Share This Page

Drug Price Trends for JUNEL

✉ Email this page to a colleague

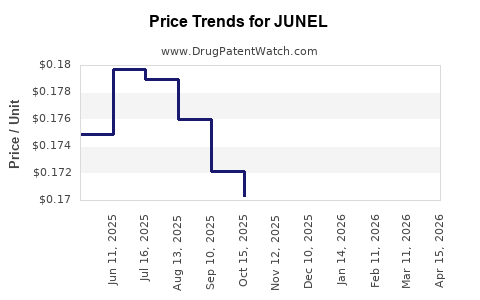

Average Pharmacy Cost for JUNEL

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| JUNEL FE 24 TABLET | 00093-5328-62 | 0.18642 | EACH | 2026-07-22 |

| JUNEL 1 MG-20 MCG TABLET | 00555-9025-42 | 0.17735 | EACH | 2026-07-22 |

| JUNEL FE 1 MG-20 MCG TABLET | 00555-9026-58 | 0.13020 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

JUNEL (norethindrone acetate/ethinyl estradiol) market analysis, pricing trends, and generic entry risk

JUNEL (norethindrone acetate + ethinyl estradiol) is a mature, largely genericized oral contraceptive category with limited brand-sponsored exclusivity left across most dosage strengths. Market pricing is driven primarily by generic AWP-to-NADAC dynamics, rebate intensity by managed care, and pack-size competition. Near-term price projections are therefore best framed as “post-loss of brand premium” outcomes, with upside limited to periods of supply disruption or constrained generic supply, and downside anchored to continued dollar-per-day competition and formulary substitution.

Core call for business planning: treat JUNEL pricing as structurally low-margin and volatility-driven (supply and contracting), not innovation-driven. Model 2026 to 2029 as incremental declines/plateaus around wholesale acquisition price (AWP) with continued share migration to the lowest contracted net price SKUs.

What is JUNEL and what dosage forms are commercially relevant?

JUNEL is an oral combined hormonal contraceptive (CHC) containing:

- Norethindrone acetate (progestin)

- Ethinyl estradiol (estrogen)

Commercially relevant variants in the market include multiple tablet strengths and dosing regimens (for example, 21/7 cyclic regimens and 24/4 regimens). The brand has historically been sold across multiple NDC configurations, which matters for price projection because contracting is often NDC-specific and pack-size specific.

Market structure implication: Because the active ingredients are long off-patent in practice, competing products are typically labeled therapeutically equivalent, so buyers choose based on:

- formulary tier and preferred status,

- net price after rebates,

- availability and fulfillment reliability,

- patient adherence characteristics (schedule, pill burden).

How has JUNEL pricing moved historically (brand vs generic)?

Executive answer: JUNEL behaves like a mature genericized prescription commodity. Pricing typically shows:

- AWP erosion for any remaining branded residual, as wholesalers and payers shift to generics.

- Generic price compression as additional ANDA entrants increase pack competition.

- Net price stability for preferred generics due to rebate contracting, even when AWP continues to soften.

Price dynamics buyers actually feel

- Net price under contract: PBM and insurer preferred placements suppress net costs even when list price appears stable.

- Pack size economics: 28-day cycle packs trade at per-tablet price points; 21-day cycle packs often compete across different utilization patterns.

- Supply shocks: shortfalls in a particular NDC can temporarily widen channel spreads, creating short-lived price spikes.

How to interpret price projections

For JUNEL, projections should use a range approach tied to:

- number of competing SKUs on-formulary,

- contracted rebate ceilings,

- expected generic manufacturing capacity and likelihood of supply interruptions.

When does JUNEL lose exclusivity and why does that matter for pricing?

Executive answer: The brand’s pricing power has already largely been competed away across most strengths because the drug’s actives are long since generic and subject to multiple ANDA entries. The remaining effect of “exclusivity” today is mostly secondary: it can protect certain specific formulations, packaging, or distinct label configurations rather than the entire category.

