Market Penetration | Expanding access in price-sensitive emerging markets. | Generic Marketers |

| Supply Chain Excellence | Ensuring consistent availability and efficient distribution to secure market share. | Logistics & Pharma Cos |

| Differentiated Generics | Potential for niche products based on specific excipients or advanced delivery mechanisms (if patent-protected). | Specialty Generic Cos |

| Payer & Provider Engagement | Negotiating favorable pricing and formulary placement with healthcare systems and insurers. | Sales & Marketing Teams |

KEY TAKEAWAYS

- Primary patents for fingolimod have expired or are expiring globally, facilitating generic market entry.

- Pricing is projected to decrease by 50% to 85% for fingolimod within two years of generic availability.

- The total market value for fingolimod is expected to contract, while treatment volume will increase due to enhanced accessibility and affordability.

- The competitive landscape will shift to a multi-generic market dominated by established and emerging generic manufacturers.

- Regulatory approval hinges on demonstrating bioequivalence, with standard ANDA/MAA processes.

- Generic fingolimod will significantly improve patient access and generate substantial cost savings for healthcare systems.

FREQUENTLY ASKED QUESTIONS

-

When is the last significant patent expiry for fingolimod globally? While specific regional expiry dates vary, the core patent protections and subsequent SPCs in major markets like the U.S. and EU have largely concluded or are in the final stages, with widespread generic entry occurring in 2020-2023.

-

Will branded Gilenya still be available after generic fingolimod is launched? Yes, branded Gilenya will likely remain available, but its market share will significantly decrease as payers and patients opt for lower-cost generic alternatives.

-

Are there any specific side effects associated with switching from branded fingolimod to a generic? If a generic fingolimod product is bioequivalent and approved by regulatory authorities, it is expected to have the same efficacy and safety profile as the branded product. Patients should not experience different side effects solely due to the switch.

-

What is the expected timeline for full generic market saturation for fingolimod? Full market saturation, where generics constitute over 90% of the volume, is anticipated within three to five years following the initial wave of generic approvals and launches in key regions.

-

Beyond price reduction, what other competitive advantages might generic fingolimod manufacturers focus on? Generic manufacturers may also compete on supply chain reliability, ensuring consistent product availability, and potentially on differentiated packaging or patient support services, although price remains the primary competitive driver.

CITATIONS

[1] U.S. Food and Drug Administration. (n.d.). Drug Search. Retrieved from https://www.fda.gov/drugs/drug-approvals-and-databases/drug-list-alphabetical- [2] European Medicines Agency. (n.d.). European public assessment reports (EPARs). Retrieved from https://www.ema.europa.eu/en/medicines/human/EPARs [3] Novartis AG. (2023). Novartis Annual Report 2023. Retrieved from https://www.novartis.com/investors/annual-reports [4] Pharmaceutical research and market analysis reports (Confidential Company Data). (Various Years). [5] National Institute for Health and Care Excellence. (n.d.). NICE guidance. Retrieved from https://www.nice.org.uk/guidance

More… ↓