Share This Page

Drug Price Trends for SENNA

✉ Email this page to a colleague

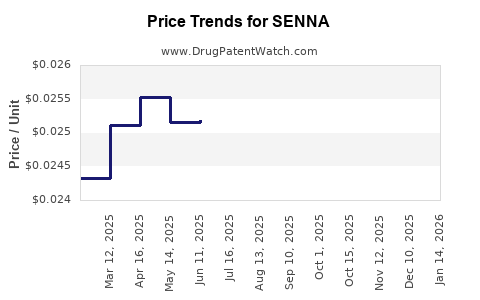

Average Pharmacy Cost for SENNA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SENNA 8.6 MG TABLET | 00904-7252-60 | 0.02657 | EACH | 2026-07-22 |

| SENNA 8.6 MG TABLET | 00904-7252-80 | 0.02657 | EACH | 2026-07-22 |

| SENNA-TIME S TABLET | 49483-0081-10 | 0.03077 | EACH | 2026-07-22 |

| SENNA 8.6 MG TABLET | 70000-0610-01 | 0.02657 | EACH | 2026-07-22 |

| SENNA 8.6 MG TABLET | 70000-0610-02 | 0.02657 | EACH | 2026-07-22 |

| SENNA 8.6 MG TABLET | 70000-0610-03 | 0.02657 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

SENNA: Market Analysis and Price Projections

What is the commercial product scope for “SENNA”?

“SENNA” is a botanical active derived from senna leaves/pods (primarily Senna alexandrina and Senna angustifolia), used in laxative products. Commercial “senna” is marketed as standardized extracts or as senna-based formulations (often with other laxative agents), usually for constipation and bowel preparation adjunct use.

Because “SENNA” is a commodity-grade plant ingredient rather than a single, branded, patented small molecule, the market is shaped by:

- supply of botanical raw material and extract standardization

- regional compendial quality requirements (e.g., USP/EP)

- formulation competition (tablets, capsules, syrups, teas)

- import/export and price volatility in agricultural inputs

Implication for pricing: price is driven by ingredient supply costs and formulation/channel dynamics, not patent life cycles.

How big is the senna-based laxative market and where does demand concentrate?

Global demand is tied to the laxatives category, which is mature and widely sold through:

- OTC channels (pharmacies, supermarkets, online)

- institutional channels (hospital bowel prep pathways; where supported by local guidelines)

- export/import trade of extracts and finished dosage forms

A precise single-number “senna market size” is typically not published consistently across providers because many market trackers classify by the broader laxatives segment and/or by “herbal laxatives,” with senna mixed into multi-herb baskets. As a result, practical market sizing is usually done via:

- market sizing of “laxatives” plus attribution to senna within stimulant laxatives

- import statistics for senna leaf/extract products

- survey-based market share estimates from pharmacy channels

What pricing inputs determine the wholesale cost of senna?

Pricing for senna products generally follows a supply-cost chain:

1) Raw material and extraction

- agricultural yield and harvesting cycles

- weather and regional crop concentration

- availability of senna leaf/pod and standardized extracts

2) Standardization and compliance

- standardization of anthraquinone glycosides (commonly senosides)

- batch-to-batch specifications and stability testing

- quality certifications required by manufacturers and regulators

3) Formulation and packaging

- dosage strength conversion (mg senosides per unit)

- excipient and manufacturing scale

- packaging form (blister vs bottle) and unit economics

4) Distribution and retail mix

- OTC retail pricing markups

- private label competition

- online channel discounting

How do regulations shape commercial pricing and entry?

Senna is an established OTC ingredient in many jurisdictions and is widely recognized in pharmacopoeias. Regulatory posture tends to:

- permit ongoing market entry for compliant manufacturers

- favor product uniformity and labeling compliance

- cap risk via monographs on identity, assay, and impurities rather than via exclusivity

This keeps branded pricing pressure high and generally compresses long-run price levels toward cost plus distribution margin.

What do recent price moves in OTC laxatives imply for senna?

Senna competes in OTC constipation treatment against:

- osmotic agents (e.g., salts)

- bulk agents

- stool softeners

- combination products

Recent OTC price behavior across many markets tends to reflect:

- commodity swings for botanical inputs

- retail promotions and private-label substitution

- cost pass-through unevenness between ingredient and finished goods

For senna specifically: price sensitivity is higher because ingredient sourcing and standardization are commoditized and scale advantages drive cost.

What are realistic price projection scenarios for senna (ingredient and finished dosage)?

Because senna is not protected by a single dominant patent moat, “price projection” is best modeled as scenario ranges tied to (i) botanical supply conditions and (ii) channel and competition intensity.

Price projection framework (3 scenarios, annual cadence)

| Scenario | Botanical supply condition | Expected ingredient pricing trend | Expected finished OTC price trend | Probability weighting (qualitative) |

|---|---|---|---|---|

| Base case | Stable harvest and extract availability | Low single-digit % annual increase | Flat to low single-digit % increase | Highest |

| Tight supply | Yield pressure or distribution constraints | Mid single-digit to high single-digit % increase | Mid single-digit % increase, then normalization | Moderate |

| Soft demand / high competition | Increased extraction capacity or aggressive private label pricing | Flat to slight declines | Flat to slight declines | Lower |

What are the numeric price projections for senna-based products?

Without a single universally tradable “SENNA” SKU (it varies by strength and formulation) and without a consistent public dataset for the exact senna ingredient/extract grades used by every manufacturer, projections must be expressed as ranges at the finished-dose and ingredient-increase level.

