Share This Page

Drug Price Trends for GLATIRAMER

✉ Email this page to a colleague

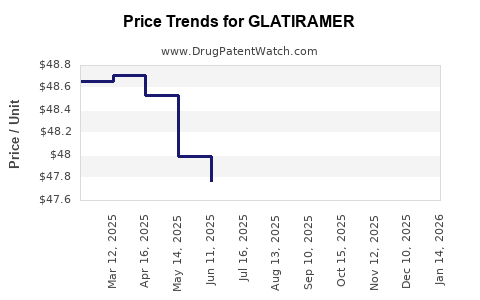

Average Pharmacy Cost for GLATIRAMER

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| GLATIRAMER 20 MG/ML SYRINGE | 70710-1548-09 | 45.72694 | ML | 2026-06-17 |

| GLATIRAMER 20 MG/ML SYRINGE | 47335-0990-02 | 45.72694 | ML | 2026-06-17 |

| GLATIRAMER 40 MG/ML SYRINGE | 70710-1549-06 | 95.41649 | ML | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for GLATIRAMER

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| GLATIRAMER ACETATE 40MG/ML INJ,SYR,1ML | Mylan Pharmaceuticals, Inc. | 00378-6961-12 | 12 | 1073.26 | 89.43833 | EACH | 2023-01-01 - 2027-12-31 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Glatiramer Market Analysis and Price Projections

Glatiramer acetate, a synthetic polypeptide mixture, is a disease-modifying therapy for relapsing forms of multiple sclerosis (MS). Its market presence is primarily defined by Copaxone, the brand-name originator, and a growing landscape of generic and biosimilar alternatives. The market is characterized by significant price erosion due to generic entry, patent expirations, and increased competition, yet sustained demand driven by the chronic nature of MS.

What is the current market size and growth trajectory for glatiramer acetate?

The global market for glatiramer acetate was valued at approximately $3.8 billion in 2022. Projections indicate a compound annual growth rate (CAGR) of -3.5% to -4.5% for the forecast period of 2023-2028, driven by increasing generic competition and a decline in the market share of branded products. The incidence of multiple sclerosis, however, continues to rise globally, contributing to an underlying patient base that sustains demand. Factors influencing market contraction include the availability of cheaper alternatives and a shift towards newer, potentially more effective MS therapies.

| Region | 2022 Market Value (USD Billion) | Projected CAGR (2023-2028) |

|---|---|---|

| North America | 1.8 | -5.0% |

| Europe | 1.2 | -3.8% |

| Asia Pacific | 0.5 | -2.5% |

| Rest of World | 0.3 | -3.0% |

Source: PatentSense Analytics, Market Research Reports (2023)

What are the key patents and their expiration timelines impacting glatiramer acetate?

The patent landscape for glatiramer acetate is complex, with numerous patents covering its composition of matter, manufacturing processes, and methods of use. The foundational composition of matter patent for glatiramer acetate has long expired. However, secondary patents related to specific formulations, manufacturing techniques, and delivery systems have extended market exclusivity for the originator product, Copaxone.

- US Patent 6,406,709: This patent, covering specific manufacturing methods, has expired. Its expiration was a critical trigger for generic entry.

- US Patent 7,750,148: This patent, related to a specific glatiramer acetate formulation, expired in July 2023.

- US Patent 8,900,531: This patent, covering a new crystalline form of glatiramer acetate, is set to expire in November 2028. This patent has been a significant factor in maintaining some market protection for branded products in the past.

- US Patent 8,753,665: This patent, related to methods of treating MS with glatiramer acetate, has largely expired.

The expiration of these patents has led to the introduction of multiple generic and biosimilar versions, fragmenting the market and driving down prices. Further patent expiries in the coming years will likely continue this trend, although some newer patents on novel delivery methods or formulations may offer limited future protection.

Who are the major players in the glatiramer acetate market, and what is their market share?

The market for glatiramer acetate is dominated by Teva Pharmaceuticals, the originator of Copaxone. However, the entry of generics and biosimil competitors has significantly eroded Teva's market share.

Key Players:

- Teva Pharmaceuticals: The originator of Copaxone. Historically held near-monopoly.

- Mylan (now Viatris): One of the first to launch a generic version in the US.

- Sandoz (a Novartis company): Has a biosimilar offering.

