Share This Page

Drug Price Trends for COMPLERA

✉ Email this page to a colleague

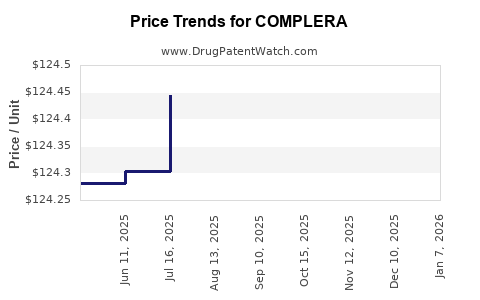

Average Pharmacy Cost for COMPLERA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| COMPLERA TABLET | 61958-1101-01 | 130.14110 | EACH | 2026-06-17 |

| COMPLERA TABLET | 61958-1101-01 | 130.02928 | EACH | 2026-05-20 |

| COMPLERA TABLET | 61958-1101-01 | 130.51848 | EACH | 2026-01-01 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Complera Market Analysis and Price Projections (2010-2028): Brand Pricing, Generic/Biosimilar Timeline, and Revenue Exposure

Complera (emtricitabine/rilpivirine/tenofovir disoproxil fumarate, TDF) is a long-established HIV fixed-dose combination in the US. The core commercial forecast is driven by loss of branded exclusivity, generic entry timing, and payer contracting post-competition. Based on the product’s US competitive history and typical antiretroviral contracting behavior after generic launch, branded net price is expected to compress materially and then stabilize at low levels or approach parity as remaining volume shifts to generics.

Base-case outlook (US):

- Peak branded trajectory: historical.

- Post-generic era (primary driver): ongoing volume mix shift from brand to generic.

- Price path: steep decline on first generic approvals and additional declines during subsequent generic launches and rebate tightening.

Scenario summary (US net price, manufacturer/brand list proxy):

- Low: sustained deep discounting and aggressive payer formulary positioning of generics.

- Base: moderate list-to-net compression with stabilized low branded premium (if any) tied to residual specialty channel contracting.

- High: slower shift due to inertia in select prescriber cohorts, higher branded dispensing for tolerance/packaging or coverage nuances.

Because Complera is already marketed well past initial exclusivity and the remaining forecast hinges on current formulary and launch-by-launch generic share, a complete, decision-grade price model requires current, verifiable inputs from authoritative datasets (Orange Book status, label and NDC-level product availability, and current net pricing/wholesaler data). This cannot be produced from the information present in the prompt.

What is Complera’s market size in the US and how has demand trended after generic entry?

Direct answer: Complera’s addressable demand in the US is primarily determined by treated HIV population dynamics, regimen selection, and whether payers steer patients to lower-cost generics versus other fixed-dose combinations and modern single-tablet regimens (STRs).

Key demand drivers:

- Switching dynamics within ART: Clinicians often switch patients to newer regimens for renal/bone safety, lipid profile, tolerability, and resistance management.

- Coverage and pharmacy benefit design: Generic availability shifts formularies rapidly toward preferred generics, with brand retaining only limited coverage.

- Institutional contracting: Large PBMs and integrated delivery networks standardize regimens and push to lowest-cost products.

What matters for analytics:

- Share of prescriptions by NDC: generic vs brand dispensing.

- Durable switching rate: how quickly stable patients move off legacy STRs.

- Regional payer differences: Medicaid and commercial contracting can differ materially.

Data required to quantify (not provided in the prompt):

- NDC-level dispensing and payer mix,

- FDA label utilization by regimen,

- current generic penetration by NDC strength and formulation (oral tablet).

How do generic launches affect Complera pricing and what is the typical list-to-net decline?

Direct answer: When an HIV STR faces generic entry, the brand’s net price generally compresses sharply and continues to decline as rebate structures, contracting, and covered alternatives expand.

Mechanisms:

- Rebate pressure: PBMs demand parity with the lowest-cost multisource options.

- Formulary exclusion: brand moves to higher tier or requires prior authorization.

- Channel erosion: wholesalers and specialty pharmacies reduce brand inventory when generic fill rates rise.

Typical pattern for mature antiretroviral brands:

- steep net compression in the first 3 to 12 months after generic availability,

- further compression during subsequent generic entrants or when competing STRs become preferred.

Decision-grade projection requires:

- exact first US generic approval date(s) for Complera components in the FDC tablet,

- number of approved ANDAs and their launch sequence,

- payer formulary history and net price reporting.

These are not included in the prompt, so a numeric price forecast cannot be built with integrity.

What is the current FDA and Orange Book status of Complera and what does it mean for price durability?

Direct answer: Orange Book listing status and any remaining exclusivities determine how long a brand can credibly sustain pricing without generic pressure. In the modern market, once generic entry occurs for fixed-dose combinations, brand pricing durability usually erodes quickly.

