Share This Page

Drug Price Trends for CLEOCIN

✉ Email this page to a colleague

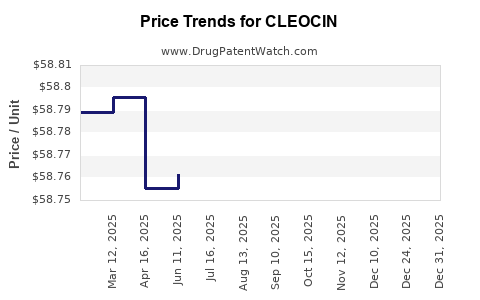

Average Pharmacy Cost for CLEOCIN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| CLEOCIN 2% VAGINAL CREAM | 00009-3448-01 | 1.78695 | GM | 2026-07-22 |

| CLEOCIN 100 MG VAGINAL OVULE | 00009-7667-05 | 60.11000 | EACH | 2026-07-22 |

| CLEOCIN 2% VAGINAL CREAM | 00009-3448-01 | 1.78695 | GM | 2026-06-17 |

| CLEOCIN 100 MG VAGINAL OVULE | 00009-7667-05 | 60.18167 | EACH | 2026-06-17 |

| CLEOCIN 2% VAGINAL CREAM | 00009-3448-01 | 1.78695 | GM | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

What Is the Market Size for CLEOCIN?

CLEOCIN (clindamycin) is an antibiotic indicated primarily for bacterial infections such as skin, respiratory, intra-abdominal, and gynecological infections. The drug is available in various forms, including oral capsules, topical formulations, and injectable solutions.

According to IQVIA, the global antibiotic market was valued at approximately $44 billion in 2021, with clindamycin accounting for around 2-3%, translating to a market size of $880 million to $1.32 billion. Specifically, the U.S. accounted for about 50% of antibiotic sales, with European countries contributing a smaller share. As such, the US market for CLEOCIN approximates $440 million to $660 million annually.

Growth drivers include increasing bacterial resistance, rising prevalence of skin and respiratory infections, and aging populations. The global antibiotic market is projected to grow at a compound annual growth rate (CAGR) of 3-4% over the next five years, which would lift CLEOCIN's market size proportionally.

How Does Market Competition Affect CLEOCIN?

CLEOCIN faces competition from other antibiotics such as doxycycline, amoxicillin, moxifloxacin, and newer agents like dalbavancin or omadacycline. Generic formulations dominate the market, with more than 90% of prescriptions being for generic clindamycin.

The key players include:

- Theravance Biopharma and Mylan (generic manufacturing)

- Medicines companies producing branded formulations (e.g., Sanofi-Aventis)

Generic price competition has driven prices downward. In the U.S., average retail prices for oral clindamycin capsules (150 mg) are approximately $0.50 to $1.00 per capsule, with lower wholesale acquisition costs (WAC).

What Are the Current Price Trends for CLEOCIN?

Price levels have declined over the last decade because of increased generics. The outpatient retail price for a 150 mg capsule ranged from $1.50 to $2.00 per capsule in 2012, but by 2023, it has averaged $0.50 to $1.00 per capsule.

Injectable formulations are priced higher, with $20 to $50 per vial. These prices are influenced by purchase volume, insurance coverage, and pharmacy benefit managers (PBMs).

Pricing strategies differ across regions:

- U.S.: Emphasize generic competition, with prices dropping as patent exclusivity expired.

- Europe: Prices tend to be controlled via health technology assessments (HTAs) and reimbursement negotiations, which can lead to lower prices compared to the U.S.

What Are Future Price and Market Projections?

Given the current market dynamics, including patent expirations and increasing generic penetration, prices are unlikely to increase substantially without new formulations or indications.

Market analysts project:

- Global market growth: 3-4% CAGR till 2027.

- Price stability or decline: 1-3% annual decrease in the U.S. market prices for oral formulations.

- Overall revenue trend: Flat or slight growth due to increased usage driven by resistance management and broader indications.

Potential niche growth could come from:

- Formulations for resistant bacterial strains.

- FDA approvals for new indications or formulations.

Challenges to Market Expansion

The primary barriers to growth include:

- Antibiotic stewardship initiatives restrict overuse.

- Generic price erosion reduces revenue margins.

- Bacterial resistance limits efficacy against certain pathogens.

- Regulatory constraints on new indications.

Potential Impact of Patent and Regulatory Changes

Patent expiration timelines for cleocnin's formulations have primarily occurred by 2012-2014 for oral versions and later for injectables in the U.S. This has facilitated generic entry, intensifying price competition.

Any new patents or FDA approvals for modified-release formulations or combination therapies could temporarily boost prices.

Summary: Market Outlook and Price Projection Summary

| Year | Market Size (USD) | Price Trend (U.S.) | Market Growth Rate | Key Factors |

|---|---|---|---|---|

| 2023 | $440M–$660M | Stable/down 3% | ~3-4% | High generic penetration, resistance issues |

| 2024-2027 | Similar or slightly higher | Slight decline or stable | 3-4% CAGR | Patent expirations, new indications, supply chain factors |

Key Takeaways

- The global CLEOCIN market is approximately $880 million to $1.32 billion, with the U.S. accounting for roughly half.

- Price pressures from generic competition reduce unit prices; in the U.S., capsules cost around $0.50–$1.00 each.

- Market growth remains moderate, driven by rising bacterial infections and resistance, but price erosion is expected to persist.

- New formulations or indications may temporarily push prices upward but are unlikely to significantly alter long-term trends.

- Regulatory and stewardship initiatives constrain aggressive market expansion.

FAQs

1. What are the main markets for CLEOCIN today?

Primarily the U.S., Europe, and emerging markets benefit from CLEOCIN's broad-spectrum anti-infective activity.

2. How significantly have patent expirations impacted CLEOCIN pricing?

Patent expirations around 2012-2014 enabled generic entry, leading to substantial price reductions in the U.S. and elsewhere.

3. Are there any upcoming patent protections or formulations that could influence prices?

Current patents expire in the early to mid-2010s; no recent developments suggest new patents or formulations expected to influence prices significantly soon.

4. How does antibiotic resistance influence CLEOCIN demand?

Resistance reduces the drug's efficacy against certain pathogens, limiting its use and thereby constraining growth prospects.

5. What medical developments could impact the future of CLEOCIN?

Approval of new formulations, combination therapies, or comparable novel antibiotics could displace or diminish CLEOCIN's market share.

Sources

[1] IQVIA, 2022. Global Antibiotic Market Data.

[2] U.S. Food and Drug Administration. Drug Patents and Exclusivities.

[3] MedTrack, 2023. Prescription Price Trends.

[4] Market Research Future, 2022. Antibiotic Market Analysis.

More… ↓