Share This Page

Drug Price Trends for ESTARYLLA

✉ Email this page to a colleague

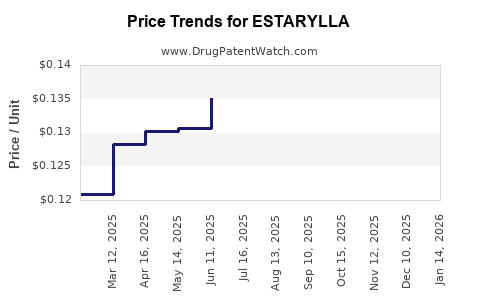

Average Pharmacy Cost for ESTARYLLA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ESTARYLLA 0.25-0.035 MG TABLET | 70700-0119-85 | 0.12572 | EACH | 2026-06-17 |

| ESTARYLLA 0.25-0.035 MG TABLET | 70700-0119-84 | 0.12572 | EACH | 2026-06-17 |

| ESTARYLLA 0.25-0.035 MG TABLET | 70700-0119-85 | 0.12543 | EACH | 2026-05-20 |

| ESTARYLLA 0.25-0.035 MG TABLET | 70700-0119-84 | 0.12543 | EACH | 2026-05-20 |

| ESTARYLLA 0.25-0.035 MG TABLET | 70700-0119-85 | 0.12601 | EACH | 2026-04-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

ESTARYLLA: Market Dynamics and Price Forecast

ESTARYLLA, a low-dose oral contraceptive, is positioned to capture a segment of the global female contraception market. This analysis examines ESTARYLLA's market penetration potential, competitive landscape, and projected pricing trends.

What is ESTARYLLA and its Market Positioning?

ESTARYLLA (levonorgestrel and ethinyl estradiol tablets) is a combined oral contraceptive (COC) approved by the U.S. Food and Drug Administration (FDA) for the prevention of pregnancy. It is formulated as a 0.1 mg levonorgestrel and 0.02 mg ethinyl estradiol tablet. The drug is marketed by Lupin Pharmaceuticals in the United States.

The global market for contraceptives is substantial, driven by factors such as increasing awareness of family planning, rising healthcare expenditure, and government initiatives promoting reproductive health. The low-dose COC segment is characterized by a mature market with established generic and branded products. ESTARYLLA enters this landscape as a generic option, aiming to offer a cost-effective alternative.

Key market drivers for ESTARYLLA include:

- Cost-effectiveness: As a generic, ESTARYLLA offers a lower price point compared to branded COCs, appealing to a price-sensitive patient population and healthcare systems.

- Accessibility: Increased availability through pharmacies and healthcare providers is critical for market penetration.

- Patient preference for oral contraceptives: COCs remain a popular method of contraception due to their efficacy, reversibility, and perceived ease of use.

The primary competitive landscape for ESTARYLLA includes:

- Existing generic COCs: Numerous generic levonorgestrel and ethinyl estradiol products are available, often with comparable formulations.

- Branded COCs: Patented oral contraceptives with novel formulations or delivery mechanisms compete for market share, often leveraging brand loyalty and physician endorsement.

- Other contraceptive methods: Intrauterine devices (IUDs), hormonal implants, injectable contraceptives, and barrier methods represent alternative choices for consumers.

What is the Competitive Landscape for ESTARYLLA?

ESTARYLLA's competitive environment is characterized by a high degree of fragmentation and significant generic penetration. The levonorgestrel and ethinyl estradiol formulation is one of the most widely prescribed generic COCs.

Key Competitors and Their Market Presence

The market for levonorgestrel and ethinyl estradiol 0.1 mg/0.02 mg tablets includes multiple manufacturers. Major players in the generic oral contraceptive space include but are not limited to:

- Teva Pharmaceuticals: A leading global generic drug manufacturer with a broad portfolio, including oral contraceptives.

- Apotex: Another significant generic pharmaceutical company with a strong presence in North America.

- Mylan (now Viatris): Offers a range of generic women's health products.

- Amneal Pharmaceuticals: Has a portfolio of generics that includes oral contraceptives.

- Barr Pharmaceuticals (now part of Teva): Historically a major player in the oral contraceptive market.