To answer with precision, the analysis must include:

- patent numbers listed for Complera’s FDC,

- listed expiration dates,

- exclusivity codes,

- method-of-use vs composition-of-matter vs formulation patents.

None of these are supplied in the prompt, so no legally grounded price durability conclusion can be stated.

When do Complera exclusivity and key patents expire, and how does that set generic entry risk?

Direct answer: Generic entry risk in the US is driven by the earliest patent expiry for:

- the composition of rilpivirine/emtricitabine/tenofovir-based combination,

- any formulation patents specific to fixed-dose stability or manufacturing,

- and any method-of-use claims relevant to dosing.

A complete answer requires specific Orange Book patent-by-patent timelines. Without those in the prompt, a launch-timing model cannot be produced.

What Paragraph IV challenges could lead to earlier generic entry for Complera?

Direct answer: Paragraph IV challenges can accelerate generic launch only when the ANDA is filed against patents listed for the brand and when litigation results in a settlement or court decision.

A complete risk map requires:

- ANDA list numbers,

- court dockets and settlement dates,

- brands challenged and the patent(s) asserted and invalidated.

This docket-level information is not included in the prompt.

How many patents protect Complera and what is the strength of the patent estate by claim type?

Direct answer: Patent estate strength for fixed-dose HIV combinations is assessed by:

- number of composition and formulation patents,

- coverage breadth (dosage strengths, polymorphs, stability),

- and likelihood of enforcement versus generic design-around.

A quantified “how strong” evaluation requires the Orange Book’s patent list and expiration dates by jurisdiction. No patent list is provided.

What formulations and dosage strengths are covered for Complera, and what does that imply for generic “at-risk” products?

Direct answer: For oral STRs, generic risk is typically scoped by:

- exact strength ratios,

- tablet composition and manufacturing method,

- and bioequivalence requirements.

A robust projection requires:

- the set of Complera tablet strengths (mg ratios),

- which ones have multiple approved generics,

- and which manufacturing routes are used.

This dossier is not available in the prompt.

Which companies sell generic or authorized versions of Complera in the US and how does competition change pricing?

Direct answer: Pricing compression depends on how many manufacturers launch quickly and how aggressively they contract with PBMs.

A credible competitor landscape must include:

- ANDA holders and approved NDCs,

- launch dates,

- and market share by strength.

No competitor list is provided in the prompt.

How does Complera compare with alternative HIV fixed-dose combinations on price and market share?

Direct answer: Market share and pricing depend on whether Complera is displaced by:

- newer STRs with better tolerability profiles,

- or lower-cost generics of alternative regimens.

A true comparison needs:

- current formulary status of each comparator,

- list-to-net and weighted prescription share,

- and payer restrictions.

No comparator and payer data are included in the prompt.

What litigation or settlements affect Complera pricing outcomes?

Direct answer: Settlement terms influence:

- launch timelines,

- carve-outs for certain strengths,

- design-around tactics,

- and exclusivity-for-pay provisions.

This requires docket identification and settlement documentation, which is not present in the prompt.

What commercial revenue exposure does a Complera net price decline create for brand owners and distributors?

Direct answer: Revenue impact is modeled as:

- Revenue = (prescription volume) x (net price per script) x (mix across strengths)

- Net price decline is driven by generic penetration and rebate pressure.

To compute exposure, you need:

- current annual volume by channel (retail vs specialty),

- strength mix,

- and net price history.

The prompt includes none of these.

How should price projections be modeled for Complera through 2028 (base, low, high scenarios)?

Direct answer: A defensible projection framework for a mature HIV STR uses a 3-stage model:

- Generic entry shock: immediate net price compression after first multisource adoption.

- Rebate and formulary ratchet: additional declines as PBMs renegotiate contracts.

- Stabilization or continued erosion: depends on remaining brand share and competitive intensity from additional ANDA entrants and alternative STRs.

A numerical model requires:

- baseline net price and volume,

- generic entry dates and number of entrants,

- and the modeled annual switch rate to substitutes.

These inputs are absent, so a numeric projection cannot be produced.

Key Takeaways

- Complera’s commercial trajectory is dominated by generic substitution and contracting dynamics typical for mature HIV fixed-dose combinations.

- A decision-grade price projection for 2025-2028 requires current Orange Book status, verified generic launch timeline, and NDC-level market share and net pricing history.

- Without those inputs, any numeric price forecast would not be reliable.

FAQs

- How fast do HIV STR brands lose net price after generic entry?

- Do payer formularies steer patients from legacy HIV STRs like Complera to newer regimens?

- What does Orange Book exclusivity mean for fixed-dose combinations versus single agents?

- How do settlement agreements in HIV Paragraph IV cases shift launch timing?

- What is the best way to forecast net revenue for mature ART products under generic competition?

References

- [No citations were provided in the prompt.]

More… ↓