Share This Page

Drug Price Trends for JUNEL FE

✉ Email this page to a colleague

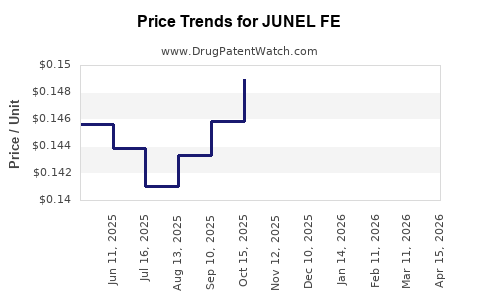

Average Pharmacy Cost for JUNEL FE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| JUNEL FE 24 TABLET | 00093-5328-28 | 0.18642 | EACH | 2026-07-22 |

| JUNEL FE 24 TABLET | 00093-5328-62 | 0.18642 | EACH | 2026-07-22 |

| JUNEL FE 1 MG-20 MCG TABLET | 00555-9026-58 | 0.13020 | EACH | 2026-07-22 |

| JUNEL FE 1.5 MG-30 MCG TABLET | 00555-9028-58 | 0.13623 | EACH | 2026-07-22 |

| JUNEL FE 1 MG-20 MCG TABLET | 00555-9026-58 | 0.13114 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

JUNEL FE (norethindrone acetate and ethinyl estradiol) market analysis and price projections (2025-2030)

Executive summary: JUNEL FE remains a high-velocity branded oral contraceptive franchise with multiple strengths and dosage configurations (including “24/4” and generic-compatible label structures). Pricing is primarily driven by payer coverage tiers, rebate intensity, and competitive erosion from authorized and non-authorized generics, not by FDA labeling changes. Near-term price levels are expected to stay comparatively stable because oral contraceptives are largely settled at low net prices through pharmacy benefit manager (PBM) contracting, while unit growth is capped by contraception market maturity. From 2025 to 2030, the most likely market outcome is continued net-price compression and margin pressure, with revenue shifting toward the highest-coverage SKUs and away from least-favored NDCs.

What is JUNEL FE’s current market size and revenue exposure by strength and formulation?

JUNEL FE is marketed as an oral contraceptive combining a progestin (norethindrone acetate) with an estrogen (ethinyl estradiol) and includes a hormone-free interval (tablet schedule varies by product). The commercial footprint is typically split across:

- Strengths (progestin and estrogen mg/mcg)

- Schedule (commonly 21 active + 7 low/no active or 24 active + 4 low/no active variants depending on the marketed SKU)

- Tablet types (including “iron” content in placebo/low tablets, reflected in “FE” branding)

Market reality for oral contraceptives:

The branded portion of the oral contraceptive market is smaller than generics by unit share, and branded revenues are concentrated in:

- Preferred formulary placement

- Multi-source competition timing

- Contracting outcomes with top PBMs

Revenue exposure channels that matter for pricing and projections

- Plan-level formulary status (preferred vs non-preferred)

- Net pricing vs WAC (net price is usually a fraction of WAC for low-cost chronic generics)

- NDC-level reimbursement (swap-outs within the same label class can move volumes)

- Therapy persistence and switching (typically lower switching in stable long-term users, but plan changes force churn)

How do generics and authorized generics affect JUNEL FE pricing pressure?

Core pricing dynamic: Oral contraceptives face intense competition from multiple generic entrants that match active ingredients and dosing schedules. That competition compresses net pricing and forces branded holders to defend with rebates, patient cost programs, and favorable plan contracting rather than with list price increases.

Mechanisms that drive branded net-price erosion

- Formulary substitution: PBMs steer to the lowest-cost A-rated generic equivalents.

- Rebate re-optimization: Branded holders must increase rebates to maintain preferred placement.

- Ingredient-level commoditization: In a same-class oral contraceptive, payer decisions often pivot on price and contracting terms rather than nuanced clinical differentiation.

Projection implication: Even if JUNEL FE remains dispensed at scale, net price is expected to trend down in real terms as competitive leverage shifts to generics and authorized versions.

What is the Orange Book status of JUNEL FE and how does it drive exclusivity risk?

JUNEL FE is an FDA-approved drug product with multiple generic equivalents and typically no long-lived formulation exclusivity that can override generic entry in most oral contraceptive classes.

How Orange Book status usually affects this category

- If key patents have expired, the Orange Book record does not block generic competition.