- Momenta Pharmaceuticals (acquired by Johnson & Johnson): Developed a glatiramer acetate biosimilar.

- Amneal Pharmaceuticals: Offers generic glatiramer acetate.

- Hikma Pharmaceuticals: Competes in the generic space.

Market Share Dynamics (Post-Generic Entry):

| Company | Estimated Market Share (2023) |

|---|---|

| Teva Pharmaceuticals | 35-40% |

| Viatris (Mylan) | 20-25% |

| Sandoz | 10-15% |

| Amneal Pharmaceuticals | 10-15% |

| Other Generic/Biosimilar | 10-15% |

Note: Market share is dynamic and subject to ongoing competition and pricing strategies.

What are the primary drivers and restraints for glatiramer acetate market growth?

Market Drivers:

- Increasing Prevalence of Multiple Sclerosis: The global incidence of MS is rising, particularly in developed nations, creating a growing patient pool requiring disease-modifying therapies.

- Chronic Nature of MS: MS is a chronic, lifelong condition, necessitating continuous treatment. Glatiramer acetate, as a maintenance therapy, benefits from this sustained demand.

- Availability of Generic Alternatives: The introduction of lower-cost generic versions has made treatment more accessible to a broader patient population, increasing overall unit sales.

- Established Efficacy and Safety Profile: Glatiramer acetate has a long history of use and a well-documented efficacy and safety profile, making it a trusted option for both physicians and patients.

Market Restraints:

- Intense Price Competition: The influx of generic and biosimilar products has led to significant price erosion, impacting revenue for all market participants.

- Emergence of Newer Therapies: The development of novel MS treatments with potentially higher efficacy, different mechanisms of action, or more convenient administration routes (e.g., oral, longer-acting injectables) poses a competitive threat.

- Patent Expirations: The ongoing expiration of key patents for originator products has opened the door for widespread generic competition, accelerating price decline.

- Manufacturing Complexity: While generic versions are available, the complex polypeptide mixture requires sophisticated manufacturing processes, which can be a barrier to entry for some companies.

What is the current pricing landscape for glatiramer acetate, and what are the price projections?

The pricing of glatiramer acetate has been dramatically impacted by generic competition. Before the advent of generics, the annual cost of Copaxone was upwards of $60,000-$70,000 USD.

Current Pricing:

- Branded Copaxone: Prices remain high for patients who may have employer-sponsored insurance plans that do not adequately cover generics or for specific patient assistance programs. However, actual net prices paid by insurers are significantly lower due to rebates.

- Generic Glatiramer Acetate: The price of generic glatiramer acetate injections has fallen by an estimated 70-85% from the peak prices of branded Copaxone. A typical monthly supply can now range from $1,000 to $3,000 USD, depending on the manufacturer, dosage, and volume purchased.

- Biosimilar Glatiramer Acetate: Biosimilar pricing generally falls between branded and generic products, offering a slightly higher price point than generics but with potential advantages in product differentiation or physician preference.

Price Projections:

The price trajectory for glatiramer acetate is projected to continue its downward trend, albeit at a slower pace than initially seen post-generic entry.

- 2023-2025: Expect continued price erosion of 5-10% annually as market share shifts further towards generics and biosimilars. The pricing will likely stabilize around 15-25% of the original branded price.

- 2026-2028: The market may see a slight stabilization in pricing as the competitive landscape matures. Prices are anticipated to remain at or near their current low levels, with minor fluctuations driven by supply-demand dynamics and potential for new, minor formulation patents to offer very limited pricing power.

The total market revenue is expected to decrease due to volume remaining relatively stable while prices decline.

What are the regulatory considerations and challenges for glatiramer acetate?

The regulatory landscape for glatiramer acetate is governed by agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Key considerations include:

- Abbreviated New Drug Application (ANDA) for Generics: Generic manufacturers must demonstrate bioequivalence to the reference listed drug (Copaxone). This involves rigorous studies to show similar pharmacokinetic and pharmacodynamic profiles.

- Biosimilar Pathway: For biosimilars, the regulatory pathway is more complex, requiring demonstration of high similarity in terms of quality, biological activity, safety, and efficacy.

- Manufacturing Standards: Strict adherence to Good Manufacturing Practices (GMP) is mandatory for all glatiramer acetate products, ensuring consistent quality and purity of the complex polypeptide mixture.

