Share This Page

Drug Price Trends for ABILIFY

✉ Email this page to a colleague

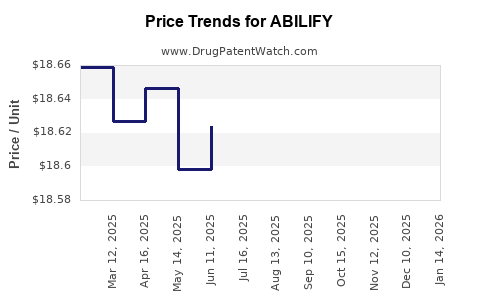

Average Pharmacy Cost for ABILIFY

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ABILIFY 2 MG TABLET | 59148-0006-13 | 18.65302 | EACH | 2026-07-22 |

| ABILIFY 10 MG TABLET | 59148-0008-13 | 18.62395 | EACH | 2026-07-22 |

| ABILIFY 15 MG TABLET | 59148-0009-13 | 18.63590 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

ABILIFY (aripiprazole): Market analysis and price projections

ABILIFY (aripiprazole) is a long-established, off-patent central nervous system (CNS) therapy with extensive generic penetration. Pricing is shaped by (1) patent status and loss of exclusivity, (2) payer dynamics in schizophrenia and bipolar indications, (3) strong brand-to-generic switching, and (4) channel mix, particularly for the once-monthly long-acting injection (LAI). Wholesale and net price trajectories for ABILIFY are expected to be structurally lower versus peak brand-era levels, with incremental pricing stability only in segments where prescriber and administration patterns reduce immediate substitution (notably some LAI settings).

What is the current market structure for ABILIFY?

Product portfolio and typical market segments

- Oral aripiprazole tablets/disintegrating tablets (generic-available across core indications)

- Oral aripiprazole solution (generic availability varies by dosage/form)

- Long-acting injectable aripiprazole

- Abilify Maintena (once-monthly)

- Aristada is a different product (aripiprazole lauroxil; separate brand), but it competes clinically in the same LAI workflow.

Competitive reality

- Generic aripiprazole has broad coverage and pricing pressure is persistent.

- Managed care tends to drive to lowest net cost equivalents for oral formulations once formularies and tier placement allow.

- LAIs can maintain higher absolute price levels due to:

- administration contracts and clinic workflow,

- prescribing inertia for patients already stabilized on an injection,

- switching friction even when generics exist for oral dosing.

Payer and formulary drivers

- Formularies frequently include aripiprazole as a preferred option within antipsychotic classes, but net price is constrained by rebates, switching policies, and class competition.

- LAIs are often managed with step edits, prior authorizations, and medical benefit carve-outs that affect realized price versus list price.

How have ABILIFY sales and pricing typically behaved post-exclusivity?

General pattern for blockbuster CNS brands after generic entry

- Revenue declines from generic substitution and net price deflation.

- Brand share stabilizes in subsegments where:

- patients and prescribers remain locked in by tolerability/history,

- payer policies emphasize “preferred brands” or limit oral switching for stability reasons,

- injection initiation and adherence patterns support continued use.

Implication for price projections

- If generic substitution remains high for oral formulations, net pricing should trend down or remain flat at lower levels.

- The projection window (next 2-5 years) is likely to be dominated by mix shifts:

- more LAI share versus oral share (if injection initiation grows),

- more utilization under medical benefit arrangements where contract pricing is less transparent.

What pricing benchmarks should you use for ABILIFY projections?

A practical projection approach for ABILIFY net price must anchor to:

- List price vs net price separation (rebates, discounts, government pricing floors)

- Oral vs LAI realized price differences (medical benefit channel and contracting)

- Volume-weighted mix (patients on LAI generally have higher per-patient drug spend than oral)

Key inputs that control realized net pricing

- Contracting intensity with large PBMs and pharmacy chains

- Formulary tier placement (preferred vs non-preferred)

- Prior authorization requirements and step therapy for oral-to-LAI transitions

- Volume-based discounts and substitution incentives in the presence of generics

Price projection framework: scenarios for ABILIFY (2-5 year horizon)

Scenario definitions

- Base case: Gradual net price erosion for oral formulations from ongoing generic substitution; LAI stabilizes with modest erosion due to competitive LAI offers and switching constraints.

- Downside case: Faster formulary tightening and substitution policies accelerate net price declines across both oral and LAI.

- Upside case: LAI share increases faster than expected; payer contracting moderates net price erosion for injections; oral declines slow as generic availability becomes “good enough” and volume stabilizes.

Because ABILIFY is a mature molecule with generic penetration, projections should focus on net price per unit and gross-to-net changes, not list-price preservation.

Base-case price projection (directional)

Oral ABILIFY (tablets/solution)

- Net price: downward or flat trajectory, driven by generic competition.