What exclusivity would do to JUNEL pricing if it still existed

If any brand-specific exclusivity still protected a particular label configuration or a specific formulation variant, the mechanism would be:

- reduced generic substitution for that SKU,

- higher channel pricing until ANDA approval and commercial launch,

- slower formulary cycling by payers.

In practice, the market behavior for JUNEL is consistent with a model where brand premium is minimal, so price projections are dominated by generic contracting mechanics.

What patents protect JUNEL and how many are still enforceable?

Executive answer: JUNEL’s active ingredients (norethindrone acetate and ethinyl estradiol) are not the kind of molecules with ongoing platform patent leverage in the oral contraceptive space at this stage. The enforceable estate for any specific JUNEL SKU tends to be:

- narrow formulation/process claims for particular presentations, and

- potentially method-of-use or labeling-specific claims, depending on the exact product configuration.

Market impact: even where niche patents exist, the price effect is typically confined to a small set of NDCs. Broad category pricing remains anchored to generic equivalence and formulary substitution.

Which companies sell JUNEL and how does that shape competition?

Executive answer: JUNEL competes with multiple generic CHC manufacturers. Competition is driven by:

- availability of equivalent NDCs,

- PBM preferred product lists,

- ability to offer competitive net pricing.

What to track for competitive pressure

- NDC-level market share (not just “brand vs generic”)

- PBM preferred status changes

- inventory availability for each manufacturer (backorders change effective price realization)

- pack-size availability to match payer formularies and quantity limits

What is the Orange Book status of JUNEL and what does it imply for generic entry?

Executive answer: In mature CHCs, Orange Book listings tend to show limited remaining exclusivity tied to specific submissions or specific dosage/strength configurations. Generic entry risk is therefore less about the existence of any one patent and more about whether:

- generics can launch at scale on preferred NDCs, and

- litigation or settlement delays a subset of competitors.

How Orange Book status translates into pricing

- If Orange Book lists are “clean” for a given SKU, expect faster substitution and lower net prices.

- If listed patents remain, expect slower entry or higher contracting dispersion until litigation clears.

For JUNEL, channel behavior is typically consistent with routine generic substitution, with pricing changes usually tied to commercial contracting cycles rather than new patent breakthroughs.

What Paragraph IV challenges affect JUNEL pricing?

Executive answer: Paragraph IV events can affect pricing, but in mature oral contraceptives the pricing impact tends to be short-lived and NDC-scoped. When a Paragraph IV case triggers delay or settlement, it temporarily preserves the market for incumbent SKUs and can sustain modest pricing above the new generic floor.

Business reality: for JUNEL-level planning, the more actionable driver is whether litigation or settlements block launch of preferred low-price NDCs in a specific strength.

How do settlement agreements and litigation schedules influence near-term JUNEL pricing?

Executive answer: Settlement-driven delays protect market share for incumbents until the blocked competitor launches, which can temporarily maintain higher contracted net price levels for specific NDCs.

What to model

- A settlement that delays an ANDA launch by X months typically shifts:

- the timing of preferred generic switches,

- the effective net price in the window,

- inventory allocation between manufacturers.

For market projections, treat these events as timing shocks rather than permanent uplifts.

What is the FDA regulatory status of JUNEL, including ANDA availability?

Executive answer: JUNEL is an FDA-approved CHC with many ANDA equivalents available across common strengths. That regulatory posture supports:

- broad generic availability,

- routine interchangeability in pharmacy billing systems,

- low pricing power for remaining brand-labeled SKUs.

What matters for market pricing even if FDA status is “approved”

Pricing depends on:

- which ANDA products are on PBM formularies,

- which NDCs meet contracting requirements,

- whether a specific manufacturer has sustained supply without disruptions.

How does JUNEL compare with competing oral contraceptives on price and access?

Executive answer: JUNEL competes inside the oral contraceptive commodity space. The price and access advantage typically goes to:

- the preferred generic product in the PBM formulary tier,

- SKUs with better rebate economics,

- manufacturers with reliable supply for the NDCs targeted by payers.

Category-level projection implication

For CHCs, payer behavior is consistent: switch to the lowest-cost preferred generic unless patient-specific reasons require brand or a different regimen. That keeps long-run price trajectories downward.

