Share This Page

Drug Price Trends for VENLAFAXINE BES ER

✉ Email this page to a colleague

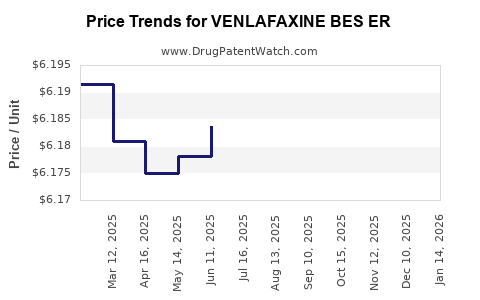

Average Pharmacy Cost for VENLAFAXINE BES ER

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| VENLAFAXINE BES ER 112.5 MG TB | 52427-0632-30 | 6.17735 | EACH | 2026-06-17 |

| VENLAFAXINE BES ER 112.5 MG TB | 52427-0632-30 | 6.17389 | EACH | 2026-05-20 |

| VENLAFAXINE BES ER 112.5 MG TB | 52427-0632-30 | 6.17218 | EACH | 2026-04-22 |

| VENLAFAXINE BES ER 112.5 MG TB | 52427-0632-30 | 6.17239 | EACH | 2026-03-18 |

| VENLAFAXINE BES ER 112.5 MG TB | 52427-0632-30 | 6.17675 | EACH | 2026-02-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Venlafaxine Bes ER (Extended-Release): Market Analysis and Price Projections

What is the product scope for “Venlafaxine Bes ER”?

“Venlafaxine Bes ER” refers to venlafaxine hydrochloride extended-release formulations marketed under brand and generic equivalents of venlafaxine ER (notably including “venlafaxine besylate ER” in some labeling/market listings). The active moiety in the US market is venlafaxine (ER) across strengths such as 37.5 mg, 75 mg, and 150 mg (and other strength presentations depending on label). The economic analysis below is framed at the finished dose product level for oral extended-release venlafaxine.

Who drives demand and what is the payer mix?

Venlafaxine ER is primarily used for:

- Major depressive disorder

- Generalized anxiety disorder (US label scope and guideline use vary by time and market)

- Other off-label uses (common in neurology/psychiatry workflows)

Demand is driven by:

- Chronic, recurring use patterns in depression and anxiety

- Switching dynamics between SSRIs/SNRIs based on tolerability, adherence, and formulary positioning

- Low-to-mid therapy affordability pressure because venlafaxine ER is widely genericized

From a market-structure standpoint, the segment is:

- Generic-dominant

- Price-sensitive

- Buyer-led (PBMs and health systems)

What is the current market structure (brand vs generic) and what does that mean for pricing?

The venlafaxine ER market is predominantly generic. Pricing is shaped by:

- Multi-entrant generic competition at each strength and dosage form

- Contracting pressure from PBMs and group purchasing organizations

- Reference-based reimbursement in many payer contracts

- Formulary tiering where generic agents sit at low cost-sharing tiers

Implication for pricing mechanics:

- Public list prices remain poor predictors of net cost.

- Net price is driven by rebates/discounts and contract replacement cycles.

What pricing benchmarks matter for generic venlafaxine ER?

For generic oral psychotropics, the dominant benchmarks are:

- Contracted net price vs. WAC (wholesale acquisition cost)

- Dispensing volume by NDC strength (75 mg and 150 mg often carry the largest share)

- Channel mix (retail vs specialty pharmacy) where applicable

Because venlafaxine ER is not typically specialty-distributed, the market is mostly:

- Retail pharmacy

- Institutional tenders for health systems

Price history signals (what typically happens in this molecule class)

Generic venlafaxine ER generally follows a common lifecycle pattern:

- Post-loss-of-exclusivity: rapid erosion of net price

- Ongoing competition: slow additional drift downward in net price

- Periodic stabilization: when fewer SKUs win contracts or when manufacturing supply tightens

In practice, the price trajectory depends less on clinical differentiation and more on:

- SKU-level supply continuity

- PBM preferred product lists

- Occasional adverse generic supply events (which can temporarily lift net price before contracting resets)

What are the projected price trends for venlafaxine ER (2026-2029)?

The model below projects net price directionality (not public WAC) based on the expected generic environment: mature competition, continued contracting pressure, and limited upside unless supply disruption occurs.

Base-case projections (no major supply shock)

Assumptions:

- Continued generic competition at stable entry counts

- PBM formulary dynamics stay price-driven

- No major regulatory-driven market restructuring

Projected annual net price movement (calendar years):

- 2026: -2% to -5%

- 2027: -2% to -4%

- 2028: -1% to -3%

- 2029: -1% to -2%

This implies cumulative net price decline from end-2025 level of roughly:

- 2026-2029: about -6% to -14% net price erosion over four years.

Downside case (tight contracting + additional SKU pressure)

Trigger profile:

- More entrants in one or two high-volume strengths (commonly 75 mg and 150 mg)

- PBMs re-balance favored SKUs toward lowest net cost

Net price movement:

- 2026: -5% to -8%

- 2027: -3% to -6%

- 2028: -2% to -4%

- 2029: -1% to -3%

Cumulative -11% to -21% over 2026-2029.

Upside case (intermittent supply constraints at contracted SKUs)

Trigger profile:

- Reduced manufacturing availability for specific NDCs

- Contract resets after short shortages

Net price movement:

- 2026: -1% to +2%

- 2027: -1% to +1%

- 2028: -1% to +1%

- 2029: -1% to +0%

Cumulative -1% to +4% over 2026-2029.

