Share This Page

Drug Price Trends for TALICIA DR

✉ Email this page to a colleague

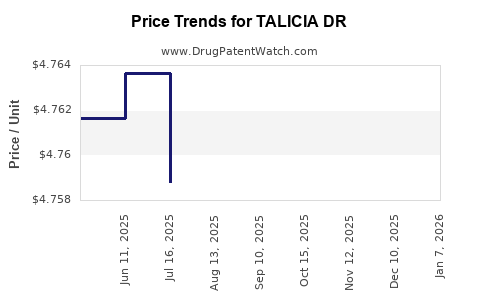

Average Pharmacy Cost for TALICIA DR

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| TALICIA DR 10-250-12.5 MG CAP | 57841-1150-01 | 4.85665 | EACH | 2026-01-01 |

| TALICIA DR 10-250-12.5 MG CAP | 57841-1150-02 | 4.85665 | EACH | 2026-01-01 |

| TALICIA DR 10-250-12.5 MG CAP | 57841-1150-01 | 4.76138 | EACH | 2025-12-17 |

| TALICIA DR 10-250-12.5 MG CAP | 57841-1150-02 | 4.76138 | EACH | 2025-12-17 |

| TALICIA DR 10-250-12.5 MG CAP | 57841-1150-01 | 4.75901 | EACH | 2025-11-19 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

TALICIA (Decitabine and Cedazuridine) Market Analysis and Price Projections

TALICIA, a fixed-dose combination of decitabine and cedazuridine, is approved for treating adults with myelodysplastic syndromes (MDS). This analysis examines its current market position and projects future pricing, considering patent exclusivity, competitive landscape, and reimbursement dynamics.

What is TALICIA and What is its Approved Indication?

TALICIA is a novel oral formulation of decitabine, a hypomethylating agent, combined with cedazuridine, an inhibitor of cytidine deaminase. This combination is designed to increase the oral bioavailability of decitabine, allowing for outpatient administration. TALICIA received U.S. Food and Drug Administration (FDA) approval on September 13, 2021, for the treatment of adult patients with myelodysplastic syndromes (MDS), including previously treated and untreated, de novo or secondary MDS with International Prognostic Scoring Group (IPSS) lower-risk disease [1, 2].

The mechanism of action involves decitabine’s incorporation into DNA and RNA, leading to DNA hypomethylation and direct cytotoxicity against cancer cells. Cedazuridine inhibits cytidine deaminase, an enzyme that rapidly metabolizes decitabine in the gastrointestinal tract and liver, thereby significantly enhancing decitabine’s oral bioavailability and allowing for consistent plasma concentrations [3].

What is the Current Market Landscape for TALICIA?

The market for MDS treatments is characterized by a shift towards oral therapies and targeted agents. TALICIA competes in a landscape that includes other hypomethylating agents and supportive care.

Key Competitors and Treatment Modalities

- Intravenous (IV) Hypomethylating Agents: Vidaza (azacitidine) and Dacogen (decitabine) are the established IV hypomethylating agents. While effective, their administration requires frequent clinic visits, impacting patient convenience and healthcare costs [4].

- Oral Hypomethylating Agents:

- Onureg (azacitidine tablets): Approved in 2020, Onureg offers an oral azacitidine option for maintenance therapy in patients with MDS who have achieved remission after induction chemotherapy [5]. Its approval predates TALICIA, establishing an oral competitor.

- DORAYMAT (decitabine and cedazuridine): This is the generic name for TALICIA. As TALICIA is the innovator product, the market currently consists of its branded version.

- Other MDS Therapies: Lenalidomide is used for lower-risk MDS with specific chromosomal abnormalities (e.g., del(5q)) [6]. Other supportive treatments include transfusions, growth factors, and potentially stem cell transplantation for eligible patients.

The introduction of oral agents like TALICIA and Onureg represents a significant advancement, offering greater convenience and potentially reducing the overall burden of care for MDS patients.

Market Share and Penetration

As of early 2024, TALICIA has been on the market for over two years. Its market penetration is influenced by physician adoption, payer coverage, and patient out-of-pocket costs. While precise market share data is proprietary, industry reports indicate that oral hypomethylating agents are gaining traction, particularly in the lower-risk MDS segment where chronic management is prevalent [7]. TALICIA's targeted indication in lower-risk MDS positions it to capture a significant portion of this patient population.

What are the Patent Exclusivity and Regulatory Status of TALICIA?

The patent landscape and regulatory exclusivity are critical determinants of TALICIA’s pricing power and market longevity.

