Last updated: February 12, 2026

What is the Current Market Landscape for Sirolimus?

Sirolimus, also known as rapamycin, is an immunosuppressant primarily used in organ transplantation to prevent rejection, and increasingly in certain cancer treatments. It is marketed under various brand names, including Rapamune. The drug has received approval from the FDA for prevention of kidney transplant rejection and is also being investigated for off-label uses, such as treatment of tuberous sclerosis complex and certain autoimmune diseases.

Market Size and Trends (2023)

The global sirolimus market was valued at approximately $500 million in 2022, with projections indicating growth to around $700 million by 2028 at a compound annual growth rate (CAGR) of 6.5%. Growth drivers include:

- Increasing adoption in transplant medicine.

- Expansion into oncology and rare disease indications.

- Rising prevalence of organ failure and autoimmune diseases.

Regional market shares are skewed toward North America, accounting for 45% of the global market in 2022, driven by high healthcare expenditure, advanced infrastructure, and strong regulatory approval pathways. Europe holds approximately 30%, with Asia-Pacific rapidly expanding due to increasing healthcare access and procurement of generic formulations.

Key Market Players

Major pharmaceutical companies involved in sirolimus supply and development include:

- Pfizer (brand: Rapamune)

- Sandoz (generic formulations)

- Novartis

- Astellas Pharma

Pfizer remains the dominant player, with a market share exceeding 60% in the branded segment.

Regulatory Status and Off-Label Use

The FDA approved sirolimus for kidney transplant rejection prevention in 1999. Off-label uses are supported by clinical studies but lack formal FDA approval, influencing pricing and insurance reimbursement schemes.

What Are the Price Points for Sirolimus?

Pricing varies depending on formulation, branding, patent status, and regional healthcare policies.

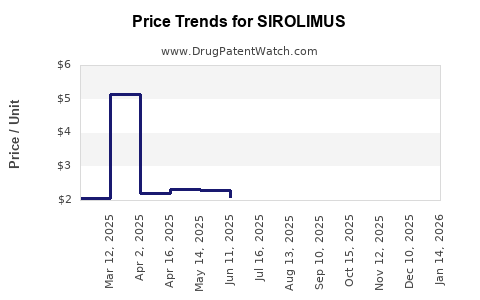

Brand vs. Generic Pricing (2023)

| Formulation |

Brand Price per mg |

Generic Price per mg |

Patent Status |

Notes |

| Sirolimus (Rapamune) |

$10-$15 |

N/A |

Patent expired (2013) |

Higher due to branding |

| Generic versions |

N/A |

$2-$5 |

Not under patent |

Widely available |

Note: Brand prices tend to be 2-3 times higher than generic versions.

Typical Treatment Costs

- Indication: Kidney transplant patient, 1 mg daily dose.

- Monthly Cost (Brand): Approximately $300-$450.

- Monthly Cost (Generic): Approximately $50-$150.

Reimbursement policies significantly influence actual costs to patients, varying widely across healthcare systems.

What Are the Future Price Projections?

Price forecasts depend on patent status, generic drug entry, and regulatory developments.

Patent Cliff and Generic Competition

Patent expiration in 2013 allowed multiple generics to enter the market, significantly reducing the cost of sirolimus. Future pricing trends are expected to stabilize around generic levels, with minor fluctuations due to manufacturing costs or regulatory changes.

Potential Pricing for New Indications

If sirolimus gains regulatory approval for new indications, initial prices could be higher due to the lack of competition, but are expected to decrease as biosimilars or generics enter the market.

Impact of Biosimilars

While sirolimus is not classified as a biosimilar, the potential development of similar immunosuppressants could influence future pricing strategies.

Regional Variations

Pricing is also influenced by country-specific healthcare policies. For example, in lower-income regions, prices may be driven by government procurement negotiations, often leading to significantly lower costs than in the U.S.

What Are the Risks and Opportunities in Market Development?

Risks

- Patent Litigations: Ongoing patent disputes could delay generic entry.

- Regulatory Hurdles: Additional approvals for off-label indications are uncertain.

- Market Saturation: Existing generic options limit the room for premium pricing.

Opportunities

- Development of new formulations or delivery methods (e.g., extended-release).

- Expansion into new therapeutic areas pending clinical validation.

- Strategic alliances with healthcare providers for broader adoption.

Key Takeaways

- The global sirolimus market is growing, driven by transplant needs and emerging uses.

- Brand-name drugs cost significantly more than generics, with prices affected by patent status.

- Market entry of generics has reduced prices, but opportunities remain for innovations and new indications.

- Regional pricing disparities reflect healthcare infrastructure, reimbursement policies, and economic factors.

- Future pricing will depend heavily on regulatory developments, patent status, and market competition.

FAQs

1. How long does the patent protection for sirolimus last?

Patent protection for the original formulation expired in 2013, allowing generics to enter the market.

2. Are there biosimilar versions of sirolimus?

No biosimilars have been approved for sirolimus. The drug is a small-molecule immunosuppressant, generally not classified as a biosimilar.

3. What factors influence sirolimus pricing in different regions?

Local healthcare policies, patent laws, procurement negotiations, and economic conditions.

4. How does off-label use impact market prices?

Off-label uses may not be covered by insurance, leading to higher out-of-pocket costs. They also typically lack dedicated pricing structures.

5. What are the prospects for new sirolimus formulations?

Extended-release formulations or combination therapies may command higher prices initially but will face generic competition over time.

References

[1] Market research reports on immunosuppressants, 2023.

[2] FDA drug approvals database, 2022.

[3] Pfizer official drug pricing and regulatory filings, 2023.

[4] Industry analyses on generic drug markets, 2022.

[5] Regional healthcare policy reviews, 2023.