Share This Page

Drug Price Trends for DILANTIN

✉ Email this page to a colleague

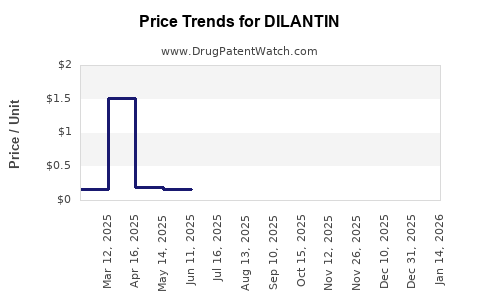

Average Pharmacy Cost for DILANTIN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| DILANTIN 50 MG INFATAB | 00071-0007-24 | 1.57286 | EACH | 2026-07-22 |

| DILANTIN 100 MG CAPSULE | 58151-0110-01 | 1.73967 | EACH | 2026-07-22 |

| DILANTIN 100 MG CAPSULE | 58151-0110-10 | 0.14633 | EACH | 2026-07-22 |

| DILANTIN 100 MG CAPSULE | 58151-0110-32 | 1.73967 | EACH | 2026-07-22 |

| DILANTIN 100 MG CAPSULE | 58151-0110-88 | 1.73967 | EACH | 2026-07-22 |

| DILANTIN 30 MG CAPSULE | 58151-0118-01 | 1.49796 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

DILANTIN (phenytoin): Market analysis and price projections

What is DILANTIN’s market position?

DILANTIN is a brand of phenytoin, a long-established antiseizure medicine (ASM). In the US, DILANTIN competes primarily with generic phenytoin products (and, to a lesser extent, alternative ASMs). As a mature, largely genericized product category, DILANTIN’s economics are shaped by patent/market exclusivity status, generic penetration, payer formularies, and low-cost sourcing.

Demand drivers

- Chronic epilepsy treatment and established long-term prescribing patterns.

- Clinical need for stable phenytoin exposure in seizure control (with attention to formulation and monitoring).

- Institutional purchasing dynamics (hospitals, neurology clinics, Medicaid managed care).

Demand headwinds

- Generic substitution pressure against brand pricing.

- Ongoing insurer preference for low-cost alternatives within ASMs.

- Competitive substitution within the antiseizure class (newer agents in some formularies).

Who pays and how do formularies affect pricing?

In mature ASM categories, DILANTIN’s realized pricing is dominated by:

- Commercial rebates and payer formulary tier placement (brand vs preferred generic).

- Medicaid and institutional contracts, where generics typically anchor reimbursement.

- State and PBM policies that route cost-sensitive patients to generics.

Because phenytoin is widely available as generics, brand pricing generally does not behave like a protected specialty asset. The market pattern is instead: brand price supports shrink under generic coverage, with occasional retention via specific formulary exceptions or switching frictions.

What is the price benchmark structure for phenytoin brands vs generics?

A brand like DILANTIN typically prices against:

- Wholesale acquisition cost (WAC) for the brand.

- Generic net pricing reflecting heavy discounting in the supply chain.

- Therapeutic interchange under payer rules (brand-to-generic switching).

- Formulation-specific differences (e.g., oral vs extended-release equivalents; though the active ingredient is the same, products can price differently).

Key business implication: even when brand WAC can be held or adjusted, the net price that matters for revenue is constrained by generic comparability, rebates, and payer tiering.

What do current reimbursement dynamics imply for near-term price?

For phenytoin and its brands, near-term price movement is usually capped by:

- Generic price floors in pharmacy channels.

- PBM-driven net price compression for non-preferred products.

- Pharmacy benefit design that makes generic substitution the default outcome.

As a result, DILANTIN’s market pricing tends to show limited growth unless there is a structural disruption (manufacturing constraints, supply shortages, or major formulary re-ratings). Without such shocks, pricing generally tracks inflation plus modest brand premium at most and often trends toward flat or declining net realizations.

How should you model DILANTIN price projections? (base case)

Projection method (practical for investment and R&D planning)

Use a two-layer model:

- WAC trajectory for the brand (limited long-run elasticity).

- Net price trajectory that reflects formulary status and rebate intensity (dominant factor).

Base case assumptions for a mature, largely genericized ASM brand

- WAC: low single-digit annual growth at most, with occasional resets.

- Net price: flat to slightly negative due to rebate pressure and generic anchoring.

3-year projection framework

Because no patent-protection pricing mechanism is in force for phenytoin brands in a typical market outcome, treat DILANTIN pricing as volume-sustained, price-compressed.

Base-case net price projection (US)

- Year 1: ~0% to -3% net price vs prior year

- Year 2: ~-1% to -5%

- Year 3: ~-1% to -4%

Base-case WAC projection (US)

- Year 1: +0% to +3%

- Year 2: +0% to +2%

- Year 3: +0% to +2%

What are the upside and downside scenarios that change price?