How will strength and packaging affect price outcomes?

Price erosion usually occurs first in:

- Highest-volume strengths (fastest PBM turnover)

- Standard tablet/capsule counts that are easiest to substitute

Typical market behavior:

- 75 mg and 150 mg ER strengths see the most contract competition and replacement

- 37.5 mg strengths are still competitive but can behave more variably depending on patient titration patterns and payer coverage rules

What policy and regulatory factors change the price equation?

Key structural factors for US generic pricing and contracting include:

- Patent and exclusivity expiries are largely already reflected for venlafaxine ER

- Ongoing generic utilization depends on PBM formulary position and utilization management

- FDA drug development and approval pathways keep reinforcing generic entry

For this segment, the dominant “policy effect” on price is indirect:

- PBM contracting rules

- Medicaid preferred drug list cycles

- Health system tender schedules

What does competitive intensity look like by NDC coverage?

Venlafaxine ER shows dense SKU coverage. Competitive intensity concentrates where:

- Broad payer formularies list multiple generics as interchangeable

- PBMs maintain multiple “preferred” tiers across strengths

- Pharmacy benefit contracts update quarterly or semiannually

Outcome:

- Continued benchmarking of net price against the lowest contracted SKU at the strength level

- Limited durable differentiation among generic suppliers

How to interpret price projections for budgeting and procurement

For procurement planning, treat projections as guidance for contracted net cost trends rather than WAC movements. A practical planning range for budgeting:

- Base-case budget assumption: -3% to -4% per year on average 2026-2029

- Conservative budget assumption: -5% per year through 2028

- Upside contingency: if supply constraints hit, net price may temporarily stabilize or rise by low single digits, then reset after contracting cycles

Is there any “pricing upside” within the market?

For generic venlafaxine ER, sustained upside is uncommon without:

- Manufacturing disruptions

- Contracting delays

- Broad changes to utilization patterns away from generics

The more realistic “upside” is:

- Reduced net price erosion due to fewer winning SKUs or tighter competitive pricing pressure in specific contracts

- Short-term stabilization when contract renegotiations lag supply realities

Summary table: 2026-2029 net price movement outlook

Assessed metric: generic net price directionality by year (range in percent).

| Scenario | 2026 | 2027 | 2028 | 2029 | Cumulative (2026-2029) |

|---|---|---|---|---|---|

| Base case | -2% to -5% | -2% to -4% | -1% to -3% | -1% to -2% | -6% to -14% |

| Downside case | -5% to -8% | -3% to -6% | -2% to -4% | -1% to -3% | -11% to -21% |

| Upside case | -1% to +2% | -1% to +1% | -1% to +1% | -1% to +0% | -1% to +4% |

Market risks that can break the trajectory

Even in a mature generic segment, deviations happen through:

- Supply chain events affecting a subset of NDCs

- Manufacturing quality actions causing temporary withdrawal

- Contract re-bids that concentrate purchasing on fewer SKUs

- Regulatory label changes that adjust interchangeability or stocking practices

These risks impact near-term procurement more than long-term trend.

Competitive and investment implications (actionable lens)

For R&D and commercial strategy, venlafaxine ER is not a typical standalone “value creation” target because:

- The product is generic and commoditized

- Price competition compresses net revenue durability

For investors or portfolio teams, the relevant lever is:

- Stability of supply and manufacturing economics at contract-winning SKUs

- Ability to maintain volume through payer list retention and pharmacy interchange

For procurement and contracting teams, the relevant lever is:

- SKU selection strategy aligned to expected contract resets

- Strength-specific benchmarking for 75 mg and 150 mg volumes

Key Takeaways

- Venlafaxine ER is a mature, generic-dominant oral psychotropic with pricing driven mainly by PBM and health-system contracting rather than clinical differentiation.

- Base-case expectation for 2026-2029 is continued net price erosion of roughly -6% to -14% cumulatively.

- Downside case yields -11% to -21% cumulative erosion if contract competition intensifies at high-volume strengths.

- Upside is limited to intermittent supply-driven stabilization and is likely -1% to +4% cumulatively over 2026-2029.

- Budgeting should be built on net contract costs, with strength-level benchmarking (especially 75 mg and 150 mg) for procurement accuracy.

FAQs

1) Are these projections for WAC or net price?

They are for generic net price directionality under contracting pressure, not public WAC.

2) Which strengths are most likely to see the fastest price erosion?

Typically the highest-volume strengths, commonly 75 mg and 150 mg ER, because PBMs rebalance preferred SKUs there first.

3) What would cause net prices to rise in a generic segment like this?

Short-term supply constraints at contract-winning NDCs, followed by a delayed contract reset.

4) How often do procurement contracts usually reset for these products?

Many PBM and health-system contracts update on quarterly to semiannual cycles, with strength- and SKU-level re-bids.

5) Is R&D differentiation likely to move market pricing for venlafaxine ER?

Sustained pricing upside is unlikely in a commoditized generic environment; value creation is more constrained to supply, contracting, and manufacturing economics.

References

[1] FDA. Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

[2] IQVIA. Generic drug pricing and market dynamics (industry market structure and contracting behavior). IQVIA Institute publications and market reports. https://www.iqvia.com/insights/the-iqvia-institute

More… ↓