Share This Page

Drug Price Trends for EPINASTINE HCL

✉ Email this page to a colleague

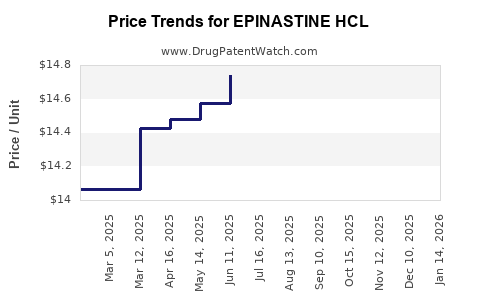

Average Pharmacy Cost for EPINASTINE HCL

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| EPINASTINE HCL 0.05% EYE DROPS | 70069-0008-01 | 14.85313 | ML | 2026-05-20 |

| EPINASTINE HCL 0.05% EYE DROPS | 60505-0584-01 | 14.85313 | ML | 2026-05-20 |

| EPINASTINE HCL 0.05% EYE DROPS | 70069-0008-01 | 14.46243 | ML | 2026-04-22 |

| EPINASTINE HCL 0.05% EYE DROPS | 60505-0584-01 | 14.46243 | ML | 2026-04-22 |

| EPINASTINE HCL 0.05% EYE DROPS | 70069-0008-01 | 13.79143 | ML | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for EPINASTINE HCL

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| EPINASTINE HCL 0.05% SOLN,OPH | Golden State Medical Supply, Inc. | 51991-0836-75 | 5ML | 68.62 | 13.72400 | ML | 2023-06-15 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Epinastine HCl: Patent Landscape and Market Projections

Epinastine HCl, an H1 antihistamine and mast cell stabilizer, is utilized for the symptomatic treatment of allergic conjunctivitis. Its market performance is influenced by patent expiry, generic competition, and the prevalence of allergic eye conditions.

What is Epinastine HCl and Its Therapeutic Use?

Epinastine hydrochloride is a second-generation H1 antihistamine. It acts by blocking the action of histamine, a chemical released during allergic reactions, thereby reducing symptoms like itching and redness. Unlike first-generation antihistamines, epinastine is less likely to cause drowsiness. Its dual mechanism of action, including mast cell stabilization, offers a comprehensive approach to managing allergic conjunctivitis. This condition is characterized by inflammation of the conjunctiva, the membrane lining the eyelid and covering the white part of the eye, triggered by allergens such as pollen, dust mites, or pet dander.

What is the Current Patent Landscape for Epinastine HCl?

The patent landscape for epinastine HCl is characterized by foundational composition of matter patents that have long expired, alongside later patents related to specific formulations, methods of use, and manufacturing processes.

Key Patent Expiries:

- Original Composition of Matter Patents: These patents, typically covering the active pharmaceutical ingredient itself, are no longer in force. The primary patent for epinastine was filed in the late 1970s and early 1980s. For example, United States Patent US4280957 A, covering epinastine and related compounds, was filed in 1979 and granted in 1981, expiring well before current market considerations.

- Formulation and Delivery Patents: Patents related to specific ophthalmic solutions, sustained-release formulations, or combination therapies involving epinastine have provided market exclusivity for extended periods. These patents are crucial for extended brand protection. For instance, patents covering specific buffering agents, preservatives, or viscosity modifiers in ophthalmic solutions can extend protection.

- Method of Use Patents: Patents claiming specific uses of epinastine for treating particular types of allergic conjunctivitis or in combination with other treatments could still be relevant, though their enforcement is often more complex and dependent on demonstrating novel therapeutic benefits.

- Manufacturing Process Patents: Improvements in synthetic routes or purification methods can be patented, offering a degree of protection against generic manufacturers by requiring them to develop non-infringing processes.

The expiration of key patents has opened the door for generic competition, significantly impacting pricing and market share dynamics. Companies relying on epinastine HCl for their branded products must navigate the landscape of remaining secondary patents, which may offer limited protection periods or be subject to litigation.

Who are the Key Market Players and Competitors?

The market for epinastine HCl is populated by both originator companies and generic manufacturers.