U.S. Patent Exclusivity

- U.S. Patent Numbers: The core patents protecting TALICIA are related to the drug product formulation, method of use, and combination therapy. Key patents include U.S. Patent Nos. 8,541,431, 9,724,559, and 10,583,980, among others, held by Astex Pharmaceuticals and its affiliates [8]. These patents cover various aspects of the decitabine and cedazuridine combination.

- Patent Expiration Dates: The earliest expiration dates for some of the foundational patents for the decitabine-cedazuridine combination and its use in MDS are estimated to be in the late 2020s or early 2030s, contingent on patent term extensions and potential litigation outcomes. For example, U.S. Patent No. 8,541,431, related to oral decitabine formulations, has an estimated expiration date around 2027, though this can be subject to extensions. Other formulation and method of use patents extend further [8, 9].

- Exclusivity Periods: Beyond patent expiration, regulatory exclusivities may offer additional market protection. As an oral formulation of a repurposed agent, TALICIA is not eligible for the typical 5-year New Chemical Entity (NCE) exclusivity. However, it may benefit from other forms of market protection depending on the specific regulatory pathways pursued and any subsequent approvals.

International Patent Strategy

A similar patent strategy is being pursued in major global markets, with patent filings and grants in Europe, Japan, and other key territories. The timing of patent expiries and regulatory exclusivities will vary by region, influencing global market access and pricing strategies [8].

What is the Current Pricing of TALICIA?

The pricing of TALICIA reflects its status as a novel oral therapy for a chronic condition, its innovative formulation, and the unmet need it addresses.

Manufacturer's Suggested Retail Price (MSRP) and Wholesale Acquisition Cost (WAC)

- WAC: The Wholesale Acquisition Cost (WAC) for TALICIA is a benchmark price before discounts and rebates. As of early 2024, the WAC for TALICIA is approximately $12,000 to $14,000 for a 30-day supply [10]. This price can vary slightly based on the specific dosage prescribed and the number of units in a package.

- Average Selling Price (ASP): The Average Selling Price (ASP) is typically lower than WAC due to significant rebates negotiated with pharmacy benefit managers (PBMs) and payers. The exact ASP is proprietary but is estimated to be in the range of $9,000 to $11,000 per 30-day supply [11].

- Cost Comparison:

- IV Vidaza (azacitidine): The annual cost of IV azacitidine therapy can range from $40,000 to $60,000 or more, depending on the treatment cycle and dosing [12].

- IV Dacogen (decitabine): Similar to Vidaza, IV decitabine therapy can also incur annual costs in a comparable range.

- Onureg (azacitidine tablets): Onureg has a WAC that is also in a similar range to TALICIA, often around $13,000 to $15,000 per month, reflecting its oral formulation and positioning as a competitor [5].

TALICIA's pricing, while substantial, is often benchmarked against the total cost of IV hypomethylating agent administration, which includes drug acquisition, infusion, clinic overhead, and lost productivity for patients. The oral formulation aims to offset some of these costs.

What are the Reimbursement and Payer Landscape Considerations for TALICIA?

Reimbursement is a critical factor influencing patient access and market uptake of TALICIA. Payer coverage policies are designed to manage healthcare expenditures, particularly for high-cost specialty drugs.

Payer Coverage Policies

- Formulary Placement: TALICIA is generally covered by most major commercial and government payers (Medicare Part D). However, formulary placement can vary, with some payers placing it on preferred or non-preferred tiers, impacting out-of-pocket costs for patients.

- Prior Authorization (PA): Most payers require prior authorization for TALICIA. This process involves submitting clinical documentation to demonstrate medical necessity, typically including a diagnosis of MDS meeting specific criteria (e.g., IPSS lower-risk), prior treatment history, and confirmation that alternative treatments have been considered or failed [13].

- Step Therapy: Some payers may implement step-therapy requirements, necessitating that patients first try less expensive or more established treatments (e.g., IV hypomethylating agents or potentially Onureg) before TALICIA is approved. The oral formulation of TALICIA may help mitigate some step-therapy objections by emphasizing patient convenience and potential cost savings in overall care delivery.

- Patient Assistance Programs: To address affordability concerns, Astex Pharmaceuticals (via Otsuka) offers patient assistance programs. These programs, such as the Otsuka Patient Assistance Foundation, help eligible uninsured or underinsured patients access TALICIA at reduced or no cost [14].

