Share This Page

Drug Price Trends for HEADACHE

✉ Email this page to a colleague

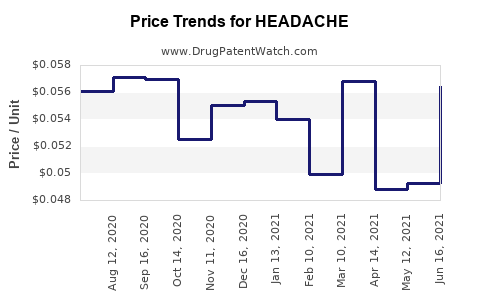

Average Pharmacy Cost for HEADACHE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| HEADACHE RLF 250-250-65 MG CPLT | 70000-0066-01 | 0.06369 | EACH | 2026-02-18 |

| HEADACHE RELIEF CAPLET | 70000-0146-01 | 0.06369 | EACH | 2026-02-18 |

| HEADACHE RLF 250-250-65 MG CPLT | 70000-0066-01 | 0.06345 | EACH | 2026-01-21 |

| HEADACHE RELIEF CAPLET | 70000-0146-01 | 0.06345 | EACH | 2026-01-21 |

| HEADACHE RLF 250-250-65 MG CPLT | 70000-0066-01 | 0.06462 | EACH | 2025-12-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

HEADACHE Drug Market Analysis and Price Projections

This report analyzes the global market for HEADACHE drugs, focusing on current market size, key therapeutic areas, competitive landscape, and future price projections. The market is driven by increasing prevalence of headache disorders, rising healthcare expenditure, and advancements in drug discovery.

What is the current global market size for HEADACHE drugs?

The global market for HEADACHE drugs was valued at approximately $30 billion in 2023. Projections indicate a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030, reaching an estimated $41.5 billion by the end of the forecast period. This growth is primarily attributed to the expanding patient population experiencing chronic and episodic headaches, including migraines, tension-type headaches, and cluster headaches. The increasing awareness and diagnosis rates of headache disorders also contribute to market expansion.

What are the key therapeutic areas within the HEADACHE drug market?

The HEADACHE drug market is segmented into several key therapeutic areas, reflecting the diverse nature of headache disorders and their treatment approaches:

- Migraine: This is the largest segment, driven by the development of novel CGRP inhibitors and triptans. Migraine affects an estimated 15% of the global population and is characterized by severe, often debilitating, head pain.

- Tension-Type Headache (TTH): The most common type of headache, TTH, is typically less severe than migraine but can still significantly impact quality of life. Treatment focuses on over-the-counter (OTC) analgesics and, in chronic cases, preventative medications.

- Cluster Headache: Though less prevalent than migraine or TTH, cluster headaches are intensely painful and represent a significant unmet need for effective acute and preventative treatments.

- Other Headache Disorders: This category includes secondary headaches caused by underlying medical conditions, medication overuse headaches, and trigeminal autonomic cephalgias.

Who are the leading players in the HEADACHE drug market?

The HEADACHE drug market is characterized by a mix of established pharmaceutical giants and emerging biopharmaceutical companies. Key players include:

- AbbVie Inc.: With its significant presence in migraine treatment, notably through Ubrelvy (ubrogepant) and Qulipta (atogepant), AbbVie is a major force.

- Eli Lilly and Company: Known for its CGRP antagonist Emgality (galcanezumab-gnlm), Lilly is a significant contributor to the migraine market.

- Teva Pharmaceutical Industries Ltd.: Teva offers a broad portfolio of generic and branded headache medications, including sumatriptan.

- Pfizer Inc.: Pfizer's portfolio includes OTC analgesics and prescription medications relevant to headache management.

- Amgen Inc.: Amgen holds a stake in the migraine market with Aimovig (erenumab-aooe), a CGRP inhibitor.

- Novartis AG: Novartis contributes with treatments like OnabotulinumtoxinA (Botox) for chronic migraine.

- Biohaven Pharmaceutical Holding Company Ltd. (now part of Pfizer): Biohaven's Nurtec ODT (rimegepant) is a significant oral CGRP antagonist for acute migraine treatment and prevention.

What are the primary drivers of market growth?

Several factors are propelling the growth of the HEADACHE drug market:

- Increasing Prevalence of Headache Disorders: Global estimates suggest that headache disorders are among the most common neurological conditions, affecting hundreds of millions worldwide. Factors such as stress, lifestyle changes, and an aging population contribute to this prevalence.