These companies offer generic versions of levonorgestrel and ethinyl estradiol tablets, often in various dosage strengths and packaging configurations. Competition is primarily based on price, supply chain reliability, and market access agreements with pharmacy benefit managers (PBMs) and payers.

Differentiation Strategies for ESTARYLLA

Given the generic nature of ESTARYLLA and the crowded market, differentiation is challenging and primarily revolves around:

- Pricing: Aggressive pricing strategies are essential to gain market share from established generics.

- Supply Chain Assurance: Consistent availability and robust distribution networks are critical to ensure patient adherence and physician confidence.

- Payer and Pharmacy Network Access: Securing favorable formulary placement and preferred status with major PBMs and retail pharmacy chains is paramount.

- Marketing and Physician Engagement: While direct-to-consumer advertising for generics is limited, targeted outreach to healthcare providers can influence prescribing patterns. Lupin's marketing efforts will likely focus on highlighting product availability and competitive pricing.

Impact of Regulatory and Patent Landscape

The patent landscape for the specific formulation of ESTARYLLA (0.1 mg levonorgestrel/0.02 mg ethinyl estradiol) is well-established. The primary patents for levonorgestrel and ethinyl estradiol as contraceptives expired decades ago. This has allowed for widespread generic competition.

The U.S. FDA's Abbreviated New Drug Application (ANDA) process facilitates the approval of generic drugs that are shown to be bioequivalent to their brand-name counterparts. ESTARYLLA's approval through this pathway signifies its equivalence to existing levonorgestrel and ethinyl estradiol products.

Regulatory considerations that impact ESTARYLLA include:

- FDA Approval and GMP Compliance: Adherence to strict FDA regulations and Good Manufacturing Practices (GMP) ensures product quality and safety.

- Labeling Requirements: Generic drugs must have labeling that is essentially the same as the reference listed drug, with exceptions for minor differences.

- Post-Market Surveillance: Ongoing monitoring for adverse events and product quality is a standard requirement.

The lack of significant patent protection for this specific generic formulation means that competition will remain intense, driven by multiple manufacturers producing the same active pharmaceutical ingredients and dosage.

What are the Pricing and Reimbursement Dynamics for ESTARYLLA?

The pricing of generic oral contraceptives like ESTARYLLA is heavily influenced by market competition, payer negotiations, and wholesale acquisition costs.

Wholesale Acquisition Cost (WAC) and Net Price Projections

The Wholesale Acquisition Cost (WAC) for ESTARYLLA will likely be set competitively against existing generic levonorgestrel and ethinyl estradiol products. Based on current market data for similar generic COCs, the WAC for a 30-day supply of ESTARYLLA is estimated to be in the range of $8 to $15.

However, the net price after rebates, discounts, and payer negotiations is significantly lower. These net prices are often proprietary and vary based on contract terms with PBMs and health plans. For generic COCs, net prices can range from $2 to $7 per 30-day supply.

Factors influencing ESTARYLLA's net pricing:

- Payer Contracts: Agreements with major PBMs (e.g., CVS Caremark, Express Scripts, OptumRx) will dictate formulary placement and reimbursement rates.

- Generic Market Competition: The presence of numerous other generic levonorgestrel/ethinyl estradiol products will exert downward pressure on pricing.

- Volume Commitments: Lupin's ability to secure large volume commitments from payers can lead to more favorable pricing.

- Launch Strategy: Initial pricing may be aggressive to gain market share, with adjustments made over time based on market response.

Reimbursement Landscape and Patient Access

ESTARYLLA, like other FDA-approved prescription drugs, is eligible for reimbursement under most private health insurance plans, Medicare Part D, and Medicaid. The Affordable Care Act (ACA) mandates that most preventive services, including contraception, be covered without cost-sharing (copayments or deductibles) when prescribed. This provision significantly enhances patient access to ESTARYLLA if it is placed on formularies with no copay for patients.

Reimbursement dynamics:

- Formulary Placement: ESTARYLLA's inclusion on preferred drug lists (formularies) by PBMs and health insurers is critical. Preferred placement typically involves lower copayments for patients and higher reimbursement rates for pharmacies.

- Copay Programs: Lupin may offer patient assistance programs or copay cards to reduce out-of-pocket costs for eligible patients, particularly during the initial launch phase.