Originator Companies:

- Santen Pharmaceutical Co., Ltd.: Santen is a significant player with its branded ophthalmic solution, Allelock® (epinastine HCl 0.05%), which has historically been a dominant product in markets like Japan and some European countries.

- Alcon (Novartis subsidiary): While not directly marketing a branded epinastine product as prominently as Santen, Alcon has been involved in the ophthalmic space and may hold relevant intellectual property or distribution agreements.

Generic Manufacturers:

The generic market is fragmented and competitive. Key players often include:

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Mylan N.V. (now part of Viatris)

- Apotex Inc.

- IOL Chemicals and Pharmaceuticals Ltd.

These companies focus on developing bioequivalent generic versions of epinastine HCl ophthalmic solutions once primary patents have lapsed. Their competitive strategy centers on achieving regulatory approval and capturing market share through lower pricing.

Competitive Landscape Analysis:

The market is characterized by a shift from brand-name dominance to generic price erosion following patent expirations. This dynamic intensifies competition, requiring companies to focus on efficient manufacturing and distribution. The availability of multiple generic options for epinastine HCl ophthalmic solutions directly impacts the pricing strategies of both originator and generic brands.

What are the Market Size and Growth Projections for Epinastine HCl?

The global market size for epinastine HCl is moderate, primarily driven by its specific indication for allergic conjunctivitis. Projections indicate a modest growth rate, influenced by the increasing prevalence of allergic diseases and the accessibility of generic alternatives.

Market Size (Estimated):

The global ophthalmic antihistamine market, which includes epinastine HCl, is valued in the hundreds of millions of U.S. dollars. The specific segment for epinastine HCl is a fraction of this, estimated to be in the range of USD 50 million to USD 150 million annually, depending on the geographic scope and inclusion of all its formulations. This figure is subject to significant variability due to differing market access and prescription patterns across regions.

Growth Drivers:

- Rising Incidence of Allergic Conjunctivitis: An increase in environmental allergens and the growing awareness of allergic diseases contribute to higher diagnoses of allergic conjunctivitis.

- Demand for Ophthalmic Antihistamines: Patients and healthcare providers increasingly opt for targeted ophthalmic treatments over systemic antihistamines due to faster symptom relief and fewer systemic side effects.

- Generic Accessibility: The availability of cost-effective generic epinastine HCl solutions expands access, particularly in emerging markets, thus increasing overall volume.

Growth Restraints:

- Intense Generic Competition: The presence of numerous generic manufacturers leads to significant price erosion, limiting revenue growth for the overall market.

- Development of Newer Therapies: Research and development in ophthalmology may yield newer, potentially more effective or convenient treatments for allergic conjunctivitis, diverting market share.

- Limited Indication Breadth: Epinastine HCl is primarily indicated for allergic conjunctivitis, lacking broader applications that could drive more substantial market expansion.

Market Projections (Next 5 Years):

The market for epinastine HCl is projected to grow at a Compound Annual Growth Rate (CAGR) of 2% to 4% over the next five years. This slow but steady growth is primarily driven by increased prevalence of allergic conjunctivitis and wider adoption of generics, counterbalanced by intense price competition.

Geographic Considerations:

- North America and Europe: These regions represent mature markets with established generic penetration. Growth will be driven by prevalence increases rather than significant new market entries.

- Asia-Pacific: This region is expected to see higher growth rates due to increasing healthcare access, rising disposable incomes, and a growing awareness of allergic conditions. Generic penetration is also expanding rapidly.

What are the Pricing and Reimbursement Trends for Epinastine HCl?

Pricing for epinastine HCl ophthalmic solutions is bifurcated, with significant differences between branded and generic products. Reimbursement policies vary by region and payer.

Pricing Dynamics:

- Branded Products (e.g., Allelock®): Original branded formulations command a premium price, reflecting R&D investment and brand recognition. Prices can range from USD 20 to USD 50 per bottle (typically 5 mL of 0.05% solution), depending on the market and specific product.

- Generic Products: Following patent expiry, generic epinastine HCl solutions are priced substantially lower. A typical 5 mL bottle of a generic formulation might range from USD 5 to USD 15. Price variations among generic manufacturers are driven by manufacturing costs, distribution agreements, and market competition.

