Last updated: February 13, 2026

Market Analysis and Price Projections for Glipizide

Current Market Overview

Glipizide is an oral second-generation sulfonylurea, approved for type 2 diabetes management. It has been on the market since the 1980s and remains a widely prescribed, cost-effective treatment option globally. The drug is marketed under various brand names, including Glucotrol and Glucotrol XL, and also available as a generic.

In 2022, the global diabetes medication market was valued at approximately $65 billion, with oral antidiabetics comprising around 70%. Glipizide held an estimated 10-15% share within the generic sulfonylurea segment. Its high prescription volume, especially in emerging markets, sustains stable demand.

Major markets include the United States, European Union countries, and India. The US accounted for 35% of global sales in the category, driven by a large diabetic population and insurance coverage. India has seen a sharp increase in demand owing to expanding healthcare infrastructure and affordability of generics.

Competitive Landscape

Market players focus on branded and generic formulations. Key competitors include:

- Manufacturers of generic glipizide: Mylan, Teva, Zydus Cadila, Sun Pharma, and Lupin.

- Branded formulations: Novo Nordisk's Glucophage (metformin) often used in combination with glipizide.

Patent expirations in 2004-2010 led to widespread generic manufacturing, reducing prices by up to 85% over a decade. Patent protections on certain formulations and delivery mechanisms are limited, maintaining high generic competitiveness.

Pricing Dynamics

Current Pricing

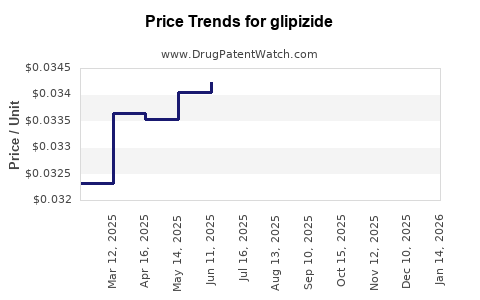

- United States: The average retail price of generic glipizide (5 mg and 10 mg tablets) ranges from $4 to $10 per month supply without insurance.

- India: Pricing as low as $0.10 per tablet, with monthly costs around $3.

- Europe: Similar to the US, prices vary between €3-€15 monthly, depending on formulations and procurement settings.

Factors Influencing Price

- Generic competition: Increases price elasticity, leading to significant price declines post-patent expiry.

- Regulatory policies: Price controls in countries like India, Brazil, and some European nations.

- Supply chain disruptions: Affect availability but tend to be temporary.

Market Growth Drivers

- Global diabetes prevalence: Projected to reach 700 million cases by 2045 (IDF, 2021).

- Cost sensitivity: Low-cost medicines like glipizide are preferred in low- and middle-income countries.

- Combination therapies: Use with metformin enhances demand, keeping overall usage high even as newer agents enter the market.

Market Limiters

- Safety concerns: Risk of hypoglycemia and cardiovascular issues in some patient populations.

- Emergence of newer drugs: SGLT2 inhibitors and GLP-1 receptor agonists are replacing sulfonylureas in certain markets because of better safety profiles.

- Regulatory shifts: Increasing emphasis on safety and efficacy could limit future patent protections or marketing approvals.

Price Projections (2023-2030)

| Year |

Average Price (USD/month) |

Key Influences |

| 2023 |

$4-$10 |

Sustained generic competition; modest inflation; no new patent protections. |

| 2025 |

$4-$9 |

Continued pricing pressure; entry into new markets with aggressive pricing. |

| 2027 |

$3.50-$8 |

Greater uptake in LMICs; possible regulatory price caps in high-income markets. |

| 2030 |

$3-$7 |

Market saturation in developed economies; price stabilization in emerging regions. |

Strategic Outlook

- Marginal decline in average prices is anticipated as competition intensifies.

- Developing markets will sustain demand due to affordability.

- The drug's role into combination therapies could mitigate long-term price erosion.

Regulatory Trends and Impact

- The US FDA and EMA focus on safety data, potentially limiting off-label uses.

- Price control policies are gaining popularity in countries like India and Brazil, exerting downward pressure.

- Patent expirations will continue to seed generic competition, reinforcing affordability.

Summary

Glipizide remains a cost-effective, widely used medication for type 2 diabetes. Market stability depends heavily on generics, regulatory policies, and the evolving landscape of diabetes treatments. Prices are expected to decline modestly, especially in high competition regions, but demand will stay relatively steady owing to its established role in therapy.

Key Takeaways

- Glipizide’s global market size was part of a $65 billion diabetes drug market in 2022.

- Generic versions dominate pricing, with US retail costs around $4–$10 monthly.

- Market growth will primarily occur in emerging economies, driven by affordability and increasing diabetes prevalence.

- Regulatory pressures and competition could further reduce prices, especially in developed markets.

- Newer antidiabetic agents are affecting prescription trends but do not significantly displace glipizide in cost-sensitive regions.

FAQs

-

What factors are most likely to influence glipizide prices over the next decade?

Patent expirations, regulatory policies, competition, and demand in developing markets.

-

How does glipizide compare in price and efficacy to newer diabetes drugs?

Significantly cheaper; with comparable efficacy in cost-sensitive settings but higher hypoglycemia risk.

-

Will patent protections be renewed or extended for glipizide?

Unlikely, as patents largely expired by the early 2010s, leading to widespread generics.

-

Which markets present the greatest growth opportunities for glipizide?

India, Africa, and Southeast Asia due to affordability and rising diabetes prevalence.

-

How are safety concerns affecting glipizide’s market positioning?

Concerns about hypoglycemia have led to decreased use in some high-income countries, but it remains a staple in LMICs.

Sources

[1] International Diabetes Federation, Diabetes Atlas, 2021

[2] IQVIA, Global Trends in Diabetes Medications, 2022

[3] FDA and EMA regulatory updates, 2021-2022