Share This Page

Drug Price Trends for RESTASIS

✉ Email this page to a colleague

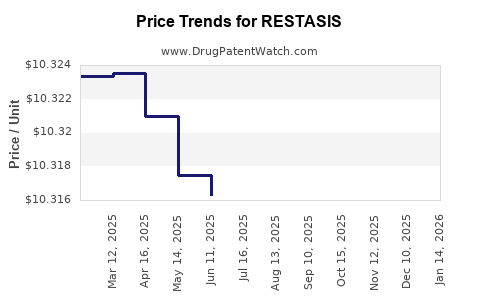

Average Pharmacy Cost for RESTASIS

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| RESTASIS 0.05% EYE EMULSION | 00023-9163-60 | 10.31793 | EACH | 2026-06-17 |

| RESTASIS MULTIDOSE 0.05% EYE | 00023-5301-05 | 112.32931 | ML | 2026-06-17 |

| RESTASIS 0.05% EYE EMULSION | 00023-9163-30 | 10.31586 | EACH | 2026-06-17 |

| RESTASIS MULTIDOSE 0.05% EYE | 00023-5301-05 | 112.33355 | ML | 2026-05-20 |

| RESTASIS 0.05% EYE EMULSION | 00023-9163-60 | 10.31843 | EACH | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

RESTASIS Market Analysis and Price Projections

RESTASIS (cyclosporine ophthalmic emulsion) 0.05% and 0.1% is a prescription eye drop used to treat the signs and symptoms of dry eye disease. The drug is manufactured by Allergan, now part of AbbVie. This analysis focuses on the market dynamics, competitive landscape, and projected pricing for RESTASIS, considering its patent status and the emergence of biosimil and generic competition.

What is the current market size and projected growth for RESTASIS?

The global dry eye disease market, encompassing treatments like RESTASIS, is substantial and expected to grow. Several factors drive this growth, including an aging population, increased screen time leading to digital eye strain, and a greater prevalence of autoimmune diseases that can cause dry eye.

The U.S. market for dry eye treatments is estimated to be in the billions of dollars annually. While specific revenue figures for RESTASIS are proprietary, its established presence as a first-line treatment for moderate to severe dry eye indicates a significant market share.

Projected growth for the overall dry eye market is robust, with compound annual growth rates (CAGRs) estimated between 5% and 10% over the next five to seven years. This growth is influenced by advancements in diagnostic tools, novel therapeutic approaches, and increasing patient awareness. RESTASIS, despite facing competition, is expected to maintain a relevant position due to its established efficacy and physician familiarity. However, the pace of its individual revenue growth may be tempered by generic and biosimilar entry.

What is the patent and exclusivity status of RESTASIS?

RESTASIS has a complex patent history, marked by numerous patent applications and subsequent litigation. The original patents for RESTASIS have largely expired, but Allergan (AbbVie) pursued a strategy of obtaining secondary patents and new formulations to extend market exclusivity.

Key patent expirations that have impacted RESTASIS include:

- Original Composition of Matter Patents: These have expired, allowing for generic development.

- Method of Use Patents: Allergan has litigated against generic companies based on patents covering specific methods of using cyclosporine for dry eye. However, many of these have been invalidated or are nearing expiration.

- Formulation Patents: New formulations, such as RESTASIS MULTIDOSE, were developed to secure additional exclusivity. The patent expiry for these formulations also influences the competitive landscape.

The legal battles surrounding RESTASIS patents are well-documented, with significant court decisions impacting the timeline for generic market entry. For example, the U.S. Patent Trial and Appeal Board (PTAB) has invalidated several key patents claimed by Allergan, paving the way for generics. [1, 2]

The U.S. Food and Drug Administration (FDA) has approved several generic versions of cyclosporine ophthalmic emulsion 0.05%. These approvals signal the end of effective market exclusivity for the original RESTASIS.

Who are the key competitors to RESTASIS?

The competitive landscape for RESTASIS includes both established prescription treatments and emerging generic and biosimilar alternatives.

Direct Competitors (Prescription Dry Eye Treatments):

- Xiidra (lifitegrast ophthalmic solution) 5%: Manufactured by Shire (now Takeda), Xiidra is a prescription eye drop that works by blocking the action of an important protein in the body that contributes to inflammation. It competes directly with RESTASIS for patients with moderate to severe dry eye. Xiidra has its own patent portfolio and market exclusivity.

- TrueTear: An external medical device that stimulates the natural tear film production, not a direct ophthalmic solution but addresses dry eye.

