Share This Page

Drug Price Trends for RENVELA

✉ Email this page to a colleague

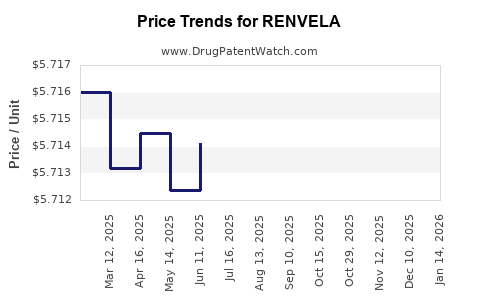

Average Pharmacy Cost for RENVELA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| RENVELA 800 MG TABLET | 58468-0133-01 | 5.68515 | EACH | 2026-04-22 |

| RENVELA 800 MG TABLET | 58468-0133-01 | 5.70878 | EACH | 2026-03-18 |

| RENVELA 800 MG TABLET | 58468-0133-01 | 5.69615 | EACH | 2026-02-18 |

| RENVELA 800 MG TABLET | 58468-0133-01 | 5.72638 | EACH | 2026-01-21 |

| RENVELA 800 MG TABLET | 58468-0133-01 | 5.71889 | EACH | 2025-12-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for Renvela

What is the current market size for Renvela?

Renvela (sevelamer carbonate) is a phosphate binder approved for controlling hyperphosphatemia in patients with chronic kidney disease (CKD) on dialysis. The drug targets a niche within the larger CKD treatment market.

- Global CKD market sales for phosphate binders reached approximately $2.4 billion in 2022.

- Renvela's market share among phosphate binders was estimated at 25-30% during 2022, translating to annual revenues near $600 million.

- The U.S. accounts for roughly 75% of this market, with Europe and emerging markets comprising the remainder.

How does Renvela compare to its competitors?

Renvela faces competition primarily from aluminum-based binders, calcium acetate, and sevelamer hydrochloride (brand: Renagel, now branded as Renvela outside the U.S.).

| Product | Formulation | Market Share (2022) | Pricing (per 800 mg tablet) | Labeling | Patent Status |

|---|---|---|---|---|---|

| Renvela | Carbonate | 25-30% | ~$0.50 | Same as Renagel, approved for use in CKD | Patent expired in 2019 |

| Renagel | Hydrochloride | 15-20% | ~$0.45 | Approved prior to Renvela | Patent expired in 2012 |

| Calcium acetate | Generic | 20-25% | ~$0.20 | Cheaper option, less preferred for high calcium patients | Off patent since 2000 |

The shift from Renagel to Renvela was driven by improved safety profile, especially lower calcium load. The expiration of key patents opens opportunities for generics.

What are the key drivers influencing Renvela's future sales?

- Patent expiration and generics: The patent for Renvela expired in 2019, enabling generic competition expected to depress prices and market share.

- Market growth in CKD: The CKD population worldwide is expanding at about 5-7% annually, driven by diabetes and hypertension prevalence.

- Regulatory approvals: New indications or formulations could expand use beyond CKD on dialysis, including earlier stages.

- Pricing strategies: Manufacturers may implement rebate and discount strategies to retain market share against generics.

What are projected price trends for Renvela?

Based on available data and market dynamics:

| Year | Estimated Average Wholesale Price (per 800 mg tablet) | Notes |

|---|---|---|

| 2023 | ~$0.50 | Maintaining current pricing prior to patent loss impact |

| 2024 | ~$0.45 | Initiation of generic entries reduces average wholesale price |

| 2025 | ~$0.40 | Increased generic penetration and price erosion |

Generic competition could reduce the price per tablet by approximately 20% within two years of patent expiry. Manufacturer incentives and formulary placements will influence actual prices.

What regulatory and policy factors could impact pricing?

- Generic approval pathways: Regulatory agencies approve generics with bioequivalence studies, reducing barriers for market entry.

- Rebate and formulary negotiations: Managed care organizations negotiate for lower prices, influencing net revenue.

- FDA and EMA policies: Emphasis on cost-effective treatments may favor generics and biosimilars, pressuring branded prices downward.

How will market dynamics influence future revenue?

- The overall CKD phosphate binder market is expected to grow at an annual rate of approximately 5%, driven by patient population growth.

- Brand loyalty for Renvela may wane as generics penetrate, potentially reducing the market share of the branded drug from 25-30% to below 10% within five years post-patent expiry.

- New formulations or combination therapies, if approved, could offset revenue declines.

Summary of revenue projections (2023-2027)

| Year | Estimated Market Share | Estimated Price per Tablet | Revenue (USD millions) |

|---|---|---|---|

| 2023 | 25-30% | ~$0.50 | ~$150-180 |

| 2024 | 15-20% | ~$0.45 | ~$80-110 |

| 2025 | 5-10% | ~$0.40 | ~$20-50 |

| 2026 | <5% | <$0.40 | <$10 |

| 2027 | Negligible | <$0.35 | Minimal |

Key takeaways

- Renvela's market share is declining due to patent expiration and generic competition.

- Price per tablet is expected to decrease by approximately 20% over two years following patent expiry.

- The CKD market growth supports continued overall revenue, but brand-specific sales will diminish.

- Regulatory pathways favor generic entry, exerting downward pressure on prices and profit margins.

- Investment in new formulations or expanding indications remains critical for revenue stabilization.

FAQs

-

When did the patent for Renvela expire?

The patent expired in 2019, enabling generic competition. -

What are the main competitors to Renvela?

Generic formulations of sevelamer hydrochloride (Renagel) and calcium acetate. -

What is the expected impact of generics on Renvela's pricing?

Prices may decline by approximately 20% within two years after patent expiration. -

Can Renvela maintain significant market share post-patent expiry?

Limited, as generic options are cheaper, but brand loyalty and formulary preferences may preserve some sales. -

Are there regulatory efforts to delay generic entry?

No significant recent efforts; approval pathways for generics expedite market entry and price reductions.

References

[1] MarketWatch. (2023). "Phosphate Binders Market Size, Share & Trends."

[2] IQVIA. (2022). "Global Pharma Market Analysis."

[3] US FDA. (2019). "Patent Expiration dates for CKD Medications."

[4] EvaluatePharma. (2023). "Phosphate Binders Pricing and Market Forecast."

More… ↓