- Price Erosion: The introduction of multiple generic competitors has historically led to a rapid decline in pricing for both branded and generic products. This erosion is a significant factor in the overall market revenue projections.

Reimbursement Trends:

- Prescription vs. Over-the-Counter (OTC): In many markets, epinastine HCl ophthalmic solutions are available as prescription drugs. However, in some regions, particularly with lower concentrations or specific formulations, they may be accessible as OTC products.

- Insurance Coverage: In countries with robust healthcare systems (e.g., U.S., UK, Germany), epinastine HCl is generally covered by private insurance and public health programs when prescribed for allergic conjunctivitis. Coverage levels and co-pays vary.

- Formulary Placement: Pharmaceutical benefit managers (PBMs) and hospital formularies often prioritize generic alternatives due to cost-effectiveness, leading to epinastine HCl generics being favored over branded options.

- Direct-to-Consumer Advertising (DTCA): In markets like the U.S., DTCA for branded allergy eye drops can influence patient demand, though it is often counteracted by payer efforts to steer towards generics.

- Government Tenders and Bulk Purchasing: In public healthcare systems and certain emerging markets, government tenders and bulk purchasing agreements can significantly influence the pricing and availability of epinastine HCl, often securing very competitive prices.

Future Pricing Outlook:

The downward pressure on pricing is expected to continue, especially in highly competitive generic markets. Innovation in formulation (e.g., preservative-free options, enhanced delivery systems) may create opportunities for higher-priced, differentiated products, but the core generic market will remain price-sensitive.

What are the Regulatory Considerations for Epinastine HCl?

Regulatory pathways for epinastine HCl, particularly for ophthalmic solutions, involve stringent requirements from health authorities worldwide.

Key Regulatory Agencies and Guidelines:

- U.S. Food and Drug Administration (FDA): For a new drug application (NDA) for an original formulation or a supplemental NDA (sNDA) for new indications or formulations. For generic versions, Abbreviated New Drug Applications (ANDAs) are required, demonstrating bioequivalence to a reference listed drug (RLD).

- European Medicines Agency (EMA): Through national competent authorities, the EMA oversees marketing authorization applications (MAA) for branded products and national procedures for generics.

- Pharmaceuticals and Medical Devices Agency (PMDA) in Japan: Approves drugs for the Japanese market.

- Other National Regulatory Bodies: Health Canada, Therapeutic Goods Administration (TGA) in Australia, and others have their own specific requirements.

Key Regulatory Requirements:

- Chemistry, Manufacturing, and Controls (CMC): Comprehensive data on drug substance and drug product manufacturing, purity, stability, and quality control. This includes detailed specifications for active pharmaceutical ingredient (API) and finished dosage forms.

- Non-clinical Studies: Toxicology and pharmacology data.

- Clinical Trials: For original applications, robust Phase I, II, and III trials are necessary to demonstrate safety and efficacy. For generics, bioequivalence studies comparing the generic to the RLD are paramount.

- Labeling and Packaging: Compliance with local regulations regarding prescription information, warnings, dosage instructions, and packaging integrity.

- Good Manufacturing Practices (GMP): All manufacturing facilities must adhere to GMP standards.

- Post-Marketing Surveillance: Pharmacovigilance systems to monitor adverse events and ensure ongoing safety.

Challenges and Opportunities:

- Generic Approval Timelines: The time taken for ANDA or MAA approval can vary significantly, impacting market entry for generic manufacturers.

- Patent Litigation: Challenges to existing patents or defense against infringement claims can be a significant regulatory and legal hurdle.

- Excipient Compliance: For ophthalmic solutions, excipients (e.g., preservatives like benzalkonium chloride) are subject to scrutiny for safety and potential toxicity. The move towards preservative-free formulations is a growing trend driven by regulatory and patient preference.

- Quality Standards: Maintaining high quality across multiple manufacturing sites and supply chains is crucial, especially as global supply chains become more complex.

Specific Considerations for Epinastine HCl Ophthalmic Solutions:

- Sterility: Ophthalmic products require strict sterility assurance.

- pH and Osmolarity: The formulation must be compatible with the ocular surface to avoid irritation.

- Preservative Efficacy: If preservatives are used, their efficacy must be demonstrated against microbial contamination according to pharmacopeial standards (e.g., USP, Ph. Eur.).

