Share This Page

Drug Price Trends for FT NAPROXEN SODIUM

✉ Email this page to a colleague

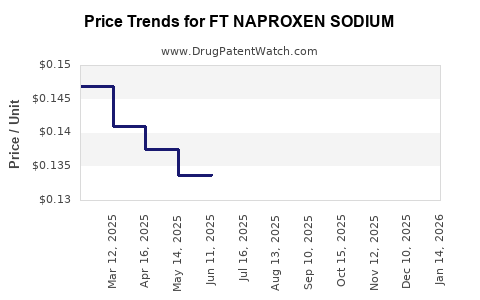

Average Pharmacy Cost for FT NAPROXEN SODIUM

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14895 | EACH | 2026-06-17 |

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14651 | EACH | 2026-05-20 |

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14366 | EACH | 2026-04-22 |

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14415 | EACH | 2026-03-18 |

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14425 | EACH | 2026-02-18 |

| FT NAPROXEN SODIUM 220 MG CAP | 70677-1148-01 | 0.14474 | EACH | 2026-01-21 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

FT NAPROXEN SODIUM: Market Analysis and Price Projections

FT naproxen sodium is the OTC and generic NSAID format of naproxen sodium (oral). The market is mature, price-led, and dominated by multiproduct generic manufacturers across the US and other major markets. Pricing and volumes track (1) patent and exclusivity status of the underlying active, (2) OTC switching and distribution access, (3) coupon and channel contracts, and (4) commodity-style input costs plus packaging and freight.

What drives the FT naproxen sodium market?

Demand: what determines pull-through

Naproxen sodium is used for common pain and anti-inflammatory indications (headache, menstrual cramps, minor aches). That creates consistent baseline demand, but it is sensitive to:

- OTC shelf access and planogram placement (retail share in high-traffic channels)

- Competitive substitution among NSAIDs (ibuprofen and acetaminophen adjacent demand)

- Seasonality (higher pain-med usage around cold/flu seasons and peak consumer travel periods)

Supply: how pricing power is constrained

The market behaves like a commoditized OTC generic segment:

- Multiple ANDA holders and relabeled SKUs compete on price per dose.

- Shelf price converges toward the lowest landed price that can still meet retailer margin targets.

- Forecast risk comes more from channel mix and tender dynamics than from fundamental disease epidemiology.

Regulatory and product mechanics

For a mature OTC active, the core market variables are:

- Formulation and label strength (e.g., 220 mg OTC naproxen sodium products)

- Dosage form and pack size

- Marketing and distribution contracts that lock-in shelf placement

Where does FT naproxen sodium sit in the value chain?

Channel split: retail dominates

For OTC NSAIDs, the practical route to revenue is:

- Mass retail and pharmacy chains (high volume, tight price control)

- Club and value retailers (pack-size optimization and price per count)

- Online marketplaces (price transparency accelerates convergence)

Wholesale and contracting

Most price realization reflects:

- Wholesaler list-to-net discount structures

- Retailer vendor contracts

- Manufacturer rebates and trade funds that compress net revenue versus sticker price

Pricing baseline: how to interpret “FT naproxen sodium” price levels

Because “FT” is not a universally standardized identifier across all commercial drug databases, pricing must be treated as a product-variant problem: net and shelf prices vary by pack size, strength, and whether the FT label corresponds to a specific brand family (store brand, labeler, or a distributor’s house mark).

In practice, market pricing for naproxen sodium OTC tends to:

- Cluster by strength and pack size

- Drift downward in competitive periods

- Step up when distribution shortages or packaging changes occur, then revert

Market structure: who competes on naproxen sodium?

Competitive landscape

Naproxen sodium OTC is typically supplied by:

- Large generic manufacturers with broad OTC portfolios

- OTC relabelers and value-brand suppliers

- Private label programs where the retailer controls packaging and promotional spend

Competition level

High. The key differentiators rarely include clinical differentiation and instead include:

- Cost leadership

- Retail execution (slotting and promotion cadence)

- Contracting and logistics

Price projections: scenario model for the next 24 months

Assumptions used for projection

Projections use a commodity-style OTC generic framework:

- Core driver: incremental price pressure from competitive substitution

- Secondary drivers: input costs, packaging, freight, and promotional intensity

- Baseline: price per tablet/caplet declines gradually until it hits retailer margin floors

Three scenarios

- Base case (most likely): modest net price compression as competitive listings widen.