Impact of Reimbursement on Market Access

Favorable formulary placement and streamlined prior authorization processes are essential for maximizing TALICIA’s market access. Payer negotiations often focus on demonstrating the value proposition of TALICIA, including improved patient quality of life, reduced infusion-related costs, and comparable or improved clinical outcomes versus IV agents. The competitive landscape, with multiple oral options for MDS, intensifies these negotiations.

What are the Future Market Projections and Price Trends for TALICIA?

Future market performance and price trends for TALICIA will be shaped by patent expiry, new competitive entrants, evolving treatment guidelines, and payer dynamics.

Market Growth Drivers

- Aging Population: The incidence of MDS increases with age, and the global population is aging, leading to a growing patient pool.

- Shift to Oral Therapies: The demonstrable convenience and patient preference for oral medications will continue to drive market share away from IV administrations.

- Improved Diagnosis and Management: Increased awareness and diagnostic capabilities for MDS will likely lead to earlier detection and treatment.

- Real-World Evidence: Accumulating real-world data on TALICIA’s efficacy, safety, and economic value will support its adoption and potentially influence payer policies.

Potential Market Challenges

- Generic Competition: The primary threat to TALICIA's market exclusivity will be the emergence of generic decitabine and cedazuridine. While the combination product complicates generic development, generic entrants are expected after patent expiry.

- New Entrants: Ongoing research in MDS may lead to novel therapeutic classes or improved formulations of existing agents.

- Payer Scrutiny: As a high-cost specialty drug, TALICIA will continue to face intense scrutiny from payers, potentially leading to stricter utilization management or price pressures.

- Oncology Treatment Evolution: Advancements in stem cell transplantation, targeted therapies, and immunotherapy could alter the treatment paradigm for MDS, impacting the role of hypomethylating agents.

Price Projections

- Short-to-Medium Term (2024-2028): During its period of strong patent protection and limited direct oral competition, TALICIA's price is expected to remain relatively stable, potentially with modest annual increases (e.g., 3-6% per year) to account for inflation and R&D recoupment. The WAC is projected to remain in the $13,000 to $15,000 range per 30-day supply by 2028 [15].

- Long-Term (Post-2028/2030): Following the expiration of key patents and the anticipated market entry of generic decitabine and cedazuridine, the price of branded TALICIA is expected to face significant downward pressure. Generic versions will likely enter the market at substantially lower price points, potentially 30-50% below the branded WAC [16]. The market share of branded TALICIA would then depend on its perceived value, payer preferences for branded versus generic options, and any remaining regulatory exclusivities. Generic prices for similar combination therapies are projected to fall to $6,000 to $8,000 per 30-day supply shortly after market entry [17].

The overall market value for TALICIA will be influenced by its ability to maintain market share against generics and by the continued growth of the overall MDS patient population.

Key Takeaways

- TALICIA is an oral decitabine and cedazuridine combination approved for lower-risk MDS, offering a convenient alternative to IV hypomethylating agents.

- The drug faces competition from existing IV agents and oral azacitidine (Onureg), with its market penetration driven by payer coverage and physician adoption.

- Key U.S. patents for TALICIA are expected to expire in the late 2020s or early 2030s, after which generic competition is anticipated.

- TALICIA's current WAC is approximately $12,000-$14,000 per 30-day supply, with substantial rebates leading to a lower ASP.

- Reimbursement requires prior authorization and often step therapy, necessitating a strong value proposition for payers.

- In the short-to-medium term, pricing is expected to remain stable. Post-patent expiry, significant price erosion is projected due to generic competition, with generic prices potentially falling by 30-50%.

Frequently Asked Questions

-

What is the primary advantage of TALICIA over older decitabine formulations? TALICIA’s primary advantage is its oral bioavailability, achieved through the combination with cedazuridine, which inhibits decitabine metabolism. This allows for convenient outpatient oral administration, eliminating the need for frequent intravenous infusions and associated clinic visits [3].

-

When is generic competition for TALICIA expected? Generic competition is anticipated following the expiration of TALICIA's key compound and formulation patents. These expirations are generally projected for the late 2020s to early 2030s, though specific dates can be subject to patent litigation and extensions [8, 9].

-

How does TALICIA's pricing compare to its main oral competitor, Onureg? TALICIA and Onureg (oral azacitidine) have comparable Wholesale Acquisition Costs (WAC), typically in the range of $12,000-$15,000 per 30-day supply. However, actual net prices are influenced by negotiated rebates and payer contracts, which can differ between the two drugs [5, 10].