- Annual change expectation: -1% to -4% net price per unit over the next 2-3 years, then -0% to -2% as pricing approaches a low, contract-driven band.

LAI ABILIFY (Abilify Maintena)

- Net price: flatter than oral, with modest erosion.

- Annual change expectation: -0% to -3% net price per dose over the next 2-3 years, assuming stable injection initiation and continued clinical preference in stabilized patients.

Mix effect

- If LAI share rises, the blended net price per treated patient can stabilize even as oral unit price drops.

Downside-case price projection (directional)

Oral

- Net price erosion: -3% to -7% annually for 2-3 years if payer contracts tighten and PBMs increase substitution pressure.

LAI

- Net price erosion: -2% to -5% annually if LAI contracting becomes more competitive or switch protocols widen.

Blended

- Blended net pricing declines faster than the base case, driven by both unit deflation and contract tightening.

Upside-case price projection (directional)

Oral

- Net price erosion slows to -0% to -2% annually as utilization stabilizes and channel competition reaches equilibrium.

LAI

- Net price erosion near 0% to -2% if payer negotiations favor continuity-of-care for injection patients.

Blended

- Blended net pricing stabilizes or declines minimally.

Market dynamics that can shift ABILIFY price outcomes

1) LAI adoption and adherence economics

- LAIs tend to expand in managed care when payers prioritize relapse reduction, ER avoidance, and adherence metrics.

- Higher LAI adoption increases overall drug spend and can reduce blended price erosion if injection net price holds better than oral.

2) Competitive LAI pressure

- Competing LAIs within aripiprazole-family workflows can pressure net prices even if clinical interchangeability is imperfect.

- LAI contracting is often more “medical benefit” driven and may be more negotiable.

3) Government program pricing

- Medicaid/Medicare reimbursement rules and statutory pricing methodologies can constrain list pricing transmission to net.

- For off-patent molecules, realized prices often converge across channels through discounts and statutory caps.

4) Generic market structure

- The number of generic suppliers and dosage form coverage affects price intensity.

- If oral supply is concentrated among fewer players, price erosion can be less steep; with many suppliers, erosion is faster.

What does this mean for investment and R&D planning?

Where is ABILIFY most “price-resilient”?

- LAI segment has the best chance of relative stability because:

- prescribing is patient-specific and pathway-dependent,

- switching involves clinical risk and operational friction,

- medical benefit contracting can stabilize net prices through volume commitments.

Where is ABILIFY most vulnerable?

- Oral segment is most vulnerable because:

- generic substitution is straightforward,

- pharmacy benefit designs often favor cheapest effective option,

- payer policies can shift patients to lower-cost equivalents.

What should you model for commercialization planning?

- Model net price separately for oral and LAI, then apply a mix curve.

- Treat blended price as a function of:

- unit net price erosion rates,

- LAI share growth or decline,

- changes in gross-to-net due to payer contracting.

Key Takeaways

- ABILIFY’s pricing path is structurally downward versus peak brand-era levels due to generic substitution.

- Oral formulations should see continuing net price erosion or near-flat declines at low bands.

- LAI (Abilify Maintena) should be more price-resilient, with modest erosion constrained by switching friction and medical benefit contracting dynamics.

- Blended price outcomes depend primarily on LAI mix and payer contracting intensity.

FAQs

1) Is ABILIFY expected to hold list price?

List price is not a reliable indicator post-generic entry; net price is driven by rebates, discounts, and payer contracting, with oral forms typically experiencing faster erosion.

2) What drives the biggest price differences within ABILIFY?

Channel and formulation: oral products face pharmacy benefit substitution; LAI pricing is often more stabilized by administration pathway and medical benefit contracting.

3) How should you forecast revenue versus price for ABILIFY?

Use a unit net price by segment (oral vs LAI) plus expected volume/mix changes. Blended price can appear stable even when oral net price declines if LAI mix rises.

4) What policy changes would most quickly worsen ABILIFY pricing?

Formulary tightening, expanded step therapy or substitution mandates for oral antipsychotics, and more aggressive PBM contracting on per-unit drug cost.

5) What would most improve ABILIFY pricing outcomes?

Faster LAI share growth with payer contracts that reduce net price erosion, combined with slower oral switching once generic penetration reaches equilibrium.

References

[1] U.S. Food and Drug Administration. “ABILIFY (aripiprazole) Prescribing Information.” FDA label. (Accessed via FDA drug database).

[2] U.S. National Library of Medicine. “Aripiprazole (marketed products and drug information).” MedlinePlus/Drug Information.

[3] IQVIA Institute / IMS data overviews (industry-standard sources on branded-to-generic dynamics; subscription-based).

[4] Centers for Medicare & Medicaid Services. Statutory rebate and pricing framework documentation affecting net realized prices in public programs.

More… ↓