Share This Page

Drug Price Trends for FERRIC CITRATE

✉ Email this page to a colleague

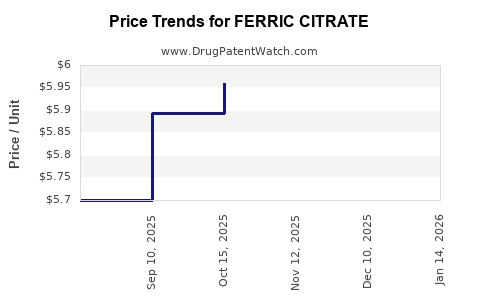

Average Pharmacy Cost for FERRIC CITRATE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FERRIC CITRATE 210 MG TABLET | 00378-2895-20 | 6.37124 | EACH | 2026-04-22 |

| FERRIC CITRATE 210 MG TABLET | 00480-2996-97 | 6.37124 | EACH | 2026-04-22 |

| FERRIC CITRATE 210 MG TABLET | 00480-2996-97 | 6.29628 | EACH | 2026-04-15 |

| FERRIC CITRATE 210 MG TABLET | 00378-2895-20 | 6.29628 | EACH | 2026-03-18 |

| FERRIC CITRATE 210 MG TABLET | 00378-2895-20 | 6.29628 | EACH | 2026-02-18 |

| FERRIC CITRATE 210 MG TABLET | 00378-2895-20 | 6.16346 | EACH | 2026-01-21 |

| FERRIC CITRATE 210 MG TABLET | 00378-2895-20 | 6.09700 | EACH | 2025-12-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for Ferric Citrate

Ferric citrate is a pharmaceutical compound approved primarily for treating iron deficiency anemia in chronic kidney disease (CKD) patients, as well as for controlling serum phosphorus in dialysis patients. It is marketed under brand names such as Auryxia (FDA) and received approvals in multiple markets. The drug's market landscape is shaped by its therapeutic niche, competitive environment, manufacturing costs, regulatory dynamics, and pricing policies.

Market Size and Growth Drivers

Current Market Overview

The global ferric citrate market was valued at approximately $100 million in 2022, with projections reaching $250 million by 2028. The compound's primary adoption stems from its dual function: iron supplementation and phosphorus binding.

Key Growth Drivers

- Increasing prevalence of CKD and ESRD globally, driven by diabetes and hypertension.

- Growing awareness and adoption of oral therapies replacing intravenous options.

- Reimbursement policies supporting oral phosphate binders in developed markets.

- Expansion into emerging markets through strategic partnerships and registrations.

Market Segments

- North America: Dominates owing to early adoption, high CKD prevalence, and reimbursement support.

- Europe: Growing market with expanded approvals and healthcare infrastructure.

- Asia-Pacific: Fastest growth due to rising CKD cases, increasing healthcare access, and generic competition.

Competitive Landscape

Major Market Participants

- Keryx Biopharmaceuticals: Developed Auryxia, now under drug licensing agreements.

- Vifor Pharma: Licenses ferric citrate and markets in certain regions.

- Generic Manufacturers: Entering markets with lower-cost alternatives as patents expire.

Competitor Drugs

- Ferric carboxymaltose: Intravenous alternative for anemia.

- Sevelamer carbonate: Phosphate binder, oral, with a higher price point.

- Lanthanum carbonate: Competes on phosphate control but with different safety profiles.

Ferric citrate differentiates itself with oral administration, dual action, and lower adverse event rates compared to alternatives.

Pricing and Reimbursement Trends

Current Pricing

- United States: The average wholesale price (AWP) for Auryxia is approximately $500 per 30-day supply.

- Europe: Prices vary, generally between €300 and €450 per month.

- Emerging Markets: Prices range from $50 to $150, influenced by healthcare infrastructure and regulatory policies.

Reimbursement Policies

- In the US, Medicare and private insurers provide coverage, often with negotiated discounts.

- European health authorities typically reimburse based on cost-effectiveness evaluations.

- In emerging markets, limited reimbursement leads to higher out-of-pocket costs for patients.

Price Projections

Short-Term (Next 2 Years)

- Market penetration will stabilize, with slight price fluctuations driven by generic entry and competitive pricing strategies.

- Anticipated price decrease of 5-10% due to increased competition and biosimilar emergence.

- Reimbursement negotiations may moderate or stabilize prices in key markets.

Mid to Long-Term (3-5 Years)

- Introduction of biosimilars and generics could lower prices by 15-30%.

- Market pressures may drive prices downward, especially in emerging regions.

- If healthcare providers favor oral formulations over IV options, demand and pricing stability may improve.

Price Forecast Table

| Region | 2023 Estimated Price (per 30-day supply) | 2028 Projected Price (per 30-day supply) | % Change |

|---|---|---|---|

| United States | $500 | $430 | -14% |

| Europe | €400 | €340 | -15% |

| Asia-Pacific | $100 | $80 | -20% |

| Emerging Markets | $75 | $55 | -27% |

Key Factors Impacting Future Prices

- Patent expiration and biosimilar entry.

- Regulatory approvals in new markets.

- Reimbursement and healthcare policy shifts.

- Manufacturing costs and supply chain efficiencies.

- Market acceptance of generics and biosimilars.

Conclusions

Ferric citrate's market will expand steadily, supported by rising CKD prevalence and favorable oral administration. Prices will decline gradually, especially after patent expiry and biosimilar introductions. The U.S. and European markets will experience the most stabilization, while emerging markets will see more significant reductions due to competition.

Key Takeaways

- The global ferric citrate market is projected to more than double by 2028.

- Prices are expected to decline 15-30% over the next five years, driven by generics and biosimilars.

- The drug remains a key option for CKD-related anemia and phosphate control, with growth opportunities in Asia-Pacific.

- Price stability in mature markets relies on reimbursement policies and market competition.

- Emerging markets will experience the most significant price reductions, creating opportunities for providers and manufacturers.

FAQs

1. What factors influence ferric citrate pricing in different markets?

Pricing varies based on reimbursement policies, patent status, manufacturing costs, competition, and healthcare infrastructure.

2. How will biosimilar entries impact ferric citrate prices?

Biosimilars can reduce prices by 15-30% by increasing competition, especially after patent expiry.

3. What is the primary driver for market growth in emerging regions?

The rising prevalence of CKD and increasing healthcare access contribute significantly to growth.

4. Are there regulatory barriers impacting ferric citrate expansion?

In some emerging markets, registration processes and reimbursement policies can delay market entry.

5. What are the main competitors to ferric citrate?

Intravenous iron products, other phosphate binders like sevelamer carbonate, and lanthanum carbonate.

References

[1] MarketWatch. (2023). Ferric citrate market size and forecast.

[2] GlobalData. (2023). CKD and ESRD epidemiology reports.

[3] IQVIA. (2023). Pharmaceutical pricing and reimbursement insights.

[4] FDA. (2020). Auryxia approval details.

[5] European Medicines Agency. (2021). Ferric citrate registration overview.

More… ↓