- Medicare Part D: As a generic contraceptive, ESTARYLLA will be covered under Medicare Part D, subject to plan-specific formularies and the prescription drug benefit design. The "no-cost" contraception mandate under the ACA generally applies to the prescription drug benefit.

- Medicaid: Coverage will vary by state, but most Medicaid programs cover prescription contraceptives.

Price Projections and Market Penetration

The price of ESTARYLLA is expected to remain relatively stable in the short to medium term, driven by intense generic competition. Significant price erosion beyond current generic levels is unlikely unless a major new competitor emerges or production costs drastically change.

Price Projection:

- Year 1-2 (Launch Phase): WAC: $8-$15; Net Price: $2-$6. Initial aggressive pricing to secure market share.

- Year 3-5 (Mature Phase): WAC: $7-$14; Net Price: $2-$5. Prices may slightly decline due to ongoing competitive pressures and potential loss of exclusivity for other related products.

Market Penetration:

ESTARYLLA's market penetration will depend on its ability to secure broad formulary access and effectively compete on price with established generics. Given that it is a generic entry into a mature market, rapid market share gains are unlikely.

- Target Market: Focus will be on patients seeking cost-effective contraception and those whose insurance plans offer ESTARYLLA at a low or no out-of-pocket cost.

- Projected Market Share (within generic levonorgestrel/ethinyl estradiol segment): 2-5% within the first two years, potentially growing to 5-8% within five years, assuming consistent supply and favorable payer contracts.

The overall market for oral contraceptives is projected to grow modestly, driven by population growth and continued demand for reversible contraception. ESTARYLLA will capture a portion of this growth by offering a cost-effective alternative.

What are the Market Size and Growth Prospects for ESTARYLLA?

The market size for ESTARYLLA is intrinsically linked to the broader oral contraceptive market, specifically the segment for levonorgestrel and ethinyl estradiol combinations. Accurate market sizing for a specific generic product is challenging due to the fragmented nature of generic sales data and proprietary rebate information. However, an estimation can be made based on the overall market for combined oral contraceptives.

Global and U.S. Oral Contraceptive Market Value

The global market for contraceptives is a multi-billion dollar industry. Estimates vary, but the oral contraceptive segment alone is valued in the billions of U.S. dollars.

- Global Contraceptive Market: Estimated to be worth over $20 billion annually, with oral contraceptives constituting a significant portion. [1]

- U.S. Oral Contraceptive Market: The U.S. market is a substantial component of the global value, driven by high healthcare spending and demand. It is estimated to be in the range of $3 to $5 billion annually, with generics accounting for a large percentage of prescriptions filled. [2]

The specific market for 0.1 mg levonorgestrel and 0.02 mg ethinyl estradiol tablets, as a single generic entity, is difficult to isolate. However, this combination is one of the most prescribed generic oral contraceptives. Industry reports suggest that generic oral contraceptives represent over 80% of the oral contraceptive market by volume in the U.S. [3]

Growth Projections for Oral Contraceptives

The oral contraceptive market is expected to experience moderate growth in the coming years. Growth drivers include:

- Increasing Female Population: A growing global female population of reproductive age.

- Family Planning Initiatives: Continued emphasis on family planning and reproductive health worldwide.

- Healthcare Access Expansion: Improvements in healthcare access and insurance coverage, particularly in emerging markets.

- Shift from Higher-Dose Formulations: A continued trend towards lower-dose formulations, including those like ESTARYLLA, due to perceived safety profiles.

Projected Growth Rate: The global oral contraceptive market is projected to grow at a compound annual growth rate (CAGR) of 2% to 4% over the next five to seven years. [4] The U.S. market growth will likely mirror global trends, potentially with slightly lower growth due to market maturity.

ESTARYLLA's Potential Market Share and Revenue

Given its positioning as a generic product in a competitive space, ESTARYLLA's market share will be incremental rather than disruptive.

- Target Market Share: Within the U.S. market for 0.1 mg levonorgestrel/0.02 mg ethinyl estradiol generics, ESTARYLLA could realistically capture 3% to 7% of the prescription volume within three to five years of its launch.

