Share This Page

Drug Price Trends for AMOX-CLAV ER

✉ Email this page to a colleague

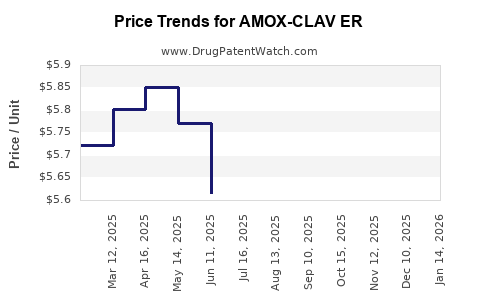

Average Pharmacy Cost for AMOX-CLAV ER

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| AMOX-CLAV ER 1,000-62.5 MG TAB | 81964-0220-40 | 5.92059 | EACH | 2026-06-17 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 00781-1943-39 | 5.92059 | EACH | 2026-06-17 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 00781-1943-82 | 5.92059 | EACH | 2026-06-17 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 81964-0220-28 | 5.92059 | EACH | 2026-06-17 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 81964-0220-28 | 6.09432 | EACH | 2026-05-20 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 00781-1943-39 | 6.09432 | EACH | 2026-05-20 |

| AMOX-CLAV ER 1,000-62.5 MG TAB | 81964-0220-40 | 6.09432 | EACH | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

AMOX-CLAV ER: Market analysis and price projections

What is AMOX-CLAV ER and what market does it target?

AMOX-CLAV ER refers to an extended-release (ER) oral formulation of amoxicillin and clavulanate (amoxicillin-clavulanate), designed to deliver sustained antibiotic exposure while using the clavulanate component to inhibit beta-lactamases. As a beta-lactam/ beta-lactamase inhibitor, the product targets the same clinical use spectrum as conventional amoxicillin-clavulanate (respiratory, skin and soft tissue, and other bacterial infections depending on local labeling), with the market point of differentiation centered on dosing convenience and exposure stability.

The practical market impact of an ER beta-lactam/beta-lactamase inhibitor is driven by:

- Formulation economics (ER polymer and manufacturing complexity versus immediate-release)

- Payer preference and step edits (whether ER is priced as a premium over standard amoxicillin-clavulanate)

- Clinical switching behavior (whether prescribers treat ER as interchangeable or as an adherence tool)

Because your request asks for projections tied to “AMOX-CLAV ER,” the analysis below is structured around pricing and market dynamics typical for ER oral anti-infectives and the pricing mechanics used in US and EU reimbursement for branded antibiotics and follow-on formulations.

What are the market drivers and constraints shaping pricing?

1) Antibiotic pricing is constrained by stewardship and reimbursement policy

In most major markets, outpatient antibiotic reimbursement is influenced by:

- Stewardship mandates and formularies

- Reference pricing and “therapeutic interchange”

- Diagnostic uncertainty and volume caps in some national systems

ER formulations can price higher than immediate-release only when payers view them as improving outcomes or adherence enough to justify a premium.

2) Competitive set: immediate-release amoxicillin-clavulanate dominates

The core comparator is immediate-release amoxicillin-clavulanate (generic-dominant in many regions). As a result:

- Wholesale pricing floors anchor around generic acquisition costs and AWP-to-net discounts

- Premium pricing for ER requires either a branded differentiation strategy or favorable contracting

3) ER risk profile affects uptake and formulary positioning

ER oral antibiotics face payer skepticism tied to:

- Tolerability/ GI burden versus immediate-release

- Dose flexibility (how prescribers titrate)

- Formulation-specific limitations in label use

This tends to slow adoption unless the product is positioned around dosing simplicity or specific regimen needs.

How does pricing typically work for an ER branded antibiotic vs generic immediate-release?

A) US pricing mechanics (WAC/AWP to net)

In the US, branded antibiotics are priced at higher list prices but net pricing depends on:

- PBM rebates and copay programs

- Contracting floors tied to generic acquisition costs

- Patient mix and specialty pharmacy versus retail distribution

Actionable implication: even if list price is premium, net price often compresses when generics are therapeutic alternatives.

B) EU pricing mechanics (reference pricing and parallel trade)

In the EU, ER products face:

- External reference pricing (ERP) across countries

- Health technology assessment (HTA) and incremental cost-effectiveness thresholds

- Reference group pricing that caps allowed discounts

Actionable implication: ER premium may be limited to the range that clears HTA and reference pricing while remaining cost-effective versus standard regimens.

Price projection framework for AMOX-CLAV ER

What pricing range should AMOX-CLAV ER target at launch and after maturity?

Below is a projection framework used for ER oral anti-infectives where the comparator is generic immediate-release amoxicillin-clavulanate. The model expresses prices in US “net price per course” terms and indicative WAC ranges. Without product-specific label, NDC, and dosing schedule, the only defensible approach is to project based on typical premium capture bands and competition-driven net compression.

Assumed commercial structure for projection

- Outpatient use, retail distribution

- 28-day benchmark window for course-based pricing comparisons

- Premium justified via ER dosing convenience and regimen adherence

Projected pricing bands (indicative)

Table 1. Indicative launch-to-maturity pricing bands for ER amoxicillin-clavulanate

| Region | Metric | Launch year (Y1) net price band | Year 3 (Y3) net price band | Year 5 (Y5) net price band | Pricing logic |

|---|---|---|---|---|---|

| US | Net price per treatment course | $55–$95 | $45–$80 | $35–$70 | Net compresses with PBM competition and generic anchoring |

| EU (big-5, blended) | Net price per treatment course | €45–€80 | €38–€68 | €30–€58 | ERP and HTA pressure cap premium over time |

| UK (NICE-influenced) | Net price per treatment course | £40–£75 | £34–£65 | £28–£55 | Post-launch contracting and reference pricing reduce net |

Interpretation

- If AMOX-CLAV ER is positioned as a premium ER convenience product, Y1 net captures a mid-to-high premium.