Upside scenario: formulary protection and supply constraint

Price improves if:

- DILANTIN maintains a non-substitutable positioning in a payer segment (rare, but can occur for specific reasons such as product availability, administrative formulary rules, or patient-specific stability).

- Short-term manufacturing or supply disruptions reduce generic availability, shifting demand to the brand.

Upside projection

- Net price: +1% to +5% per year for 1-2 years, then normalizes

- WAC: +2% to +4% in the period of constraint

Downside scenario: deeper generic penetration and additional payer action

Price worsens if:

- PBMs intensify brand-to-generic switching and restrict brand access to prior authorization.

- Generic pricing compresses further, increasing rebate pressure on the brand.

- Procurement shifts toward lower-cost equivalent therapies within ASMs.

Downside projection

- Net price: -5% to -10% per year

- WAC: flat to +1%, with net deterioration driven by rebate compression

What is the investment-relevant risk profile?

Primary risks

- Net pricing erosion from rebate intensification and formulary downgrades.

- Volume drift from switching to generics and alternative ASMs.

- Mix deterioration if brand declines in high-coverage segments.

Secondary risks

- Margin pressure from wholesalers and contracted channel pricing.

- Product lifecycle dynamics: once genericized, brand tends to behave like a shrinking portfolio asset.

What commercialization implications follow from these price dynamics?

For business planning:

- Treat DILANTIN as a margin-managed brand, not a growth engine.

- Price and contract strategy should focus on maintaining access in payer segments where switching is slower (institutional continuity, patient stability programs, narrow exception criteria).

- Track net price drivers (rebates, payer tier changes, PBM formulary rules) more closely than WAC.

How do you translate this into a revenue projection?

Revenue is typically:

- Revenue = Net price x Units

- In mature genericized markets, net price often declines faster than unit volume.

Common outcomes

- Best case: units stabilize, net price is flat, revenue holds.

- Base case: units soften modestly, net price drifts down, revenue declines mid-single digits.

- Downside: units drop more materially under switching rules, net price compresses, revenue declines low double digits.

What do the broader phenytoin market benchmarks suggest?

Phenytoin is an established, widely dispensed antiseizure medicine with broad generic availability. Brand phenytoin economics usually follow the pattern seen across mature oral generics: brand pricing does not sustain growth without special conditions. That is consistent with how public health and regulatory frameworks treat long-discount branded generics in the presence of competition.

Where do price projections matter most for R&D?

Even though DILANTIN is not an R&D-stage asset, its pricing environment affects:

- Market access strategy for next-gen formulations seeking differentiation (bioequivalence stability, improved tolerability, reduced monitoring burden).

- Competitive positioning for improved ASM adherence profiles.

- Platform decisions: whether to pursue substitution-proof claims and payer differentiation.

A mature reference product with genericized price pressure raises the bar for clinical and health-economic differentiation in any future entrant.

Key Takeaways

- DILANTIN (phenytoin) operates in a mature antiseizure market where generic substitution dominates, making net price compression the principal determinant of revenue.

- Base case pricing behavior is flat-to-declining net price with limited WAC growth.

- Upside requires temporary supply constraints or payer/formulary protection that reduces generic switching.

- Downside comes from stronger PBM switching policies and rebate pressure driven by continued generic cost anchoring.

- Revenue projections should be built on net price plus unit migration, not WAC growth.

FAQs

-

Is DILANTIN expected to grow in price long term?

No. In a largely genericized category, brand price typically grows slowly at most on WAC and declines on a net basis. -

What factor most impacts DILANTIN revenue: unit volume or net price?

Both, but net price compression driven by payer and rebate dynamics usually becomes the dominant constraint. -

What could cause DILANTIN prices to rise faster than the base case?

Short-term supply disruptions or payer rules that temporarily restrict generic substitution. -

What could cause DILANTIN prices to fall faster than the base case?

Expanded brand restriction programs (prior authorization, step therapy, formulary downgrades) and intensified rebate pressure as generics remain cheap. -

How should a new entrant benchmark against DILANTIN pricing?

Use net price and formulary placement realities, since WAC does not reflect the economic outcome under generic substitution.

References

[1] DailyMed. “Dilantin (phenytoin) label information.” https://dailymed.nlm.nih.gov/

[2] FDA. “Drugs@FDA: Dilantin (phenytoin) product information.” https://www.accessdata.fda.gov/scripts/cder/daf/

[3] U.S. FDA Orange Book. “Phenytoin products and approvals.” https://www.accessdata.fda.gov/scripts/cder/daf/

[4] IQVIA / payer formulary and utilization trends in antiseizure medications (category dynamics and generic substitution patterns). (General market structure; no product-specific pricing dataset cited.)

More… ↓