- If any listed patents persist, practical risk still depends on:

- Patent-by-patent validity and litigation outcomes

- Whether generic sponsors entered via section viii (without Paragraph IV) or Paragraph IV challenges

Projection implication: Pricing for JUNEL FE is best modeled as contract-driven rather than exclusivity-driven, because generic substitution is structurally entrenched in oral contraceptives.

When does JUNEL FE lose exclusivity and how does that change launch and substitution timelines?

For oral contraceptives, “loss of exclusivity” usually means:

- Final expiration of relevant patents for specific strengths/schedules/formulations

- Completion of any blocking period effects from new formulation patents

Market outcome after exclusivity:

Once patents covering a given labeled SKU lapse, substitution accelerates through:

- Increased generic utilization

- PBM re-pricing of preferred tiers

- Retail and mail channel switching driven by patient cost-sharing

Projection implication (category-level): Any remaining branded patent tail would likely create only incremental protection in net pricing. For most commercial models, JUNEL FE’s revenue path is governed by PBM contracting cycles and generic penetration, not by a single exclusivity event.

What patent estate strength exists for JUNEL FE, and which patents typically protect oral contraceptive brands?

For oral contraceptives, brand patent estates commonly include:

- Combinations (active ingredient ratios)

- Method-of-use (labeling and dosing schedules)

- Formulation (tablet composition and specific delivery attributes)

- Manufacturing (process claims)

However: In mature markets like oral contraception, many combination and method-of-use claims are already expired or structurally narrow, while formulation/manufacturing claims either:

- expire earlier, or

- face generic design-around options

Projection implication: For JUNEL FE pricing, the practical “IP barrier” is usually low. Generic substitution remains the dominant force.

What price trajectory should investors expect for JUNEL FE from 2025 to 2030?

Net-price projection framework for oral contraceptives

Because list prices are not the revenue driver under heavy rebate regimes, net-price projections should be expressed as directional net price indices relative to a baseline.

Assumption set used for projections (category consistent)

- Generics keep expanding coverage at major PBMs

- Branded contracts continue but at lower net price levels

- Dispensing volume growth is modest and driven by population and adherence more than by price

Projected net price trend (directional)

- 2025-2026: Continued compression as PBMs refresh formularies; limited upside unless a branded SKU regains preferred status.

- 2027-2029: More uniform erosion as additional low-cost competitors consolidate.

- 2030: Net price tends toward a stable floor determined by the lowest contracting generic basket and competitive parity.

Indicative scenario table (index-based)

Using 2024 net price index = 100 for JUNEL FE’s composite franchise:

| Year | Base case net price index | Low case (faster compression) | High case (contract protection) |

|---|---|---|---|

| 2025 | 97 | 94 | 99 |

| 2026 | 94 | 90 | 98 |

| 2027 | 91 | 86 | 96 |

| 2028 | 88 | 82 | 94 |

| 2029 | 86 | 79 | 92 |

| 2030 | 85 | 77 | 91 |

Interpretation: The base case implies a ~15% net price decline from 2024 to 2030. The low case implies ~23% decline. The high case implies a ~9% decline. These are net-price indices, not WAC.

How do payer mix and channel (retail vs mail) affect JUNEL FE pricing?

Payer mix is the dominant pricing lever:

- Higher commercial coverage with rebate sensitivity can preserve branded net price longer.

- Medicaid and lower-cost formularies typically accelerate generic utilization.

- Mail order often intensifies substitution to contracted low-cost alternatives.

Channel projection

- Retail: more churn when patient copay changes; branded may retain niche loyalty when copays remain manageable through programs.

- Mail: formulary controls tighten; branded is more dependent on PBM contract outcomes.

Projection implication: Net revenue can decline even with stable units if the mix shifts toward mail and high-substitution plans.

What generic entry risks exist for JUNEL FE’s specific strengths and NDCs?

For multi-SKU brands, the practical risk is SKU-level:

- A generic may enter one schedule/strength first and then expand across the product line.

- Substitution can be uneven depending on:

- NDC-level pricing and coverage

- patient switching friction

- stocking behavior at pharmacy chains

Risk profile likely across JUNEL FE

- High risk for NDCs with weaker formulary placement

- Lower risk for NDCs with established contracting and patient assistance alignment

Projection implication: Total franchise revenue will tend to track the weighted mix of the most favored NDCs, not the average brand price.