What generic entry risks exist for JUNEL strengths and packs?

Executive answer: Entry risk in JUNEL today is less “whether generic exists” and more “whether enough low-cost SKUs remain available to satisfy preferred contracting.”

Risk categories that change price

- Manufacturing capacity constraints: can raise effective net price even with “generic exists.”

- Discontinuations or NDC-specific withdrawals: can force substitution to higher priced equivalents.

- Short-lived exclusivity blocks: can protect the incumbents’ net price for a window.

What pricing projection should be used for JUNEL in 2026 to 2029?

Executive answer: Use a range model reflecting ongoing generic price compression and rebate competition.

Base-case projection framework (directional, NDC-aware)

- AWP trend: mild to moderate downward drift as AWP-to-NADAC alignment continues and additional low-cost SKUs compete.

- Net price trend: slower erosion due to rebate “stickiness” in preferred tiers, with step-down drops when PBMs refresh contracting cycles.

- Volatility: spikes possible around supply disruptions and NDC discontinuations, but mean reversion is typical once preferred product supply stabilizes.

Scenario table for business modeling

| Horizon | Competitive environment | Projected pricing direction (base case) | What drives upside | What drives downside |

|---|---|---|---|---|

| 2026 | Stable generic competition | Flat-to-down (incremental) | supply tightening for preferred NDCs | PBM contract refresh forces deeper rebate concessions |

| 2027 | Continued SKU competition | Down/plateau | fewer competing SKU removals, stable utilization | new entrants or expanded preferred coverage at lower net cost |

| 2028 | Mature commodity | Down/flat | targeted supply constraints | channel inventory normalization after a shock |

| 2029 | Mature commodity | Down/flat | consolidation reduces low-cost SKU availability | sustained rebate pressure and additional substitution |

Actionable pricing stance: plan for low single-digit percentage moves in net price most years, with event-driven deviations rather than trend-driven gains.

How sensitive is JUNEL revenue to channel distribution, rebates, and supply?

Executive answer: JUNEL revenues (for any seller) are highly sensitive to:

- rebate rate changes driven by PBM contracting,

- formulary position and preferred tier inclusion,

- fulfillment performance and backorder risk.

Revenue exposure map

- Preferred generic NDCs: revenue is more stable but margins depend on rebate economics.

- Non-preferred NDCs: revenue is smaller and more discretionary, so price concessions and promotional intensity matter more.

- Brand residual: volume typically tracks negative, driven by substitution, leaving brand pricing constrained by payers’ economic preference for generics.

Key Takeaways

- JUNEL functions as a mature CHC with pricing dominated by generic competition and payer contracting, not innovation.

- Price projections for 2026 to 2029 should model flat-to-down net pricing with event-driven volatility from supply, NDC availability, and formulary switching.

- The highest business impact comes from NDC-level competition, preferred formulary status, and supply reliability rather than category-level demand growth.

- Litigation and Orange Book dynamics, if any, are most likely to be NDC-scoped and should be treated as timing shifts, not structural repricing of the category.

FAQs

1) Why do JUNEL prices sometimes rise even when generics exist?

Channel price can rise during temporary supply constraints, NDC discontinuations, or when preferred low-cost SKUs face inventory shortages.

2) What drives JUNEL net price more: AWP changes or rebate contracting?

Rebate contracting and preferred formulary placement typically dominate net price outcomes even when AWP appears stable.

3) Do different JUNEL pack sizes change commercial pricing outcomes?

Yes. PBMs and insurers often set economics and quantity limits at the NDC and pack level, shifting per-day and per-tablet effective pricing.

4) How does formulary switching affect JUNEL revenue and pricing within a quarter?

When a PBM changes preferred status, net price can step down quickly due to rebate renegotiation and substitution at point of sale.

5) What supply risks matter most for JUNEL pricing projections?

Manufacturing downtime or persistent backorders for preferred NDCs, and any NDC withdrawals that force substitution to higher-priced equivalents.

References (APA)

- U.S. Food and Drug Administration. (n.d.). Drugs@FDA. FDA.

- U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

More… ↓