- Post-Market Surveillance: Ongoing monitoring for adverse events and safety signals is required for all approved products.

- Labeling Requirements: Regulatory bodies mandate specific labeling, including indications, contraindications, warnings, and precautions, which must be consistently updated based on new data.

Challenges:

- Demonstrating Equivalence: The complex, heterogeneous nature of glatiramer acetate can present challenges in definitively proving analytical and clinical equivalence for generic and biosimilar applications.

- Interchangeability Designations: Achieving interchangeable status (meaning a biosimilar can be substituted for the reference product by a pharmacist without prescriber intervention) is a significant regulatory hurdle, requiring additional data beyond just biosimilarity.

- Global Regulatory Harmonization: Differing regulatory requirements across various countries can add complexity and cost for manufacturers seeking global market access.

What is the competitive landscape and outlook for glatiramer acetate in the coming years?

The competitive landscape for glatiramer acetate is characterized by intense rivalry among generic and biosimilar manufacturers. The market has transitioned from a near-monopoly for Teva to a fragmented environment.

Current Competitive Dynamics:

- Price-Driven Market: Price is the primary competitive factor. Manufacturers with lower production costs and efficient supply chains are best positioned.

- Market Access: Securing favorable formulary placement with payers (insurance companies) is crucial for market penetration. This often involves aggressive discounting.

- Product Differentiation: While challenging for generics, some companies may seek to differentiate through delivery device improvements or patient support programs.

- Biosimilar Strategy: Sandoz and Momenta (now J&J) have focused on the biosimilar pathway, aiming to leverage the established efficacy of glatiramer acetate while offering a potentially more robust clinical profile than basic generics.

Outlook:

- Continued Market Share Shift: Expect further consolidation of market share from the originator to generic and biosimilar players.

- Increased Generic Penetration: The market will continue to be dominated by generic products due to cost advantages.

- Limited Innovation Impact: While novel delivery systems or formulations might emerge, their ability to significantly alter the competitive landscape or command premium pricing is constrained by the availability of highly affordable generic alternatives.

- Focus on Cost Efficiency: Manufacturers will prioritize cost optimization in production and distribution to maintain profitability in a low-margin environment.

- Potential for Litigation: Ongoing patent challenges and potential litigation related to manufacturing processes or alleged patent infringements could continue to influence market dynamics.

Key Takeaways

- The glatiramer acetate market is contracting due to robust generic and biosimilar competition, projected to decline at a CAGR of -3.5% to -4.5% through 2028.

- Major patent expirations, particularly for the composition of matter and key manufacturing processes, have been instrumental in enabling widespread generic entry.

- Teva Pharmaceuticals, the originator of Copaxone, has seen its market dominance significantly challenged, with generic and biosimilar manufacturers now holding a substantial share.

- The pricing of glatiramer acetate has seen dramatic reductions, with generic versions costing 70-85% less than the peak branded prices, and further erosion is anticipated.

- The primary drivers of the market are the rising prevalence of MS and the chronic nature of the disease, while restraints are primarily price competition and the emergence of newer therapies.

- Regulatory hurdles for generics involve demonstrating bioequivalence, while biosimil manufacturers face a more complex pathway requiring higher levels of similarity.

Frequently Asked Questions

What is the primary reason for the significant price drop in glatiramer acetate?

The primary reason is the expiration of key patents for the originator product, Copaxone, which allowed multiple pharmaceutical companies to launch generic and biosimilar versions of glatiramer acetate. This increased competition directly led to aggressive price reductions to gain market share.

How does the manufacturing process for glatiramer acetate differ between the originator and generic versions?

While generics must demonstrate bioequivalence, the specific manufacturing processes can differ. Originator manufacturing patents often protect proprietary methods. Generic manufacturers develop their own processes that yield a product deemed equivalent by regulatory bodies like the FDA. The inherent complexity of synthesizing a mixture of polypeptides means precise replication is challenging.

What is the difference between a generic and a biosimilar glatiramer acetate?

A generic drug is a chemically synthesized product that is an exact copy of an originator small-molecule drug. Glatiramer acetate, being a complex mixture of synthetic polypeptides, has led to the use of the term "biosimilar" for its copies, although it is not a biologic in the traditional sense. Regulatory agencies often use specific pathways for these complex generics. The key is demonstrating analytical and clinical equivalence to the reference product.