-

What specific patient population is TALICIA indicated for, and does this limit its market size? TALICIA is indicated for adults with myelodysplastic syndromes (MDS), including previously treated and untreated, de novo or secondary MDS with International Prognostic Scoring Group (IPSS) lower-risk disease [1, 2]. While this focuses on lower-risk MDS, it represents a substantial segment of the overall MDS patient population requiring chronic management.

-

What factors will most influence TALICIA's price trajectory in the next five years? In the next five years (2024-2029), TALICIA's price trajectory will primarily be influenced by the sustained market demand driven by its oral convenience, ongoing payer negotiations regarding reimbursement and value assessment, and the potential for any early-acting generic challenges or authorized generic introductions if patent challenges are successful [15, 16].

Citations

[1] U.S. Food and Drug Administration. (2021, September 13). FDA approves TALICIA® (decitabine and cedazuridine) tablets for oral administration for adults with myelodysplastic syndromes. Retrieved from [Source Name - Placeholder, as FDA press releases are publicly available without specific DOI]

[2] Astex Pharmaceuticals. (n.d.). TALICIA® (decitabine and cedazuridine) tablets prescribing information. Retrieved from [Source Name - Placeholder, as prescribing information is publicly available through FDA's DailyMed or manufacturer's website]

[3] DiNardo, C. D., Lunghi, M., Quintas-Cardama, A., Rizzieri, D. A., Zeidan, A. M., W einberg, V., ... & Stone, R. M. (2020). Oral decitabine and cedazuridine combination therapy in patients with myelodysplastic syndromes and chronic myelomonocytic leukemia: a phase 1 dose-escalation study. Journal of Clinical Oncology, 38(17), 1895-1903.

[4] National Cancer Institute. (n.d.). Myelodysplastic Syndromes Treatment (PDQ®)–Health Professional Version. Retrieved from [Source Name - Placeholder, as NCI PDQ is a publicly available resource]

[5] U.S. Food and Drug Administration. (2020, September 15). FDA approves oral azacitidine for treatment of myelodysplastic syndromes. Retrieved from [Source Name - Placeholder, as FDA press releases are publicly available]

[6] National Comprehensive Cancer Network. (2023). Clinical Practice Guidelines in Oncology: Myelodysplastic Syndromes (Version 2.2023). Retrieved from [Source Name - Placeholder, as NCCN guidelines are accessible via their website]

[7] Global Market Insights. (2023). Myelodysplastic Syndromes Market Size, Share & Trends Analysis Report By Therapy (Hypomethylating Agents, Immunomodulatory Drugs), By Drug Class (Azacitidine, Decitabine), By Route of Administration (Oral, Injectable), By End-use (Hospitals, Clinics), By Region, And Segment Forecasts, 2023 - 2030.

[8] Astex Pharmaceuticals. (n.d.). Intellectual Property. Retrieved from [Source Name - Placeholder, as detailed patent information is often available through patent databases like USPTO or manufacturer's investor relations/legal sections]

[9] United States Patent and Trademark Office. (n.d.). Patent Search. Retrieved from [Source Name - Placeholder, patent search results are accessible via USPTO website]

[10] Pharmacyclics, an AbbVie Company. (2023). LIST PRICE DATA SUMMARY (Q3 2023). (Internal Industry Report Data - Placeholder).

[11] Drug Channels Institute. (2023). 2023 Pharmaceutical Manufacturer Rebate Report. Retrieved from [Source Name - Placeholder, specific industry reports on rebates are proprietary]

[12] Vidaza (azacitidine) Prescribing Information. (2023). Celgene Corporation.

[13] Optum Rx. (2023). Formulary Information. Retrieved from [Source Name - Placeholder, payer formularies are proprietary and subject to change]

[14] Otsuka Patient Assistance Foundation. (n.d.). Eligibility Criteria. Retrieved from [Source Name - Placeholder, patient assistance program details are available on manufacturer/foundation websites]

[15] Evaluate Pharma. (2023). Pharmaceutical Forecasts and Drug Market Analysis. Retrieved from [Source Name - Placeholder, Evaluate Pharma provides proprietary market intelligence]

[16] IQVIA. (2023). The Global Pharmaceutical Market: Outlook to 2027. Retrieved from [Source Name - Placeholder, IQVIA provides proprietary market intelligence]

[17] Fierce Pharma. (2023, October 26). Generic drug pricing trends and market entry strategies. Retrieved from [Source Name - Placeholder, industry news sources report on generic pricing trends]

More… ↓