- Advancements in Drug Discovery and Development: The development of targeted therapies, particularly CGRP antagonists, has revolutionized migraine treatment. These novel mechanisms of action offer improved efficacy and tolerability compared to older drug classes.

- Rising Healthcare Expenditure: Increased healthcare spending globally, especially in emerging economies, allows for greater access to advanced diagnostic tools and novel therapeutic options for headache management.

- Growing Awareness and Diagnosis Rates: Greater public awareness campaigns and improved diagnostic capabilities by healthcare professionals lead to more accurate and timely diagnoses, thereby increasing the demand for effective treatments.

- Expansion of Generic and Biosimilar Markets: The availability of generic versions of established headache medications, and the eventual emergence of biosimilars for biologic treatments, are expected to increase affordability and patient access, further stimulating market volume.

- Focus on Preventative Therapies: There is a growing emphasis on preventative treatment strategies for chronic headache disorders, leading to increased use of medications aimed at reducing headache frequency and severity.

What are the key challenges facing the HEADACHE drug market?

Despite the positive growth trajectory, the HEADACHE drug market encounters several challenges:

- High Cost of Novel Therapies: Advanced treatments, such as CGRP inhibitors, are often associated with high price tags, limiting accessibility for a significant portion of the patient population, particularly in regions with less robust healthcare systems.

- Adverse Event Profiles of Some Medications: While newer drugs generally have improved safety profiles, some older treatments, and even some newer ones, can have side effects that impact patient adherence and physician prescribing patterns.

- Diagnostic Challenges and Misdiagnosis: Accurately diagnosing the specific type of headache disorder can be challenging, leading to delays in appropriate treatment or the use of ineffective therapies.

- Regulatory Hurdles: The stringent regulatory approval process for new drug entities requires extensive clinical trials, which are costly and time-consuming.

- Drug Resistance and Treatment Failure: Some patients may not respond to initial treatments, necessitating a trial-and-error approach to find an effective therapy, which can be frustrating for patients and healthcare providers.

- Stigma Associated with Headache Disorders: Migraine and other severe headache disorders are sometimes not taken seriously by the public and even some healthcare professionals, leading to undertreatment and lack of support for patients.

What is the projected price trend for HEADACHE drugs over the next five to seven years?

The price trend for HEADACHE drugs is expected to be multifaceted, with significant variation based on drug class, therapeutic indication, and market dynamics.

- CGRP Inhibitors: The prices for novel CGRP inhibitors, both monoclonal antibodies (mAbs) and oral small molecules, are expected to remain at a premium. However, with increasing market competition and the potential introduction of biosimilars for mAbs in the longer term (beyond the seven-year window), some price stabilization or gradual decline may occur. For oral CGRP antagonists, while still high, competition among manufacturers could lead to slight price adjustments to gain market share. Current pricing for these therapies often ranges from $6,000 to $10,000 per year per patient.

- Triptans: Generic triptans are widely available and are expected to maintain their cost-effectiveness. Brand-name triptans may see modest price increases, but their market share is likely to be further eroded by generics.

- OTC Analgesics: Prices for OTC pain relievers (e.g., ibuprofen, acetaminophen) used for tension-type headaches are likely to remain stable, with incremental increases aligned with general inflation.

- Preventative Therapies (Non-CGRP): Established preventative medications for migraine, such as certain anticonvulsants and antidepressants, will continue to be available in generic forms, maintaining affordability.

- OnabotulinumtoxinA (Botox): For chronic migraine, Botox treatments are administered every three months. The cost per treatment session is substantial, and this pricing is expected to continue, given its established efficacy and specific indication.

Overall, the market is likely to see a divergence: continued high pricing for the newest, most targeted therapies with demonstrated superior efficacy, coupled with the sustained affordability of generic and older-generation treatments. Payor negotiations and the development of value-based pricing models will also play a significant role in shaping actual out-of-pocket costs for patients and reimbursement levels for manufacturers.

What is the impact of patent expiries on the HEADACHE drug market?

Patent expiries are a critical factor influencing market dynamics and pricing. As patents for blockbuster headache medications expire, generic manufacturers can enter the market, leading to a significant reduction in drug prices.

- Triptans: Many triptan patents have already expired, resulting in a robust generic market that now dominates this class of drugs. This has made acute migraine treatment more accessible.

- CGRP Inhibitors: The patent landscape for CGRP inhibitors is more complex. Monoclonal antibodies, being biologics, have longer patent protection periods and are also subject to the eventual development of biosimilars. Oral CGRP antagonists, being small molecules, generally have shorter patent lives compared to biologics. The expiration of key patents for these newer agents will usher in generic competition, leading to price erosion for these currently high-cost therapies, though this is expected to occur in the latter half of the forecast period for some.