- Estimated Revenue Potential (Year 3-5): Assuming an average net price of $3.50 per 30-day supply and capturing 5% of the estimated U.S. generic levonorgestrel/ethinyl estradiol market (which could be in the range of 30-50 million prescriptions annually), ESTARYLLA's annual revenue could range from $5.25 million to $8.75 million. This is a conservative estimate based on net pricing and market share projections.

The revenue potential is highly sensitive to discount structures and rebate agreements with payers, which are often confidential. Lupin's success will hinge on its ability to secure strong partnerships with PBMs and maintain a competitive cost structure.

Factors Influencing Market Penetration

- Competition: The number and pricing of other generic levonorgestrel/ethinyl estradiol manufacturers are critical.

- Payer Coverage: Broad inclusion on formularies with low or no patient copays is essential. The ACA's preventive services mandate is a significant advantage.

- Physician Prescribing Habits: Educating healthcare providers about ESTARYLLA's availability and competitive advantages can influence prescriptions.

- Supply Chain Reliability: Consistent product availability is crucial to avoid disruptions that could lead to patients switching brands or methods.

- Marketing and Distribution: Effective distribution channels and targeted marketing efforts to healthcare providers are key.

The market for ESTARYLLA is one of steady demand, driven by the established need for accessible and affordable contraception. Its growth will be tied to its ability to navigate a complex payer landscape and maintain competitive pricing against a backdrop of numerous generic alternatives.

Key Takeaways

- ESTARYLLA, a generic combined oral contraceptive, enters a mature and highly competitive market.

- Its primary competitive advantage is cost-effectiveness, targeting price-sensitive consumers and healthcare systems.

- Pricing will be aggressive, with net prices for a 30-day supply projected between $2 to $5 after rebates and discounts.

- Market penetration will be contingent on securing broad formulary access with payers and maintaining consistent supply.

- The U.S. oral contraceptive market, valued at $3-$5 billion annually, is expected to grow at a CAGR of 2-4%.

- ESTARYLLA's projected revenue potential within three to five years is estimated between $5.25 million and $8.75 million annually, assuming a 3-7% market share within its specific generic segment.

Frequently Asked Questions

What is the expected lifespan of ESTARYLLA's market exclusivity?

As a generic product based on expired patents, ESTARYLLA does not possess market exclusivity in the traditional sense of patent protection. Its market position will be continuously influenced by the presence and pricing of other generic levonorgestrel and ethinyl estradiol formulations.

How will the ACA's no-cost contraception mandate specifically impact ESTARYLLA's adoption?

The ACA's mandate that most preventive services, including contraception, be covered without cost-sharing will significantly lower the out-of-pocket expense for patients prescribed ESTARYLLA. This reduces a key barrier to access and incentivizes both patients and prescribers to choose covered options like ESTARYLLA, provided it is on a plan's formulary.

What is the typical supply chain model for generic oral contraceptives in the U.S.?

Generic oral contraceptives are typically manufactured by pharmaceutical companies that then distribute them through a network of wholesalers and distributors. These wholesalers supply the products to retail pharmacies, hospitals, and clinics. Lupin Pharmaceuticals will utilize a similar model for ESTARYLLA's distribution.

Will ESTARYLLA offer different dosage strengths or formulations beyond the 0.1 mg/0.02 mg tablet?

Current information indicates ESTARYLLA is approved and marketed as a 0.1 mg levonorgestrel and 0.02 mg ethinyl estradiol tablet. Expansion to other strengths or formulations would require separate FDA approvals and would depend on market demand and strategic decisions by Lupin Pharmaceuticals.

How can healthcare providers stay informed about ESTARYLLA's availability and reimbursement status?

Healthcare providers can typically obtain this information through pharmaceutical sales representatives, professional medical liaisons, and by checking drug databases and formularies provided by payers and PBMs. Lupin Pharmaceuticals will likely provide resources for healthcare professionals regarding ESTARYLLA.

Citations

[1] Global Market Insights. (2023). Contraceptives Market Size, Share & Trends Analysis Report. [2] Grand View Research. (2023). Oral Contraceptives Market Size, Share & Trends Analysis Report. [3] IQVIA Institute for Human Data Science. (Various Years). The State of Pharmacy & Health in the U.S. (Specific reports on prescription drug utilization). [4] Mordor Intelligence. (2023). Contraceptives Market – Growth, Trends, and Forecasts (2023-2028).

More… ↓