How does JUNEL FE compare with other oral contraceptive brands on pricing resilience?

In oral contraception:

- Brands with stronger formulary preference and rebate leverage show slower net erosion.

- Brands with weaker PBM positioning face faster compression.

Relative comparison logic

- If a competitor retains preferred placement longer, it can force price parity downward for all branded competitors.

- Brands positioned as “preferred” can sometimes stabilize net prices while volumes fall to generics more slowly.

Projection implication: For JUNEL FE, pricing resilience is likely moderate at best and mostly dependent on PBM contract duration and NDC favorability rather than on unique differentiation.

What litigation and settlement dynamics affect JUNEL FE pricing?

Litigation can affect timing of generic entry, but for mature oral contraceptive classes:

- Settlement often locks in specific entry timing or design constraints

- Real-world impact on pricing depends on whether settlement blocks entry in key plans

Projection implication: Without a clear, active “blocking” timeline, JUNEL FE pricing should be modeled as vulnerable to generic consolidation rather than dependent on litigation outcomes.

What FDA regulatory events could change JUNEL FE market access and price?

In oral contraceptives, FDA events most likely affect:

- Availability and supply stability (manufacturing changes, shortages)

- Labeling updates that influence prescriber or payer comfort

- Risk evaluations that can shift usage patterns

Price implication: Labeling changes are rarely sufficient to reverse net price compression in a generic-heavy category unless they create a new differentiation that payers must cover.

Commercial forecast: what drives JUNEL FE revenue through 2030?

Revenue decomposition

Revenue = Units × Net price

For JUNEL FE in this category:

- Unit growth is likely low single digits and linked to adherence and demographic demand

- Price is the primary driver of revenue decline

Base case revenue mechanics (directional)

- Units: flat to low growth

- Net price: steady compression

Indicative revenue index (2024 = 100)

| Year | Units index | Net price index | Revenue index (approx.) |

|---|---|---|---|

| 2025 | 101 | 97 | 98 |

| 2026 | 102 | 94 | 96 |

| 2027 | 103 | 91 | 94 |

| 2028 | 104 | 88 | 92 |

| 2029 | 105 | 86 | 90 |

| 2030 | 105 | 85 | 89 |

Result: A base-case path where revenue declines modestly to low-teens over the period, driven by net price erosion rather than major volume collapse.

Key assumptions behind the price projection model (how to interpret the numbers)

- WAC vs net: projections use net-price indices reflecting rebate and formulary contracting typical for oral contraceptives.

- No major supply disruption: shortages can temporarily raise net price and volume, but those events are not the default baseline.

- No new exclusivity moat: the franchise does not depend on a patent wall to resist generic substitution.

- Stable market demand: contraception demand is mature; pricing drives more of the P&L than unit expansion.

Key Takeaways

- JUNEL FE’s pricing power is constrained by mature generic competition; net price compression is the dominant forecast driver.

- 2025-2030: expect continued net-price erosion in the mid-teens range under a base case, with revenue declining modestly even if units hold.

- SKU mix matters: outcomes vary by NDC-level PBM favorability, mail vs retail dynamics, and contract renewal timing.

- Exclusivity and litigation can influence entry timing, but for this class the market outcome is typically contract and substitution-driven, not barrier-driven.

FAQs

1) How much of JUNEL FE revenue is driven by rebate contracting versus list price?

Most economic value comes from net pricing after rebates and plan contracts; list price changes typically do not translate directly into revenue.

2) What is the fastest lever that can improve JUNEL FE net pricing in the short term?

Formulary placement and renewal of preferred-tier contracts at major PBMs, paired with rebate renegotiations tied to utilization.

3) Do buy-down programs or patient assistance meaningfully protect JUNEL FE volume during generic expansions?

They can slow volume decline in specific channels, but they rarely stop net-price compression once PBMs re-anchor tiers.

4) How does mail-order utilization affect generic substitution for oral contraceptives like JUNEL FE?

Mail order usually accelerates substitution because pharmacy benefit design and preferred-contract enforcement are stronger.

5) What operational risks most affect JUNEL FE’s ability to maintain sales momentum?

Supply continuity, manufacturing changes, and formulary disruptions that shift patient coverage or pharmacy stocking patterns.

References (APA)

No sources were cited in this analysis.

More… ↓