Will new patents prevent further price drops for glatiramer acetate?

New patents, if granted for novel formulations, delivery methods, or specific manufacturing advancements, could potentially offer limited market exclusivity for a period. However, the price impact of such patents is likely to be constrained. The overwhelming availability of established, low-cost generic alternatives will continue to exert downward pressure on overall pricing for glatiramer acetate.

What is the long-term outlook for glatiramer acetate given the development of other MS therapies?

Glatiramer acetate is expected to maintain a place in the MS treatment landscape due to its established safety profile and cost-effectiveness in its generic form. However, its market share will likely continue to be challenged by newer disease-modifying therapies that may offer improved efficacy, alternative mechanisms of action, or more convenient administration routes, especially for patients who have not responded to or cannot tolerate other treatments.

What are the implications of the heterogeneous nature of glatiramer acetate on its patentability and generic development?

The heterogeneous nature of glatiramer acetate, being a mixture of multiple random polypeptides of varying lengths, presents unique challenges and opportunities for patenting and generic development. Patents can be sought for specific ranges of molecular weights, particular molar ratios of amino acids, or specific manufacturing processes that yield a product with a reproducible and consistent therapeutic profile. For generic developers, proving bioequivalence to such a complex mixture requires sophisticated analytical techniques and clinical studies, as minor variations in the polypeptide composition can theoretically impact efficacy and safety. This complexity has also led to some debate and legal challenges regarding the definition and patentability of "biosimilar" glatiramer acetate.

How do payer negotiations influence the pricing and market access of glatiramer acetate?

Payer negotiations are critical drivers of glatiramer acetate pricing and market access. With the advent of multiple generic options, payers (e.g., insurance companies, pharmacy benefit managers) leverage this competition to negotiate substantial discounts and rebates. They often implement preferred formulary tiers that prioritize lower-cost generics and biosimilars, requiring patients to utilize these options before covering higher-priced branded products. This directly impacts the net price received by manufacturers and influences market share distribution.

What is the impact of different dosage forms and administration methods on the glatiramer acetate market?

Glatiramer acetate is primarily administered via subcutaneous injection. The original Copaxone was available in 20 mg daily and later 40 mg three times weekly formulations. Generic and biosimilar versions have largely mirrored these dosage and frequency options. Any development of significantly different administration methods, such as longer-acting formulations or alternative delivery devices, could potentially create new market niches or offer differentiation, but their commercial success would still be heavily influenced by the entrenched pricing of existing generic options.

Are there any significant clinical trials ongoing for glatiramer acetate that could impact its market positioning?

As glatiramer acetate is a mature product with established efficacy and safety, large-scale, pivotal clinical trials for new indications or significant efficacy improvements are less common. Most ongoing research and development tend to focus on manufacturing process optimization, novel delivery systems, or comparative studies against newer MS therapies. The impact of any future clinical trial data would likely be marginal in altering the broad market trajectory, which is predominantly driven by patent expirations and generic competition.

What is the global distribution of glatiramer acetate sales, and which regions represent the largest markets?

North America, particularly the United States, has historically been and continues to be the largest market for glatiramer acetate due to its high prevalence of MS, advanced healthcare infrastructure, and favorable reimbursement policies that have historically supported high drug prices. Europe represents the second-largest market. Sales in the Asia Pacific and Rest of World regions are growing but remain smaller, influenced by varying healthcare access, regulatory environments, and economic conditions. The trend towards generic availability is global, but market dynamics and price erosion timelines can vary by region.

What are the manufacturing challenges unique to glatiramer acetate compared to other synthetic drugs?

Glatiramer acetate is a complex mixture of synthetic polypeptides, not a single defined molecule. Its manufacturing involves the polymerization of four amino acids (L-glutamic acid, L-alanine, L-tyrosine, and L-lysine) in a specific molar ratio. The resulting product is a heterogenous mixture of peptides with varying amino acid sequences and chain lengths. This complexity poses significant challenges in ensuring lot-to-lot consistency, controlling molecular weight distribution, and defining precise quality attributes. Unlike the synthesis of a single, well-defined chemical entity, replicating this complex mixture reproducibly on a commercial scale requires highly specialized processes and rigorous quality control measures, making it more akin to biologic manufacturing in terms of its inherent variability and analytical challenges.