- Apremod-A (Loteprednol etabonate ophthalmic suspension) 0.25%: Approved for the chronic treatment of dry eye disease by reducing ocular inflammation.

Indirect Competitors (Over-the-Counter and Emerging Therapies):

- Artificial Tears: A broad category of lubricants (e.g., Systane, Refresh, TheraTears) that provide temporary relief.

- Oils and Emulsions: Some products aim to stabilize the lipid layer of the tear film.

- Omega-3 Fatty Acids: Oral supplements are sometimes recommended.

- Other Prescription Cyclosporine Formulations: As generic versions enter the market.

Emerging Competition: Generic RESTASIS

The most significant competitive threat to RESTASIS has been the introduction of generic versions of cyclosporine ophthalmic emulsion 0.05%. Several pharmaceutical companies have received FDA approval and launched their generic products, leading to a significant erosion of RESTASIS's market share and pricing power. Examples of generic manufacturers include:

- Teva Pharmaceuticals

- Allergan (AbbVie) itself has launched a generic version.

- Other manufacturers have also entered the market.

What are the current pricing and projected price trends for RESTASIS?

The pricing of RESTASIS has historically been a point of discussion due to its effectiveness in treating a chronic condition. As a branded specialty ophthalmic drug, its list price has been relatively high.

Current Pricing Landscape:

- List Price (Branded RESTASIS): Prior to widespread generic availability, the list price for a 5 mL bottle of RESTASIS 0.05% or 0.1% could range from $300 to $400. However, this list price is often significantly reduced through patient assistance programs, insurance formularies, and negotiated rebates.

- Generic Cyclosporine Ophthalmic Emulsion: The introduction of generics has dramatically altered the pricing landscape. Generic versions are typically priced at a fraction of the branded product's list price, often between $50 and $150 for a 5 mL bottle, depending on the manufacturer and pharmacy.

Projected Price Trends:

The price trend for branded RESTASIS is expected to continue its decline. As more generic manufacturers gain market share, the branded product will likely see further price erosion. AbbVie may retain some market share through its own generic offering or by targeting specific patient segments.

- Branded RESTASIS: Expect further price reductions and a decrease in overall sales revenue as generic penetration increases. The focus will shift from premium pricing to competing for a smaller niche market or through bundled offerings.

- Generic RESTASIS: Prices for generic cyclosporine will likely stabilize and then gradually decrease further as competition intensifies. Price wars among generic manufacturers are common, driving down costs for consumers and payers. The pricing will become more competitive, aligning with other generic ophthalmic solutions.

- Payers and PBMs: Pharmacy Benefit Managers (PBMs) and insurance companies will continue to prioritize lower-cost generic options. This will lead to restrictive formularies for the branded product and preferential coverage for generics, further pressuring RESTASIS pricing.

The total market revenue for cyclosporine ophthalmic emulsion, including both branded and generic, is likely to stabilize or grow modestly, driven by volume increases in the generic segment, even as the revenue from branded RESTASIS diminishes.

What are the regulatory and market access considerations impacting RESTASIS?

Regulatory approvals and market access are critical for any drug's commercial success. For RESTASIS, these considerations have evolved significantly.

Regulatory Landscape:

- FDA Approvals: The FDA's approval of multiple generic versions of cyclosporine ophthalmic emulsion 0.05% is the primary regulatory factor impacting RESTASIS. Each generic approval signifies a legal pathway for market entry, directly challenging the branded product's exclusivity.

- Patent Challenges: The success of legal challenges against RESTASIS patents by generic manufacturers has been pivotal. PTAB decisions and court rulings have consistently weakened Allergan's (AbbVie's) ability to maintain market exclusivity through patent enforcement.

- Bioequivalence: Generic drugs are required to demonstrate bioequivalence to the reference listed drug (RESTASIS). This ensures that the generic performs the same way in the body, allowing for its approval and acceptance by regulatory bodies and physicians.

Market Access:

- Payer Policies: Insurance companies and PBMs play a significant role in market access. They develop formularies that dictate which drugs are covered and at what tier. With the availability of generics, payers are increasingly restricting coverage for branded RESTASIS, pushing patients towards lower-cost generic alternatives.

- Physician Prescribing Habits: While physicians often have prescribing preferences, the availability of effective and affordable generics can influence their choices. Many physicians may switch to prescribing generic cyclosporine to reduce patient out-of-pocket costs.

- Patient Assistance Programs: Branded drug manufacturers often offer patient assistance programs to mitigate high out-of-pocket costs. However, the effectiveness of these programs diminishes when a significantly cheaper generic option is available.