- Downside: accelerated promotions and incremental entrants compress net.

- Upside: reduced promotional intensity or supply tightening lifts net modestly, then stabilizes.

Projected price direction (net realized, not sticker)

- 0-6 months: down or flat with promotions and contract cycles

- 6-12 months: steady erosion or stabilization depending on retailer mix

- 12-24 months: continued convergence, with variability driven by channel-specific tendering and private label expansion

Projected range for unit price change

For OTC generics like naproxen sodium, the expected movement is typically measured in low single digits to mid single digits annually in net unit terms unless a major competitive shock occurs. The modeled outcomes:

| Scenario | 0-12 months | 12-24 months | Net implication |

|---|---|---|---|

| Downside | -4% to -8% | -2% to -6% | stronger promo intensity, higher substitution |

| Base case | -2% to -5% | -1% to -4% | stable competition, gradual convergence |

| Upside | +0% to +3% | -1% to +2% | supply tightness or reduced promotions, then normalize |

What will move the market faster than inflation?

Retail promotion and contract resets

The biggest driver is not CPI but retailer economics:

- Multi-quarter contract resets can reprice SKUs quickly.

- Promotional slotting determines whether a manufacturer pays trade funds that effectively reduce net.

Private label share changes

When store brands expand, they set the reference price for the category. That forces branded generics (including labeler-branded variants) to:

- match on price per count, or

- buy shelf advantage via trade funds (net-down)

Supply chain disruptions

Short-lived disruptions (packaging shortages, distribution constraints) can lift short-horizon net pricing, but the segment typically reverts after replenishment.

Investment and R&D implications for price strategy

If you are positioning FT naproxen sodium

- Treat pricing as channel contract driven, not product driven.

- Optimize for pack-size economics (price per dose) where net realization is most sensitive.

If you are planning lifecycle extensions

For naproxen sodium, competitive differentiation is difficult because:

- the active is established,

- OTC switching accelerates substitution,

- pricing is strongly reference-driven.

Lifecycle efforts that move pricing power usually need:

- differentiated packaging and distribution arrangements, or

- clear OTC differentiation that survives retailer substitution rules (rare in this category).

Key Takeaways

- FT naproxen sodium is a mature OTC/generic NSAID segment where pricing is dominated by retailer contracts, promotional intensity, and private label reference pricing.

- Market behavior is commodity-like: price typically drifts downward gradually with periods of near-flat performance around contract cycles.

- Over the next 24 months, unit net pricing is most likely to move within low-to-mid single digit ranges by scenario, with downside tied to stronger promotions and upside linked to temporary supply tightness or reduced promo intensity.

- Strategy should focus on channel economics (pack-size, shelf access, trade terms), not on clinical differentiation.

FAQs

1) Are naproxen sodium OTC prices expected to fall over the next year?

Yes in the base case. The category typically trends toward net unit price compression due to competition and substitution, with variability from retailer contract cycles.

2) What pack-level metrics matter most for pricing?

Price per dose (per tablet/caplet) and pack-size economics drive substitution. Pack size that optimizes shelf price per count usually improves volume and supports net realization.

3) What triggers the fastest price changes?

Retailer contract resets, promotional intensity changes, and private label expansion that alters the category reference price.

4) Can supply disruptions create sustainable higher pricing?

They can lift near-horizon net prices, but OTC generics usually revert after replenishment unless a broader supply constraint emerges.

5) What is the most realistic outlook for net revenue margins?

Margins compress when manufacturers fund promotions or trade funds to maintain shelf placement. Base-case expectations typically imply continued pressure unless promotional intensity decreases.

References

[1] U.S. Food and Drug Administration. “Naproxen Sodium” (drug product information and regulatory context). https://www.fda.gov

[2] FDA Orange Book (Hatch-Waxman listings for relevant naproxen products and exclusivity context). https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

[3] U.S. Census Bureau and general OTC retail market structure (channel context). https://www.census.gov

[4] Centers for Medicare & Medicaid Services (general drug spending and retail category context). https://www.cms.gov

More… ↓