The regulatory environment for pharmaceuticals is dynamic, with evolving guidelines on data requirements and quality standards. Companies must stay abreast of these changes to ensure successful product development and market access.

What are the Future Outlook and Potential Opportunities for Epinastine HCl?

The future of epinastine HCl in the pharmaceutical market is characterized by a stable, albeit competitive, demand for its established indication, with opportunities for product differentiation and market expansion in specific regions.

Market Stability:

Epinastine HCl is a well-established treatment for allergic conjunctivitis. Its efficacy, safety profile, and accessibility through generic formulations ensure continued demand. The increasing prevalence of allergic diseases globally provides a foundational market.

Opportunities for Product Differentiation:

- Preservative-Free Formulations: The trend towards preservative-free ophthalmic products continues, driven by concerns over ocular surface toxicity. Manufacturers who can successfully develop and market preservative-free epinastine HCl solutions may capture a premium segment and appeal to patients with sensitive eyes or those using the drops frequently.

- Combination Therapies: While not currently a significant area for epinastine HCl, research into combining it with other active ingredients (e.g., lubricants, anti-inflammatories) for enhanced symptom relief or broader therapeutic coverage could present future opportunities, provided such combinations offer demonstrable synergistic benefits and clear regulatory pathways.

- Enhanced Delivery Systems: Innovations in drug delivery could lead to formulations offering longer duration of action, reducing the need for frequent dosing and improving patient compliance. This could include microparticle suspensions or other advanced ophthalmic delivery technologies.

Geographic Expansion and Market Penetration:

- Emerging Markets: Significant growth potential exists in emerging economies across Asia, Latin America, and Africa. As healthcare infrastructure improves and disposable incomes rise, demand for effective allergy treatments like epinastine HCl is expected to increase. Generic manufacturers are well-positioned to penetrate these markets with affordable options.

- Increased Awareness and Diagnosis: Public health campaigns and improved diagnostic capabilities for allergic conjunctivitis in developing regions can further drive market penetration.

Strategic Considerations for Companies:

- Generic Manufacturers: Focus on cost-efficient manufacturing, robust supply chains, and securing favorable formulary placement. Exploring niche markets and developing preservative-free options can offer competitive advantages.

- Originator Companies: Leverage remaining secondary patents for niche formulations or differentiated products. Consider licensing or strategic partnerships to expand geographic reach or explore new therapeutic applications.

- R&D Investment: While the core indication is mature, investment in formulation science and delivery systems could yield valuable intellectual property and market differentiation.

The long-term outlook for epinastine HCl hinges on its ability to maintain cost-effectiveness and adapt to evolving patient and healthcare provider preferences for ocular treatments.

Key Takeaways

- Epinastine HCl's market is defined by expired composition of matter patents, leading to substantial generic competition.

- The market size is estimated between USD 50 million to USD 150 million annually, with a projected CAGR of 2% to 4%.

- Pricing is significantly lower for generic versions, ranging from USD 5 to USD 15 per bottle, compared to branded products.

- Regulatory approval requires demonstrating bioequivalence for generics and robust safety and efficacy for new formulations.

- Future opportunities lie in preservative-free formulations, enhanced delivery systems, and expansion into emerging markets.

FAQs

-

What is the primary therapeutic indication for Epinastine HCl? Epinastine HCl is primarily used for the symptomatic treatment of allergic conjunctivitis.

-

Which companies are major players in the Epinastine HCl market? Key originator players include Santen Pharmaceutical. The generic market involves numerous manufacturers such as Sun Pharmaceutical, Teva, and Dr. Reddy's Laboratories.

-

How has patent expiry affected the price of Epinastine HCl? Patent expiry has led to significant price erosion, with generic versions of Epinastine HCl ophthalmic solutions being substantially cheaper than branded formulations.

-

What are the main growth drivers for the Epinastine HCl market? Growth is driven by the increasing incidence of allergic conjunctivitis and the wider accessibility of affordable generic options.

-

Are there any upcoming innovations or market trends for Epinastine HCl? Future trends include the development of preservative-free formulations, enhanced delivery systems, and expansion into emerging markets.

More… ↓