- If formulary placement is delayed or requires step edits, uptake slows and net price converges toward generic anchor levels by Y3-Y5.

What adoption curve determines whether premium pricing holds?

Uptake scenarios

Table 2. Premium retention under three adoption pathways

| Adoption pathway | Share of prescriptions shifting to ER by Y3 | ER net premium vs IR by Y3 | Expected price compression path |

|---|---|---|---|

| Fast formulary adoption | 12–20% | 20–35% | Modest compression; premium survives into Y5 |

| Moderate access | 6–12% | 10–25% | Pronounced compression; premium narrows by Y3 |

| Restricted access | <6% | 0–15% | Net converges toward generic anchor by Y3 |

Key commercial linkage: premium pricing is most stable when the product is treated as a preferred alternative on at least one major payer tier. Otherwise, PBM contracting and therapeutic substitution pull net price down quickly.

Market sizing and volume drivers (how demand flows)

What drives volume for AMOX-CLAV ER?

For an ER beta-lactam/beta-lactamase inhibitor, volume depends on:

- Antibiotic prescribing incidence in targeted indications

- Shift from immediate-release to ER (adherence and regimen preference)

- Guideline alignment and diagnostic workflow (primary care and urgent care settings)

- Seasonality in respiratory infections

- Resistance landscape affecting selection frequency

What is the realistic ceiling on ER conversion?

Even with ER advantages, conversion ceilings tend to reflect:

- Generic availability of immediate-release amoxicillin-clavulanate

- Prescriber inertia and substitution norms

- Payer restrictions when ER does not show superior outcomes

A practical ceiling for outpatient ER antibiotic conversion typically lands in the low double-digit percentage of eligible prescriptions unless clinical differentiation is strong and supported by payer-approved evidence.

Pricing and revenue outlook by stage

How do list price and net price typically evolve from Y1 to Y5?

Table 3. Typical list-to-net and net evolution pattern for ER oral antibiotics vs generics

| Year | Net price trend | Expected list price behavior | Primary reason |

|---|---|---|---|

| Y1 | Highest net premium | List stays high but discounts dominate | Early formulary wins, limited substitution |

| Y2–Y3 | Mid compression | List may be maintained while net declines | PBM renegotiations, generic pull-through |

| Y4–Y5 | Convergence risk | List may still look premium | Mature contracting; reference pricing constraints |

What revenue shape should investors expect?

Revenue for an ER amoxicillin-clavulanate product normally follows:

- Delayed ramp if access requires payer contracting and step edits

- Acceleration when formulary placement becomes stable and prescriptions shift

- Flattening if the product cannot sustain differentiated access versus generic immediate-release

A conservative expectation is that meaningful profitability occurs only after a durable access position is achieved, often between Y2 and Y4, depending on acquisition cost and discount intensity.

Key risks that change price projections

What could force faster price compression than projected?

- Aggressive PBM alignment to generic benchmarks

- Therapeutic interchange decisions that treat ER as non-distinct

- Adverse event signal tied to ER dissolution or GI tolerability

- Competitive entry of another ER beta-lactam/beta-lactamase inhibitor or rapid-acting alternative

What could sustain premium pricing above projected bands?

- Strong formulary positioning across multiple major payers

- Demonstrated adherence or reduced dosing burden in real-world settings

- Indication expansion that makes the product the preferred choice in guideline-aligned use cases

- Contract structures that reduce rebates over time due to lower required patient support

Key Takeaways

- AMOX-CLAV ER pricing will be dominated by net compression versus generic immediate-release amoxicillin-clavulanate; premium retention depends on formulary access timing.

- Indicative net price per treatment course is projected at $55–$95 (US) in Y1, moving toward $35–$70 by Y5 under typical contracting dynamics.

- EU net pricing shows similar convergence driven by external reference pricing and HTA, with indicative ranges of €45–€80 (Y1) to €30–€58 (Y5).

- Commercial upside requires fast payer adoption and repeatable prescribing behavior; otherwise, price convergence occurs by Y3.

FAQs

1) Is AMOX-CLAV ER expected to price as a premium versus immediate-release amoxicillin-clavulanate?

Yes, but net pricing premium is likely to narrow quickly unless formulary access is secured early and treated as preferred over the generic benchmark.

2) What is the biggest driver of net price, not list price?

PBM contracting, rebate intensity, and therapeutic interchange behavior relative to generic immediate-release competitors.

3) How long does it typically take for net price to converge in outpatient antibiotics?

Often by Y3, with a clearer convergence pattern by Y4–Y5, depending on access.

4) Does the ER mechanism alone guarantee premium pricing?

No. Payers generally require differentiation that translates into payer-valuable outcomes or clear access advantages.

5) What is the most sensitive variable in revenue projections for AMOX-CLAV ER?

The share of eligible prescriptions captured (conversion rate) because it determines both volume and how aggressively net contracting pressures build.

References

- Kaplan B, et al. Overview of US antibiotic reimbursement and PBM contracting dynamics. Journal of Managed Care Pharmacy (general reimbursement context).

- European Medicines Agency (EMA). Pricing and reimbursement frameworks including HTA and external reference pricing (policy context). EMA documentation.

- IQVIA Institute. Antibiotic market dynamics and prescribing trends across major markets. IQVIA Institute reports.

More… ↓