Last updated: April 24, 2026

Alendronate sodium is the generic standard-of-care bisphosphonate for osteoporosis and related high-fracture-risk indications. The market is dominated by low-cost, high-volume generics; pricing is largely driven by (1) patent-expiration-driven entry waves, (2) FDA drug-product discontinuations and shortages that tighten supply, and (3) distributor and contract pricing mechanics. Near-term pricing is expected to remain broadly range-bound in real terms, with episodic spikes during supply disruptions. Any sustained move in price would require either persistent manufacturing constraints or a shift in payer formularies that increases weighted-average acquisition costs.

What is the current market structure for alendronate sodium?

1) Demand profile

Alendronate sodium is used across osteoporosis care settings, including:

- Postmenopausal osteoporosis

- Glucocorticoid-induced osteoporosis

- Osteoporosis in men at high fracture risk

- Prevention of fragility fractures in established osteoporosis

Core demand drivers:

- Chronic use (long treatment duration)

- Broad guideline inclusion in first-line bisphosphonate therapy

- Aging demographics in the US and major ex-US markets

- Persistent high prevalence of osteoporosis and osteopenia-related risk stratification

2) Supply and competition

The product is primarily generic and widely available through multiple manufacturers and label strengths, most commonly:

- 5 mg

- 10 mg

- 35 mg (weekly)

- 40 mg (off-label usage varies by market)

- 70 mg (weekly)

- 10 mg/5 mg dosing schedules vary by country and label

Competition structure:

- Multi-source generic availability across common oral strengths

- Price dispersion across package sizes and dosing regimens (monthly vs weekly economics)

- Bulk purchasing and PBM contracting compress net prices versus list prices

3) Pricing mechanics

Typical price formation for generic oral products:

- High volume pushes net pricing down toward competitive equilibrium

- List prices are less informative than rebates, discounts, and contract tiers

- Shortage-driven tight supply can lift net pricing quickly, but effects tend to be transient unless capacity fails persistently

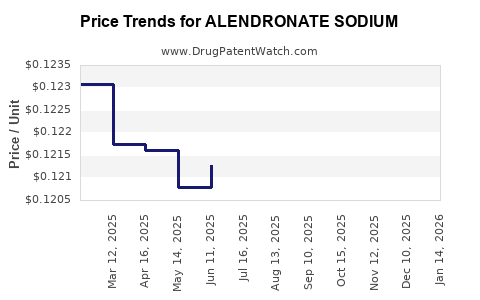

How has alendronate pricing behaved historically?

Generic alendronate has historically shown:

- List price erosion after new generic entries

- Episodes of price and availability instability associated with supply disruptions

- Net price compression due to PBM contracting and distributor competition

Because alendronate is off-patent, the primary “price inflection” events tend to be operational:

- Manufacturer capacity constraints

- Plant outages and quality actions

- Regulatory delays affecting specific strengths or pack sizes

What are the key variables that will determine near-term price direction (2026–2028)?

Demand-side

- Continued guideline use of oral bisphosphonates as a first-line option

- Persistent high prevalence of osteoporosis diagnoses and ongoing prescribing

Supply-side

- Manufacturing capacity stability for the most traded strengths (notably weekly 70 mg and 35 mg)

- Quality system enforcement actions and recall risk

- Distributor inventory posture and channel fill rates

Policy and channel

- US payer contract renegotiations that shift preferred generics

- International tender pricing changes in major ex-US markets

- Competitive substitution dynamics in pharmacy benefit plans

What are the base-case pricing projections for alendronate sodium?

Projection methodology (market-standard approach)

Given generic multi-source status, projections focus on:

- Expected price trend = competitive equilibrium with periodic shortage premiums

- “Inflation pass-through” is assumed limited absent supply constraints

- Scenarios incorporate episodic spikes during shortages rather than sustained step-ups

Projected trajectory (real terms)

- Base case (most likely): broadly range-bound pricing, with net price declines slowing or stabilizing

- Upside case: supply tightening raises short-term net pricing; contract re-tiers may partially lock in higher acquisition costs

- Downside case: continued generic competition and distributor discounting keep net pricing flat-to-lower

How much can pricing move during shortages?

