Share This Page

Drug Price Trends for MIGRAINE

✉ Email this page to a colleague

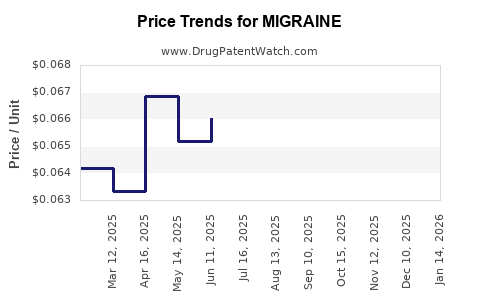

Average Pharmacy Cost for MIGRAINE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| MIGRAINE 250-250-65 MG GELTAB | 70000-0611-01 | 0.06716 | EACH | 2026-05-20 |

| MIGRAINE 250-250-65 MG CPLT | 24385-0365-71 | 0.06716 | EACH | 2026-05-20 |

| MIGRAINE FORMULA CAPLET | 24385-0365-78 | 0.06716 | EACH | 2026-05-20 |

| MIGRAINE 250-250-65 MG CPLT | 70000-0247-01 | 0.06716 | EACH | 2026-05-20 |

| MIGRAINE 250-250-65 MG CPLT | 70000-0247-02 | 0.06716 | EACH | 2026-05-20 |

| MIGRAINE 250-250-65 MG GELTAB | 70000-0611-01 | 0.06676 | EACH | 2026-04-22 |

| MIGRAINE 250-250-65 MG CPLT | 24385-0365-71 | 0.06676 | EACH | 2026-04-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

What Is the Current Market Size for Migraine Drugs?

The global migraine treatment market was valued at approximately $4.2 billion in 2022. It is projected to grow at a compound annual growth rate (CAGR) of 3.8% from 2023 to 2030, reaching around $6.1 billion. The market's growth is driven by increasing prevalence, rising awareness, and new drug approvals.

What Are the Leading Drugs and Their Market Shares?

The migraine drug market comprises triptans, CGRP (calcitonin gene-related peptide) inhibitors, and other class-specific medications.

| Drug Class | Key Drugs | Estimated Market Share (2022) | Growth Rate |

|---|---|---|---|

| Triptans | Sumatriptan, Rizatriptan | 45% | Slight decline due to newer therapies |

| CGRP Inhibitors | Aimovig (erenumab), Ajovy | 40% | Rapid growth (CAGR 9%) |

| Other Treatments | Ergots, NSAIDs, Botox | 15% | Declining as newer drugs dominate |

CGRP inhibitors have seen rapid uptake since their approval from 2018 onward, capturing a significant share from traditional triptans and older therapies.

What Are Key Drivers and Barriers in Market Growth?

Drivers:

- Increasing prevalence: Estimated that 1 billion people worldwide suffer from migraines, with higher incidence in women (up to 18%) than men.

- Rising awareness: Patients seek targeted therapies, boosting sales of innovative drugs.

- Regulatory approvals: Several new CGRP inhibitors received approval in the past five years.

Barriers:

- High drug costs: CGRP inhibitors can exceed $7,000 annually per patient, reducing affordability.

- Insurance coverage: Variability restricts patient access.

- Limited long-term safety data: Some clinicians prefer established therapies until more data are available.

What Is the Price Trajectory for Migraine Medications?

Traditional Drugs (Triptans, Ergots):

- Price per dose ranges from $10 to $25.

- Generic versions have reduced costs, increasing accessibility.

CGRP Inhibitors:

- Prices range from $6,000 to $7,500 annually.

- No substantial price reductions expected in short term due to brand exclusivity periods and manufacturing costs.

- Biosimilar development in pipeline could introduce lower-cost alternatives in 3-5 years.

Future Price Trends:

- Market penetration of biosimilars may pressure prices down 15-20% over the next five years.

- Insurance negotiations and pharmacy benefits manager (PBM) strategies could also lower out-of-pocket costs.

What Are the Commercial Expectations for New Entrants?

Pipeline drugs targeting migraines include oral CGRP receptor antagonists and combination therapies. Expected launch years range from 2024 to 2026.

| Drug Name | Developer | Expected Launch Year | Anticipated Impact |

|---|---|---|---|

| Atogepant (oral CGRP) | AbbVie | 2024 | Potential to substitute injectables |

| Eptinezumab (IV infusion) | Lundbeck | 2024 | Expanding patient eligibility |

| Novel small molecule therapy | Several biotech firms | 2025-2026 | Price competition, market expansion |

New entrants could capture 5-10% market share within 2 years of launch, especially if priced competitively and with additional convenience features.

How Do Regulatory and Policy Factors Influence Pricing?

FDA approvals and evolving reimbursement policies significantly influence market dynamics.

- Breakthrough Therapy Designation accelerates approval timelines.

- Insurance coverage mandates for CGRP inhibitors have increased access but remain variable across countries.

- Patent expirations for key drugs could usher in biosimilar competition, dampening prices.

What Are the Projections for Future Market Growth and Pricing?

| Year | Market Size (Estimate) | CAGR | Notes |

|---|---|---|---|

| 2023 | $4.2 billion | 3.8% | Steady growth driven by CGRP adoption |

| 2025 | $5.3 billion | 4.0% | Increased biosimilar competition, price pressure |

| 2030 | $6.1 billion | 3.8% | Market maturation, newer drugs expansion |

Prices for the overall market are expected to stabilize; however, specific segments—especially premium biologics—may see slight reductions due to biosimilar entry.

Key Takeaways

- The migraine drug market reached $4.2 billion in 2022, with a forecasted annual growth near 3.8%.

- CGRP inhibitors inherit the majority of sales, with rapid growth since approval.

- Drug prices remain high for biologics, with biosimilars on the horizon poised to influence downward pressure.

- New drugs and formulations could reshape market shares by 2025, broadly expanding access and competition.

- Regulatory, insurance, and patent policies will continue to shape pricing dynamics and market trajectory.

FAQs

1. How do CGRP inhibitors compare to traditional triptans in terms of pricing?

CGRP inhibitors cost roughly $6,000–$7,500 annually per patient, significantly higher than triptans, which are typically under $25 per dose due to generics.

2. What factors could accelerate market growth beyond current projections?

Faster adoption of new oral CGRP drugs, expanded insurance coverage, and more approvals of innovative therapies could increase growth rates.

3. When are biosimilars expected to impact migraine biologics’ pricing?

Biosimilars are projected to enter the market between 2024 and 2026, potentially reducing biologic prices by 15-20% over five years.

4. What regions present the most growth opportunities?

Emerging markets such as Asia-Pacific and Latin America show increasing migraine prevalence and evolving healthcare infrastructure.

5. How might policy changes affect migraine drug pricing?

Reimbursement reforms, patent expirations, and approval policies will influence both drug accessibility and pricing strategies.

Sources:

[1] MarketResearch.com, "Global Migraine Market," 2023.

[2] Grand View Research, "Migraine Drugs Market Size & Trends," 2022.

[3] FDA Drug Approvals, 2018–2023.

[4] IQVIA, "Pharmaceutical Pricing and Reimbursement," 2022.

[5] Pharma Intelligence, "Pipeline Updates for Migraine," 2023.

More… ↓