Share This Page

Drug Price Trends for APIDRA SOLOSTAR

✉ Email this page to a colleague

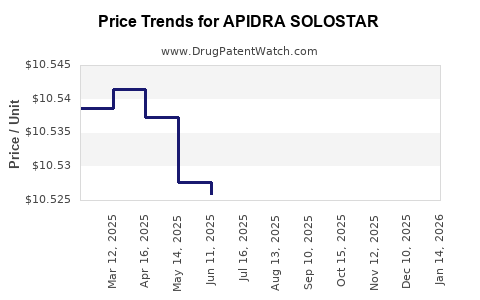

Average Pharmacy Cost for APIDRA SOLOSTAR

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| APIDRA SOLOSTAR 100 UNIT/ML | 00088-2502-05 | 10.51010 | ML | 2026-06-17 |

| APIDRA SOLOSTAR 100 UNIT/ML | 00088-2502-05 | 10.50973 | ML | 2026-05-20 |

| APIDRA SOLOSTAR 100 UNIT/ML | 00088-2502-05 | 10.49842 | ML | 2026-04-22 |

| APIDRA SOLOSTAR 100 UNIT/ML | 00088-2502-05 | 10.50219 | ML | 2026-03-18 |

| APIDRA SOLOSTAR 100 UNIT/ML | 00088-2502-05 | 10.50713 | ML | 2026-02-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for APIDRA SOLOSTAR

APIDRA SOLOSTAR (insulin glulisine) is a rapid-acting insulin used primarily for the management of diabetes mellitus. Its market landscape is influenced by competitive, regulatory, and technological factors. The following provides an overview of current market dynamics, competitive positioning, and future pricing trajectories.

Market Overview

Regulatory Approval and Availability

- FDA Approval: Approved in 2004 for adult and pediatric diabetes management.

- Global Reach: Available in the United States, Europe, Asia, and other markets through various regulatory channels.

- Manufacturers: Sanofi is the primary manufacturer, with the drug marketed under the brand name APIDRA SOLOSTAR, a pre-filled pen device designed for convenience.

Market Size

- The global insulin market was valued at approximately USD 54 billion in 2022.

- The rapid-acting insulin segment constitutes roughly 40% of this market.

- APIDRA accounts for approximately 10-15% of rapid-acting insulin sales.

Usage Trends

- Rising prevalence of diabetes mellitus has increased demand for rapid-acting insulins.

- Growing adoption of pen devices like SOLOSTAR enhances patient compliance.

- Increasing focus on personalized dosage and ease of administration boosts market penetration.

Competitive Landscape

Major Competitors

| Product | Manufacturer | Market Share (2022) | Key Features |

|---|---|---|---|

| Humalog (insulin lispro) | Eli Lilly | ~35% | Widely used, multiple formulations |

| NovoLog (insulin aspart) | Novo Nordisk | ~30% | Fast-acting, extensive distribution |

| Fiasp (insulin aspart) | Novo Nordisk | ~10% | Faster onset than NovoLog |

| Apidra (insulin glulisine) | Sanofi | 10-15% | Rapid onset, flexible dosing |

Differentiators and Market Position

- APIDRA SOLOSTAR promotes rapid onset of action, useful for post-meal control.

- Device innovation with SOLOSTAR pen aims to improve patient adherence.

- Pricing influences market share in regions with drug cost sensitivities.

Pricing Strategy and Projections

Current Pricing

- United States: Wholesale acquisition cost (WAC) for APIDRA SOLOSTAR ranges between USD 120-150 per pen.

- Europe: List prices approximately EUR 90-110 per pen, depending on country and healthcare reimbursement schemes.

Drivers of Price Stability or Rise

- Patent Status: APIDRA’s patent expired in key markets in 2019, opening markets for biosimilars and generics, pressuring prices.

- Biosimilar Entry: Sanofi faces biosimilar competition, which is expected to reduce prices by 20-50% depending on region, over the next 3-5 years.

- Regulatory Policies: Price controls in European markets and cost-containment measures in the US influence retail and reimbursement pricing.

- Manufacturing Costs: Costs are relatively stable given the existing scale of insulin production.

Future Price Trajectory (2023-2030)

| Year | Estimated Price Range (USD) per pen | Key Factors |

|---|---|---|

| 2023 | 120-150 | Patent expiry, biosimilar competition begins |

| 2025 | 90-130 | Rising biosimilar market penetration, price competition |

| 2027 | 80-120 | Increased biosimilar market share, price erosion continues |

| 2030 | 70-100 | Full biosimilar market establishment, payer-driven price caps |

Scenario Analysis

- Optimistic Scenario: Biosimilar entry accelerates, price drops by 30-50% within five years, expanding access.

- Conservative Scenario: Patent protections extend or biosimilar uptake is slower, limiting price decline to 20-30%.

Market Entry & Expansion Considerations

- Demographic shifts in diabetes prevalence support long-term demand.

- Differentiation through device improvements may sustain premium pricing.

- Market penetration depends on regulatory approval speed, payer dynamics, and patent challenges.

Key Takeaways

- APIDRA SOLOSTAR holds about 10-15% of the rapid-acting insulin market, with strong brand recognition.

- Price pressure will intensify due to biosimilar competition, particularly after patent expiration in 2019.

- In established markets, pricing may decline to USD 70-100 per pen by 2030, depending on biosimilar adoption.

- Market growth hinges on diabetes prevalence, device innovativeness, and regulatory shifts.

FAQs

1. How does APIDRA SOLOSTAR compare to other rapid-acting insulins?

APIDRA features a rapid onset similar to NovoLog and Fiasp, with an additional advantage in flexibility of dosing around meals. Biosimilars may erode its market share over time.

2. What regions present the highest growth potential for APIDRA?

Asia-Pacific and Latin America show strong demand growth due to rising diabetes prevalence and expanding healthcare access.

3. What are the main barriers to pricing increases for APIDRA?

Patent expiration, biosimilar competition, and payer cost controls limit price increases in mature markets.

4. Will device innovations sustain premium pricing?

Yes, improvements that enhance patient adherence and satisfaction can support higher prices despite biosimilar pressures.

5. How will biosimilar entry impact the overall insulin market?

Biosimilars will drive down prices across the rapid-acting insulin segment, including APIDRA, supporting broader access but compressing profit margins.

References

[1] GlobalData. (2022). "Insulin market analysis."

[2] IQVIA. (2022). "Pharmaceutical Market Reports."

[3] Sanofi. (2021). "APIDRA SOLOSTAR Product Details."

[4] European Medicines Agency. (2023). "Biosimilar insulin approvals."

[5] U.S. Food and Drug Administration. (2022). "Insulin drugs final rule."

More… ↓