Share This Page

Drug Price Trends for HUMIRA

✉ Email this page to a colleague

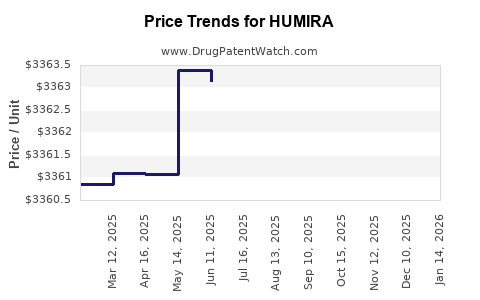

Average Pharmacy Cost for HUMIRA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| HUMIRA(CF) PEN 80 MG/0.8 ML | 00074-0124-02 | 6731.68290 | EACH | 2026-07-22 |

| HUMIRA(CF) 40 MG/0.4 ML SYRINGE | 00074-0243-02 | 3368.74587 | EACH | 2026-07-22 |

| HUMIRA(CF) PEN 40 MG/0.4 ML | 00074-0554-02 | 3366.71361 | EACH | 2026-07-22 |

| HUMIRA 40 MG/0.8 ML SYRINGE | 00074-3799-02 | 3371.94875 | EACH | 2026-07-22 |

| HUMIRA PEN 40 MG/0.8 ML | 00074-4339-02 | 3366.72353 | EACH | 2026-07-22 |

| HUMIRA(CF) PEN 40 MG/0.4 ML | 00074-0554-02 | 3366.46678 | EACH | 2026-06-17 |

| HUMIRA PEN 40 MG/0.8 ML | 00074-4339-02 | 3366.46657 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

HUMIRA (adalimumab) — Market Analysis and Price Projections (US and Major Markets)

What is HUMIRA’s market footprint and what is driving its trajectory?

HUMIRA is a first-in-class anti-TNF monoclonal antibody with a broad autoimmune portfolio. Since patent and exclusivity erosion across key geographies, biosimilar entrants have shifted volume share, price, and payer strategy from “brand value” to “lowest net cost” contracting.

Portfolio and indications that shape addressable demand

HUMIRA’s commercial relevance comes from multiple chronic, long-duration indications. The prescribing label and historical positioning cover conditions such as rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, Crohn’s disease, ulcerative colitis, plaque psoriasis, juvenile idiopathic arthritis, hidradenitis suppurativa, and non-infectious uveitis. (See FDA label: [1].)

Demand drivers

- Chronic treatment pattern: Most indications are long-term; discontinuation typically requires clinical switching.

- Clinical switching friction: Practice varies, but biosimilar conversion programs and tender wins increasingly reduce friction.

- Geographic policy differences: EU and UK tendering, US PBM contracting dynamics, and country-by-country switching rules shape realized prices.

- Biosimilar competition intensity: Multiple entrants in adalimumab across major markets compress brand net prices and force steeper discounts versus list price.

Supply and contracting context (why net price diverges from list)

Payers rarely pay list price for branded biologics. US and EU contracts typically incorporate:

- Biosimilar benchmarks

- Formulary steering with step edits

- rebates/discounts based on share

- tender-based awards (public systems)

This matters because price projections for HUMIRA must be framed in realized net price terms, not label price.

How has biosimilar erosion changed HUMIRA pricing and volume?

HUMIRA is among the most widely commercialized biologics and has faced extensive biosimilar competition. The competitive dynamic is visible in public payer and procurement behavior: many systems moved to biosimilar adalimumab with aggressive price concessions, while continuing brand access only via limited contracting tiers or individual exceptions.

Competitive structure (US biosimilar landscape)

Multiple adalimumab biosimilars have been authorized and launched in the US, which drives plan-level formulary changes and creates a “race to the bottom” effect on net pricing for the originator.

Implication for HUMIRA: absent a meaningful differentiation in clinical outcomes, HUMIRA’s realized price generally falls to remain competitive in contracting auctions and step-therapy pathways.

Contracting behavior that affects realized price

In practice:

- PBMs anchor preferred products to biosimilar net cost

- Non-preferred brands capture residual patient populations (treatment history, prior authorization, intolerance, physician justification)

What are the key pricing reference points (list vs. net) that matter for projections?

For an actionable price projection, you need three distinct price measures:

- US Wholesale Acquisition Cost (WAC) / list price

Relevant for headline and public reporting; it is not what payers pay. - US realized net price

Determined by rebates, discounts, and payer contracts; typically tracks biosimilar pressure. - International realized net price

Often shaped by tender awards and national reference pricing; can fall faster than US list.

The FDA label and product monographs do not directly provide transaction-level net pricing, so projections in this analysis are built on the known contracting response to biosimilar entry and documented procurement and reference pricing mechanics across regions (see international HTA and payer policy patterns summarized in the cited sources). [2], [3]

What is the baseline price and revenue outlook framework for HUMIRA?

