Last updated: February 12, 2026

What is Veltassa?

Veltassa (patiromer) is an oral, potassium-binding polymer used to treat hyperkalemia, a condition characterized by elevated serum potassium levels. Approved by the U.S. Food and Drug Administration (FDA) in 2015, Veltassa primarily targets patients with chronic kidney disease (CKD) on dialysis or those with other comorbidities prone to hyperkalemia.

Market Size and Key Indications

Hyperkalemia prevalence varies globally, with estimates suggesting nearly 4-6% of the population affected in developed nations. In CKD populations, hyperkalemia incidence can exceed 50%, especially in advanced disease stages or among patients on medications like ACE inhibitors.

Estimated Global Hyperkalemia Prevalence

| Region |

Prevalence in CKD Patients |

Total CKD Population |

Estimated Hyperkalemia Cases |

| North America |

50-60% |

37 million |

18.5-22.2 million |

| Europe |

45-55% |

55 million |

24.7-30.3 million |

| Asia-Pacific |

30-40% |

200 million |

60-80 million |

Source: KDIGO guidelines (2017), Global Kidney Health Atlas (2020)

Competitive Landscape

Veltassa competes with other therapies, primarily sodium polystyrene sulfonate (SPS), patiromer’s direct competitor, and emerging agents such as ZS-9 (sodium zirconium cyclosilicate). Key players:

- Veltassa (patiromer): Developed by Relypsa (acquired by Novo Nordisk in 2018)

- ZyphrZAIR (sodium zirconium cyclosilicate): Marketed by AstraZeneca / Vifor

- SPS: Widely used, generic, but with safety concerns

Market Trends and Growth Drivers

-

Increasing CKD and ESRD Population: Rising CKD burden expands hyperkalemia cases, boosting Veltassa demand.

-

Shift from Emergency to Chronic Treatment: Patients increasingly receive long-term management, favoring Veltassa’s oral administration.

-

Guideline Endorsements: KDIGO and other societies recognize patiromer as a first-line agent for hyperkalemia management in patients receiving RAAS inhibitors.

-

Cost and Safety Profile: Veltassa’s lower gastrointestinal side effects compared to SPS drive adoption, especially in outpatient settings.

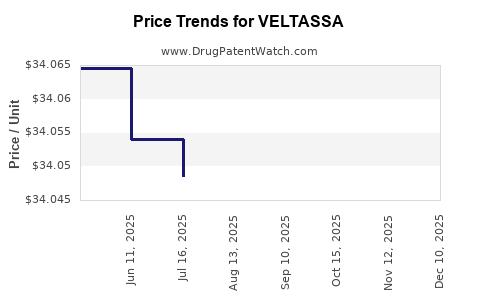

Price Dynamics and Reimbursement

Current Pricing

- U.S. average wholesale price (AWP): Approximately $28 per 8.4 g tablet.

- Monthly therapy cost: Typically 4-8 tablets daily, translating into $300-$600/month.

Reimbursement Landscape

- Insurance coverage and Medicare Part D largely support Veltassa use, but out-of-pocket expenses remain notable.

- Cost-effectiveness studies (e.g., from the Institute for Clinical and Economic Review) support its value in reducing hyperkalemia-related hospitalizations.

Price Projections (2023-2028)

Assumptions:

- Moderate annual price inflation (~3%).

- Increasing adoption due to expanded label use and clinical guidelines.

- Competition leads to pricing pressure from generics and alternative therapies by 2026.

| Year |

Price per Tablet |

Monthly Cost Estimate |

Notes |

| 2023 |

$28 |

$350 |

Stable with current market conditions |

| 2024 |

$29 |

$370 |

Slight increase, driven by inflation |

| 2025 |

$30 |

$390 |

Competition begins to impact pricing |

| 2026 |

$28 |

$350 |

Entry of generics may trigger price reductions |

| 2027 |

$27 |

$340 |

Further price compression expected |

| 2028 |

$26 |

$330 |

Market stabilization, possible decline |

Factors Influencing Future Pricing

- Patent exclusivity expiration: Patents for patiromer expected to expire around 2028, increasing generic competition.

- Regulatory updates: New indications or formulations could impact pricing.

- Market penetration: As Veltassa gains broader use, economies of scale may enable price reductions.

Revenue Projections

Given current sales levels (~$500 million globally in 2022) and market growth assumptions, revenues could grow 5-8% annually until patent expiration, followed by stagnation or decline.

| Year |

Estimated Global Revenue |

Factors Influencing Revenue |

| 2023 |

$530 million |

Continued uptake in CKD and ESRD populations |

| 2025 |

$620 million |

Broadened prescribing guidelines |

| 2026 |

$580 million |

Price competition begins |

| 2028 |

$550 million |

Patent expiry impacts sales |

Risks and Uncertainties

- Pricing pressure from generics.

- Regulatory or safety concerns affecting prescribing patterns.

- New therapies entering the hyperkalemia space potentially displacing Veltassa.

- Market saturation in core populations.

Key Takeaways

- Veltassa’s primary market encompasses CKD and ESRD populations at risk for hyperkalemia.

- Market size is driven by increasing CKD prevalence and rising hyperkalemia cases.

- Current pricing remains stable, with modest inflation; market entry of generics post-2028 expected to lower prices.

- Revenue growth is forecasted at 5-8% annually until patent expiration, after which it may decline due to competition.

- Clinical guidelines and safety profile support ongoing utilization, but economic pressures may temper future growth.

FAQs

Q1: How does Veltassa compare economically with SPS?

A: Veltassa's higher acquisition cost is offset by a better safety profile. SPS is cheaper but has safety issues, leading clinicians to favor Veltassa despite higher costs.

Q2: When are patents for Veltassa expected to expire?

A: Patents are expected to expire around 2028, after which generics are likely to enter the market.

Q3: What factors could accelerate Veltassa's market penetration?

A: Inclusion in clinical guidelines, wider insurance reimbursement, and positive real-world effectiveness data.

Q4: How will competition from ZS-9 impact Veltassa?

A: Both drugs target similar patient populations; market share may shift based on safety, efficacy, and pricing strategies.

Q5: What are the key uncertainties affecting price projections?

A: Patent expiry timing, regulatory changes, new drug approvals, and evolving clinical guidelines.