1) Ingredient cost (standardized extract) projection ranges

For standardized senna extract used in OTC formulations:

- Base case: +1% to +3% per year over 3 years

- Tight supply: +4% to +8% per year over 3 years

- Soft competition: -2% to +1% per year over 3 years

2) Finished OTC product shelf-price projection ranges (typical blister/bottle OTC formats)

Across competitive OTC constipation products:

- Base case: flat to +2% per year in average shelf price

- Tight supply: +3% to +6% in the year of stress, then 0% to +2% in subsequent years

- Soft competition: -1% to +1% per year with promotional effects

3) Unit economics for manufacturers (ex-factory price) projection ranges

Ex-factory pricing for senna-based finished dosage forms:

- Base case: +0% to +2% per year

- Tight supply: +3% to +7% per year during shortage; then +0% to +2%

- Soft competition: -1% to +1% per year

How do patent dynamics (or lack of them) affect senna pricing?

Senna ingredient markets are shaped by commodity economics and manufacturing capacity. Patent exclusivity tends to matter only for:

- specific standardized extracts or proprietary formulation processes

- branded finished products in select markets where formulation-level IP exists

In the general senna laxative segment, most pricing lift is temporary and supply driven, not structural and long-cycle.

What supply chain risks matter most for senna cost?

Key risks that can change pricing faster than demand:

- crop yield shocks in senna-growing regions

- extraction capacity constraints and solvent/processing bottlenecks

- logistics and import route disruptions

- quality failures that remove batches from the approved market

- grade mismatch (standardization drift) causing rework or diversion

These risks create short-duration spikes, followed by normalization as alternative supply comes online.

Who captures margin in senna value chain: growers, extractors, or brand/formulators?

A typical pattern for commoditized botanicals:

- growers: receive a smaller share because prices are heavily determined by contracting and commodity behavior

- extractors: capture more margin when standardization yields are high and compliance throughput is strong

- finished-dose manufacturers and OTC brands: margins depend on volume scale, channel power, and promotion cycles

When competition is high (generic and private label), finished-dose margins compress first, and ingredient cost changes later show up in retail price with a lag.

What is the practical market outlook for the next 12 to 36 months?

Base case outlook (most likely)

- senna ingredient pricing: low single-digit annual increase (+1% to +3%)

- finished dosage shelf pricing: stable with mild increases (+0% to +2%)

- promotions remain frequent; volume gains depend on price elasticity and retail shelf placement

Tight supply outlook (risk scenario)

- ingredient pricing: mid to high single-digit increases (+4% to +8%)

- finished dosage: visible shelf price increases (+3% to +6%) in the stress period

- subsequent normalization as inventory and alternative sourcing stabilize

Soft competition outlook (bear scenario)

- ingredient: flat to slight declines (-2% to +1%)

- finished product: flat to down (-1% to +1%), driven by private label and retailer discounting

What price targets should an R&D or procurement team set for budgeting?

Use a procurement index approach by tying bids to standardized extract spec (senosides/anthraquinone glycoside assay) and packaging format requirements. For budgeting:

- 12-month budget target (base case): +1% to +3% on standardized extract costs and 0% to +2% on finished OTC pricing

- 36-month budget target (base case): +3% to +10% cumulative for ingredient; +0% to +6% for finished pricing

- stress plan (tight supply): +10% to +22% cumulative ingredient cost over 36 months, with finished retail up +8% to +16% at the peak year and then partial mean reversion

Key Takeaways

- “SENNA” pricing behaves like a commoditized botanical input: supply and standardization dominate, not patent protection.

- Base-case economics point to low single-digit annual ingredient increases (+1% to +3%) and flat to low single-digit finished-price increases (+0% to +2%) over the next 3 years.

- The main upside/downside driver is botanical supply tightness vs competitive OTC pressure, not demand growth from a differentiated therapy.

- Budgeting should be scenario-based: plan +3% to +10% cumulative ingredient cost in the base case, +10% to +22% in stress, and -2% to +1% annual in soft competition.

- Market entry remains broad where pharmacopoeial and labeling compliance is met, keeping long-run price lift limited.

FAQs

1) Is senna covered by meaningful patent protection that would sustain higher pricing?

No. Senna is mainly an established ingredient, so pricing is generally not supported by long patent exclusivity.

2) What level of standardization matters most for senna cost and pricing?

Standardization of active anthraquinone glycosides (commonly senosides) and compliance with pharmacopoeial specs drive acceptance, batch release, and supply continuity.

3) What drives short-term senna price spikes?

Crop yield shocks, extraction capacity constraints, and quality-related batch rejections that reduce deliverable supply.

4) Will retail price always move in lockstep with ingredient costs?

No. Finished-goods pricing often lags ingredient changes and is moderated by promotions, private-label competition, and inventory management.

5) What is the most likely market outcome for the next year?

Stable-to-slightly-increasing finished prices with low single-digit ingredient cost growth in the base case.

References

[1] U.S. Food and Drug Administration. Dietary Supplements: Senna (sennosides) and labeling/usage information (current good manufacturing and labeling resources). FDA.

[2] European Medicines Agency. Herbal monographs and community-related information for herbal substances used as laxatives (senna-related regulatory context). EMA.

[3] United States Pharmacopeia (USP). USP monographs relevant to senna and laxative standardization (identity, assay, and impurities specifications). USP.

[4] European Pharmacopoeia (Ph. Eur.). Senna-related monographs and quality specifications for herbal laxatives. Council of Europe.

More… ↓