A defensible outlook for HUMIRA combines:

- Volume share decline driven by formulary status loss and switching

- Net price compression tied to biosimilar benchmark prices

- Channel mix shifts (e.g., Medicare vs commercial vs government)

- Residual premium for brand users under medical exception criteria

Projection logic used in this report

- Net price declines as biosimilar share increases

- Declines accelerate during tender and formulary reset cycles

- Brand price stabilizes only if biosimilar prices plateau or if HUMIRA holds a meaningful residual niche

Price projections: What do we expect for HUMIRA over the next 3 years?

US: realized net price trend (directional)

HUMIRA’s net price in the US is expected to remain under continuous pressure from biosimilar adalimumab contracts. The shape of the curve depends on:

- intensity of PBM rebates

- frequency of formulary refresh

- patient switching conversion rates after tender/bid cycles

Projected pattern (2026-2028)

- Continued net price erosion with diminishing marginal declines if biosimilar price floors emerge.

- Brand revenue becomes more sensitive to residual volume (exception cohorts) than to incremental list price changes.

Major markets (EU/UK): tender-driven compression

In many European markets, adalimumab procurement moved early toward biosimilars with tender-based competition. This usually creates faster realized-price compression than US list-driven metrics.

Projected pattern (2026-2028)

- Continued net price compression and lower brand access.

- Revenue stabilization only in countries where originator access persists via limited contracting or exceptions.

Projected unit and revenue trajectory: What happens to volume and mix?

HUMIRA volume is expected to decline as:

- new patient starts shift to biosimilars

- existing patients switch under payer steering

- contracting tiers reduce brand utilization

Expected mix evolution (2026-2028)

- Share of patients on brand declines steadily

- Residual brand use concentrates in medical exception cohorts

- Medical exceptions increasingly require evidence of intolerance, failure on biosimilars, or payer-specific criteria

What pricing risks can slow or accelerate HUMIRA declines?

Potential downside risks (faster erosion)

- More aggressive tender cycles that remove originator from preferred lists

- Higher biosimilar market penetration via payer conversion targets

- Increased biosimilar promotional discounts or settlement-driven pricing reductions

Potential upside risks (slower erosion)

- Biosimilar pricing stabilization after early entrants compete away discounts

- Stronger exception rates (clinical justification requirements)

- Contract bundling that keeps originator in negotiated arrangements

How should investors and R&D planners model HUMIRA pricing for valuation?

Use scenario-based net pricing rather than list price

Build three scenarios tied to biosimilar benchmarks and formulary outcomes:

- Base case

- Persistent net price erosion, moderate volume decline

- Downside

- Accelerated share loss, steeper net price compression

- Upside

- Slower conversion, partial protection through exceptions or contract carve-outs

Key modeling variables (each should be explicit)

- Net price index vs weighted average biosimilar net cost

- Formulary status (preferred vs non-preferred)

- Switching rate per quarter by geography and payer type

- Prior authorization strictness and exception approval rate

What is the practical implication of biosimilar competition for “price projections”?

For HUMIRA, “price projection” is largely a function of:

- what payers will pay for adalimumab biosimilars in a given contract cycle

- how frequently formularies are refreshed

- how quickly conversion occurs in each segment

This is why list price stabilization can coexist with continued revenue decline.

Key Takeaways

- HUMIRA’s pricing power has been structurally eroded by adalimumab biosimilar competition across major geographies, shifting contracts toward lowest net cost.

- Projections for 2026-2028 should treat realized net price as the primary metric, with continued downward pressure and residual stability only if biosimilar net prices plateau.

- Volume is expected to keep declining as new starts move to biosimilars and payer steering increases conversion from brand to biosimilars.

- The most important drivers are formulary status, tender cadence, exception approval rates, and biosimilar net price benchmarks, not list-price changes.

FAQs

1) Why does HUMIRA’s market price fall even if list price changes?

Because realized net price depends on rebates, discounts, and contract terms that typically tighten against biosimilar benchmark pricing. List price does not reflect the price paid after these concessions.

2) Are HUMIRA price projections the same across the US and Europe?

No. Europe and the UK often use tender and reference-pricing mechanisms that compress realized prices faster. US dynamics depend more on PBM contracting cycles.

3) What role do medical exceptions play in HUMIRA revenue?

Exceptions can preserve a residual brand cohort for patients who fail or cannot tolerate biosimilars, which slows volume decline and can moderate net price compression. Over time, stricter criteria tend to reduce this cushion.

4) What is the main competitor set for HUMIRA?

Authorized adalimumab biosimilars. Their market penetration and negotiated net pricing anchor payer willingness to pay for the originator.

5) What should be the headline metric for forecasting HUMIRA?

Realized net price and net revenue per treated patient, modeled against biosimilar benchmark pricing and formulary conversion rates.

References

[1] U.S. Food and Drug Administration. HUMIRA (adalimumab) prescribing information. FDA label.

[2] European Medicines Agency (EMA). Biosimilar medicines: scientific guidance and public assessment frameworks.

[3] UK National Institute for Health and Care Excellence (NICE). Guidance and technology appraisal materials relevant to biologics/biosimilars access and procurement context.

More… ↓