- Other Classes: Patents for older classes of headache medications, such as anticonvulsants and antidepressants used prophylactically, have long expired, ensuring a competitive generic market.

The introduction of generics typically leads to a price drop of 70-90% for a given drug within a few years of patent expiry and generic entry. This trend will continue to impact the overall revenue generated by specific molecules as their exclusivity periods wane.

What are the future trends and innovations in HEADACHE drug development?

Future trends in HEADACHE drug development are focused on improving efficacy, reducing side effects, and offering more convenient administration methods.

- Next-Generation CGRP Modulators: Research continues on developing CGRP modulators with potentially improved pharmacokinetics, reduced dosing frequency, or novel mechanisms of action to overcome resistance.

- Neuromodulation Devices: Non-pharmacological approaches, such as external trigeminal nerve stimulation (e.g., Cefaly) and vagus nerve stimulation, are gaining traction as adjunctive or alternative treatments, particularly for chronic and refractory headache types. These devices offer drug-free options.

- Personalized Medicine: Advancements in pharmacogenomics and biomarker identification aim to predict individual patient responses to specific headache medications, enabling more personalized treatment strategies. This could reduce trial-and-error approaches.

- Broader Spectrum Neurological Targets: Exploration into other neurotransmitter systems and neurological pathways implicated in headache pathophysiology beyond CGRP is ongoing, potentially leading to entirely new drug classes.

- Improved Delivery Systems: Development of faster-acting formulations, such as orally disintegrating tablets, nasal sprays, and injectables with less frequent dosing, is a key focus for improving patient convenience and adherence.

- Understanding the Gut-Brain Axis: Emerging research suggests a link between gut microbiota and headache disorders, opening potential avenues for therapeutic interventions targeting the gut-brain axis.

Key Takeaways

The global HEADACHE drug market, valued at $30 billion in 2023, is projected to grow to $41.5 billion by 2030, driven by increasing prevalence, improved diagnostics, and novel therapies like CGRP inhibitors. Migraine treatment remains the largest segment. Key players include AbbVie, Eli Lilly, and Teva. Challenges include the high cost of new drugs and diagnostic hurdles. Patent expiries will continue to introduce generic competition, particularly impacting older drug classes and eventually newer ones like CGRP inhibitors. Future innovations focus on next-generation CGRP modulators, neuromodulation devices, and personalized medicine approaches.

FAQs

-

How will biosimilars for CGRP monoclonal antibodies affect pricing? The introduction of biosimilars for CGRP monoclonal antibodies, expected in the later part of the forecast period, will likely lead to significant price reductions for these treatments, mirroring the impact seen with biosimilars in other therapeutic areas. This could range from 20% to 50% initially, with further declines as competition increases.

-

What is the expected impact of medication overuse headache on the market? Medication overuse headache (MOH) is a growing concern that can complicate treatment strategies. While not a direct market segment, managing MOH often involves discontinuing offending medications and implementing preventative therapies, indirectly influencing the demand for different drug classes. It necessitates careful patient education and physician oversight.

-

Are there any emerging treatment paradigms for cluster headaches? Cluster headaches, while a smaller market, are seeing research into novel acute treatments and preventative strategies. This includes exploring new neuromodulation techniques and targeted drug development beyond current standards of care like sumatriptan injections and oxygen therapy.

-

What role will digital health and AI play in HEADACHE drug development and treatment? Digital health platforms and AI are expected to contribute to headache management by aiding in symptom tracking, diagnosis, and patient monitoring. AI may also accelerate drug discovery by identifying novel drug targets and predicting patient response to therapies.

-

How does the regulatory environment in different regions impact HEADACHE drug access and pricing? Regulatory approvals by agencies like the FDA (U.S.) and EMA (Europe) are critical for market entry. Pricing and reimbursement policies vary significantly by country. For example, national health systems in Europe may negotiate prices more aggressively than in the U.S., leading to differential access and cost structures for HEADACHE drugs globally.

Citations

[1] Global Market Insights. (2023). Headache Therapeutics Market Size, Share & Trends Analysis Report. [2] Grand View Research. (2023). Headache Therapeutics Market Size, Share & Trends Analysis Report. [3] Fierce Pharma. (2023). The top 10 migraine drugs, ranked by sales. [4] Evaluate Vantage. (2023). Migraine: global drug forecast and market analysis. [5] U.S. Food & Drug Administration. (n.d.). Drug Approval Process.

More… ↓