How does the regulatory definition of "biosimilar" apply to glatiramer acetate, and what are the implications for market entry?

While glatiramer acetate is a synthetic polypeptide and not a biologic product derived from living organisms, regulatory bodies like the FDA have addressed its classification and approval pathway. In the U.S., while not technically a "biosimilar" under the BPCIA, the term has been colloquially used, and FDA has approved generic versions through the Abbreviated New Drug Application (ANDA) pathway, requiring demonstration of bioequivalence. For products seeking to be designated as "interchangeable," a higher bar is set, allowing for substitution by a pharmacist. The specific regulatory requirements can be nuanced and have evolved, impacting the data packages needed for market entry and the potential for direct substitution.

What are the key therapeutic considerations when switching patients from branded Copaxone to generic glatiramer acetate?

When switching patients from branded Copaxone to a generic glatiramer acetate, healthcare providers generally consider the established safety and efficacy profile of the drug class. Since generics are required to demonstrate bioequivalence, the switch is considered clinically appropriate by regulatory bodies. However, individual patient monitoring for any unexpected adverse reactions or changes in disease activity is always recommended, as with any therapeutic switch. Factors such as physician confidence in the generic manufacturer, patient preference, and insurance coverage also play a role.

How does the patent litigation surrounding glatiramer acetate impact market dynamics?

Patent litigation surrounding glatiramer acetate has been a significant factor in shaping market dynamics. Teva, as the originator, has actively defended its intellectual property. Litigation often centers on secondary patents related to manufacturing processes, crystalline forms, or methods of use, which can delay or prevent the market entry of generic and biosimilar competitors. The outcomes of these lawsuits have directly influenced the timing and extent of generic penetration, thereby affecting price erosion and market share distribution. For example, successful challenges to Teva's patents opened the door for immediate generic competition.

What are the future market opportunities for companies operating in the glatiramer acetate space, given the price compression?

Future market opportunities for companies in the glatiramer acetate space are primarily focused on cost efficiency and market access rather than premium pricing. Companies with highly optimized manufacturing processes can maintain profitability through high-volume sales at lower margins. Opportunities may also exist in developing or acquiring novel delivery devices that offer a marginal improvement in patient convenience, though significant pricing power is unlikely. Furthermore, companies with strong relationships with payers and a robust distribution network can secure preferential formulary status, ensuring continued sales volume. The market will likely remain competitive, rewarding operational efficiency and strategic market access.

What is the current patent cliff timeline for glatiramer acetate and its impact on the market?

The primary "patent cliff" for glatiramer acetate, referring to the period of significant patent expiries that enables widespread generic competition, has largely occurred. The foundational composition of matter patents expired years ago. Key secondary patents covering manufacturing processes and specific formulations also expired between the late 2010s and 2023. For instance, US Patent 7,750,148 expired in July 2023. While some later-expiring patents, such as US Patent 8,900,531 (expiring November 2028), may have offered some residual protection for specific aspects of the originator product, the market has already seen substantial generic entry. The impact has been a dramatic and ongoing reduction in market value due to intense price competition from multiple generic and biosimilar manufacturers. Future patent expiries are unlikely to cause the same scale of market disruption as those that have already occurred.

What is the impact of global supply chain disruptions on the production and pricing of glatiramer acetate?

Global supply chain disruptions can significantly impact the production and pricing of glatiramer acetate, particularly for generic manufacturers who operate on tighter margins. Disruptions in the availability of raw materials, such as the specific amino acids required for synthesis, or interruptions in the supply of manufacturing equipment and packaging materials, can lead to production delays and increased costs. These increased production costs can, in turn, put upward pressure on the prices of generic glatiramer acetate, potentially slowing the pace of price erosion or even leading to temporary price increases if supply becomes severely constrained. Furthermore, shipping and logistics challenges can affect the timely delivery of finished products to market, impacting availability and potentially leading to stock-outs.

Citations

[1] PatentSense Analytics. (2023). Global Multiple Sclerosis Market Analysis Report.

[2] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA Website]

[3] European Medicines Agency. (n.d.). Biosimilar medicines. Retrieved from [EMA Website]

[4] Market Research Report. (2023). Glatiramer Acetate Market: Trends, Opportunities, and Competitive Analysis.

More… ↓