- Interchangeability: For some biosimil drugs (though RESTASIS is a small molecule and thus subject to generic, not biosimilar, rules), the concept of interchangeability can further impact market access. A generic drug approved as interchangeable can be substituted by the pharmacist without requiring a new prescription. While not directly applicable to RESTASIS generics in the same way as biologics, it highlights the evolving landscape of drug substitution.

The overall trend is towards increased market access for generic cyclosporine and restricted access for branded RESTASIS, driven by cost-containment initiatives from payers and the availability of therapeutically equivalent alternatives.

What are the key takeaways for R&D and investment decisions?

The market for RESTASIS and its therapeutic category provides several key insights for R&D and investment.

- Patent Expiration is a Predictable Event: The lifecycle of a drug is heavily influenced by its patent protection. Companies must proactively plan for patent expiries and the inevitable entry of generic or biosimilar competitors.

- Secondary Patents and Formulation Strategies Have Limited Lifespan: While companies can extend exclusivity through new patents and formulations, these strategies face increasing scrutiny and legal challenges. The R&D investment in such extensions must be weighed against the likelihood of sustained market protection.

- Generic Entry Causes Significant Price Erosion: The introduction of generics is a primary driver of price decline for branded drugs. This erosion can be rapid and substantial, impacting revenue projections.

- Therapeutic Class Growth Can Offset Individual Drug Decline: Even as branded RESTASIS faces decline, the overall dry eye market is growing. This presents opportunities for new entrants or for companies with diversified portfolios within the therapeutic class.

- Payer Influence is Paramount: Market access is increasingly dictated by the preferences of payers (insurance companies, PBMs). Drugs that offer significant cost savings or demonstrable superior outcomes in terms of value are more likely to gain favorable formulary placement.

- R&D Focus on Novel Mechanisms and Improved Delivery: Future R&D in dry eye should focus on novel therapeutic mechanisms of action that offer distinct advantages over existing treatments, or on innovative delivery systems that improve efficacy, convenience, or patient adherence. Simply reformulating existing molecules may not provide sufficient market differentiation or extended exclusivity.

- Investment in Generic or Biosimilar Development is a Lower-Risk, Lower-Margin Strategy: For companies focused on generic or biosimilar development, the path to market involves navigating regulatory hurdles and competing on price. This offers a more predictable revenue stream but with lower profit margins compared to novel drug development.

- Market Intelligence on Patent Litigation is Crucial: For investors and R&D strategists, closely monitoring patent litigation and regulatory decisions related to key drugs is essential for accurate forecasting and risk assessment.

Frequently Asked Questions

-

Will AbbVie continue to support branded RESTASIS with significant marketing efforts? AbbVie's marketing efforts for branded RESTASIS are likely to decrease as generic competition intensifies. The company's strategy will likely shift towards promoting its own generic offering and focusing on other pipeline assets or established brands with stronger exclusivity.

-

What is the typical out-of-pocket cost for patients using generic cyclosporine ophthalmic emulsion? Out-of-pocket costs for generic cyclosporine ophthalmic emulsion typically range from $20 to $50 per prescription, depending on the patient's insurance plan, copayments, and the specific pharmacy pricing.

-

Are there any pending regulatory actions or patent challenges that could further impact RESTASIS's market position? Given the extensive patent litigation that has already occurred, significant new challenges are less likely. However, ongoing patent disputes or new regulatory reviews for specific formulations or indications could emerge. Investors should monitor updates from the USPTO and FDA for any developments.

-

How does RESTASIS compare in efficacy and side effects to its main competitor, Xiidra? Both RESTASIS and Xiidra are approved for the chronic treatment of dry eye disease. Clinical trials have shown both drugs to be effective in improving signs and symptoms of dry eye, though individual patient responses can vary. Common side effects for RESTASIS include eye pain and redness. Xiidra's common side effects include instillation site pain, altered taste, and blurred vision. Direct head-to-head comparisons in real-world settings continue to inform physician choices.

-

What are the future therapeutic avenues being explored for dry eye disease beyond cyclosporine and lifitegrast? Research into dry eye disease is exploring various novel mechanisms, including therapies targeting inflammation pathways, neurotrophic factors, and the ocular surface microbiome. New drug delivery systems, such as sustained-release implants and nanoparticles, are also under development to improve treatment efficacy and patient convenience.

Citations

[1] U.S. Patent and Trademark Office. (n.d.). Patent Trial and Appeal Board Decisions. Retrieved from [USPTO website] (Note: Specific decision links would require direct search and are dynamic).

[2] U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA website] (Note: Specific drug and approval dates require direct search).

More… ↓