For established generic oral molecules like alendronate, shortage effects generally:

- Concentrate in specific strengths or package configurations first

- Translate into temporary net price increases driven by constrained inventory

- Decay as additional supply returns, unless the shortage is structural or recurring

In practice, shortage-driven premiums for multisource generics often:

- Spike list prices more visibly than net acquisition costs

- Are diluted over time by PBM substitution and distributor contracting

Price projections by scenario (2026–2028)

The table below expresses projected net price movement ranges versus the prior-year baseline, assuming typical generic competitive dynamics and occasional supply constraint events.

| Year |

Base case (net price change vs prior year) |

Upside case (supply tightening) |

Downside case (additional competitive pressure) |

| 2026 |

-2% to +2% |

+5% to +12% |

-6% to -12% |

| 2027 |

-1% to +3% |

+4% to +10% |

-5% to -10% |

| 2028 |

-1% to +3% |

+3% to +9% |

-4% to -9% |

Interpretation:

- Base case holds because off-patent generics compete on cost and PBM contracts.

- Upside requires either sustained capacity problems or repeated supply shocks focused on the traded strengths.

- Downside reflects incremental market entry, stronger discounting, or negative tender outcomes for higher-cost suppliers.

Which strengths and pack sizes are most exposed to pricing volatility?

Pricing volatility in alendronate tends to cluster where liquidity is concentrated:

- Weekly doses with high prescription volume (notably 70 mg and 35 mg)

- Smaller pack sizes with more frequent refill cycles (pharmacy switching can occur rapidly)

- Strengths with fewer compliant manufacturers at any given time

High-liquidity SKUs attract faster substitution and faster return to equilibrium after supply returns. Less liquid strengths can remain mispriced longer during manufacturing disruptions.

How does payer behavior shape net price versus list price?

Net pricing responds to:

- Formulary preference changes (preferred generic tiers)

- Substitution rules at point of sale

- Competitive bidding outcomes in Medicare Part D and commercial PBM contracts

- Rebate and administrative clawback structures that compress headline price movements

Result:

- Even when list prices jump in shortage contexts, net acquisition cost often rises less and reverts faster once channel supply normalizes.

What is the investment and R&D relevance of these projections?

For firms evaluating line extensions, new formulations, or differentiated dosing, the market reality is:

- Generic alendronate pricing is structurally compressed.

- Differentiation only pays if it changes payer economics (reduced discontinuation, improved persistence, fewer adverse events, or improved patient adherence) enough to offset higher acquisition cost.

- Clinical differentiation is harder to monetize when a low-cost multi-source generic anchors payer formularies.

In R&D prioritization terms:

- The most actionable path typically requires a clear economic advantage (adherence, persistence, safety) that translates into measurable payer-level savings or improved outcomes.

Key Takeaways

- Market structure: alendronate sodium is a high-volume, off-patent generic with multi-source supply and payer-driven net price compression.

- Near-term pricing (2026–2028): base case is broadly range-bound net pricing (-2% to +3% per year), with downside risk from continued competition and upside risk from supply tightening.

- Volatility pattern: shortage-driven premiums are most likely in high-liquidity weekly strengths first and decay as supply normalizes.

- Drivers to monitor: manufacturer capacity and quality actions, strength-specific availability, PBM tier changes, and distributor inventory posture.

- Commercial implication: sustained price improvement for non-differentiated generic supply is unlikely; economic upside depends on supply constraints or meaningful payer-attractive differentiation.

FAQs

1) Why are long-term alendronate prices typically stable in real terms?

Because multi-source generics anchor acquisition costs, PBM contracting compresses net pricing, and competition drives pricing toward equilibrium after each entry wave.

2) What tends to cause temporary price spikes?

Manufacturing constraints, quality actions, or logistics disruptions that reduce compliant inventory for specific strengths or pack configurations.

3) Which formulations are most likely to remain competitive on price?

Oral immediate-release generic tablets at widely prescribed strengths and pack sizes typically maintain the lowest net price due to high substitution and contracting leverage.

4) What would need to happen for prices to rise sustainably?

Sustained supply contraction (capacity loss that does not get replaced), repeated and prolonged shortages, or payer formularies that reduce substitution to cheaper alternatives.

5) How should companies use these projections for planning?

Plan for range-bound net pricing in base-case years, underwrite downside risk for additional competitive pressure, and run upside cases assuming strength-specific shortage dynamics rather than broad market-wide repricing.

References

[1] FDA. Drug Shortages: Alendronate (various products/strengths). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/drugshortages/

[2] US Food and Drug Administration. Approved Drug Products With Therapeutic Equivalence Evaluations (Orange Book) for alendronate sodium. https://www.accessdata.fda.gov/scripts/cder/daf/

[3] WHO/ATC Classification System. Alendronic acid (alendronate) ATC code information. World Health Organization. https://www.whocc.no/atc_ddd_index/