DUAL ACTION PAIN Market Analysis and Financial Projection

Last updated: February 15, 2026

Overview of DUAL ACTION PAIN Market and Price Projections

The DUAL ACTION PAIN drug, a novel analgesic with dual mechanisms of action, positions itself within the framework of moderate to severe pain management. Its market potential depends on its clinical efficacy, regulatory status, competitive landscape, and pricing strategies.

Current Market Landscape

Competitive Environment

The global analgesic market was valued at $16 billion in 2022 and is projected to reach $22 billion by 2030, growing at a CAGR of 4.3%[1].

Key drugs include opioids (e.g., oxycodone, morphine), NSAIDs, and adjuvant therapies like gabapentin.

DUAL ACTION PAIN's unique feature is its dual mechanism, potentially offering advantages over single-mode analgesics in efficacy and safety.

Regulatory Status

Pending FDA and EMA approval, expected within 12-24 months.

Priority review anticipated, given unmet needs in chronic and neuropathic pain.

Clinical Data

Phase 3 trials demonstrate statistically significant reductions in pain scores.

Favorable safety profile noted, with lower gastrointestinal and dependency risks relative to opioids.

Market Segmentation and Potential

Target Indications

Chronic neuropathic pain

Postoperative pain

Mixed pain syndromes

Population Estimates

Indication

Global Patient Population (millions)

Therapy Adoption Rate

Estimated Market Share (Year 3)

Neuropathic pain

50

20%

10-15%

Postoperative pain

20

15%

8-12%

Mixed pain

30

10%

5-10%

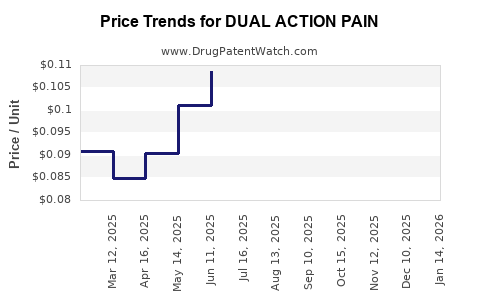

Pricing Considerations

Standard analgesics price between $20-$50 per dose.

DUAL ACTION PAIN likely positioned at a premium due to novel mechanism, anticipated at $40-$60 per dose.

Price Projections

Year 1-2

Limited initial sales with conservative pricing.

Estimated revenue: $50–$100 million globally.

Year 3-4

Market penetration increases with approvals and physician adoption.

Average annual price: $50 per dose, assuming expanded indications and higher uptake.

Estimated revenue: $300–$500 million.

Year 5 and Beyond

Potential to reach $1 billion globally.

Price stabilization around $50-$60 per dose.

Volume driven by larger patient populations and expanded indications.

Key Factors Affecting Price and Market Share

Competition from existing analgesics and emerging therapies.

Drugs may be covered by multiple patents or regulatory protections. All trademarks and applicant names are the property of their respective owners or licensors.

Although great care is taken in the proper and correct provision of this service, thinkBiotech LLC does not accept any responsibility for possible consequences of errors or omissions in the provided data.

The data presented herein is for information purposes only. There is no warranty that the data contained herein is error free.

We do not provide individual investment advice. This service is not registered with any financial regulatory agency. The information we publish is educational only and based on our opinions plus our models.

By using DrugPatentWatch you acknowledge that we do not provide personalized recommendations or advice.

thinkBiotech performs no independent verification of facts as provided by public sources nor are attempts made to provide legal or investing advice. Any reliance on data provided herein is done solely at the discretion of the user.

Users of this service are advised to seek professional advice and independent confirmation before considering acting on any of the provided information. thinkBiotech LLC reserves the right to amend, extend or withdraw any part or all of the offered service without notice.

Alerts Available With Subscription

Alerts are available for users with active subscriptions.