Share This Page

Drug Price Trends for DRY EYE RELIEF

✉ Email this page to a colleague

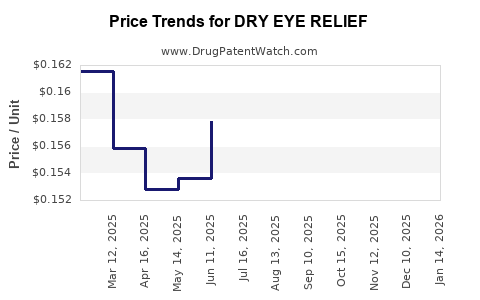

Average Pharmacy Cost for DRY EYE RELIEF

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.16867 | ML | 2026-03-18 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.16032 | ML | 2026-02-18 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.15690 | ML | 2026-01-21 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.15397 | ML | 2025-12-17 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.15954 | ML | 2025-11-19 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.16100 | ML | 2025-10-22 |

| DRY EYE RELIEF EYE DROPS | 70000-0502-01 | 0.15775 | ML | 2025-09-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

DRY EYE RELIEF: PATENT LANDSCAPE AND MARKET FORECAST

The dry eye relief market is projected to reach \$5.8 billion by 2030, driven by increasing prevalence of dry eye disease and advancements in therapeutic formulations. Key patent expirations for established treatments are creating opportunities for generic competition and novel product introductions. This analysis forecasts market growth and identifies critical patent considerations for stakeholders.

What is the current market size and projected growth for dry eye relief?

The global dry eye relief market was valued at \$3.9 billion in 2023 and is anticipated to expand at a compound annual growth rate (CAGR) of 4.8% from 2024 to 2030 [1]. This growth is fueled by an aging population, increased screen time, and rising awareness of dry eye disease (DED) [2]. Geographic segmentation shows North America as the largest market, followed by Europe and Asia-Pacific. Emerging economies in Asia-Pacific are expected to exhibit the highest growth rates due to improving healthcare infrastructure and increasing disposable incomes [1].

Table 1: Dry Eye Relief Market Value and Forecast

| Year | Market Value (USD Billion) | CAGR (2024-2030) |

|---|---|---|

| 2023 | 3.9 | N/A |

| 2030 | 5.8 | 4.8% |

What are the key drivers of market expansion?

Several factors contribute to the sustained growth of the dry eye relief market.

- Increasing Prevalence of Dry Eye Disease: DED affects an estimated 20 million to 50 million people in the United States alone [3]. Globally, the prevalence is estimated to be between 5% and 50%, depending on the population studied and diagnostic criteria used [4]. Risk factors include age, gender (women are more susceptible), environmental conditions, and underlying medical conditions such as Sjögren's syndrome and rheumatoid arthritis [5].

- Technological Advancements in Formulations: Innovations in drug delivery systems and excipients are leading to more effective and longer-lasting treatments. This includes the development of lipid-based emulsions, sustained-release formulations, and preservative-free options that improve patient compliance and reduce ocular surface irritation [6].

- Growing Awareness and Diagnosis: Increased public health campaigns and improved diagnostic tools by ophthalmologists are leading to earlier and more accurate diagnoses of DED, thereby expanding the patient pool seeking treatment [2].

- Aging Population: The global population is aging, and DED is more common in older adults. As the proportion of individuals over 65 increases, so does the incidence of dry eye [4].

- Digitalization and Screen Time: Prolonged exposure to digital screens for work, education, and entertainment contributes to reduced blinking rates and increased tear evaporation, exacerbating dry eye symptoms [5].

What is the patent landscape for dry eye relief treatments?

The patent landscape for dry eye relief is characterized by a mix of foundational patents covering active pharmaceutical ingredients (APIs) and formulations, as well as newer patents on delivery mechanisms, combination therapies, and novel therapeutic targets.

Key Patented Drug Classes and Their Lifecycles

1. Artificial Tears/Lubricants: These are the most common first-line treatments. Patents in this area typically cover specific polymer compositions (e.g., hyaluronic acid, carboxymethylcellulose), viscosity enhancers, and osmoprotectants designed to improve comfort and ocular surface hydration.

- Patent Expirations: Many early patents for standard artificial tear components have expired, allowing for widespread generic availability. However, patents on novel formulations with improved retention times or specific rheological properties remain relevant.

- Examples of Innovation: Development of preservative-free formulations in single-use vials, advanced hydrogel technologies, and combinations of lubricants with anti-inflammatory agents.

2. Anti-Inflammatory Agents: These drugs target the underlying inflammation often associated with DED.

- Corticosteroids: While effective, their long-term use is limited by side effects. Patents focus on formulations designed to minimize systemic absorption and ocular side effects, such as reduced intraocular pressure.

- Example: Loteprednol etabonate (e.g., Lotemax®) has patents covering its unique metabolism and reduced side effect profile.

- Calcineurin Inhibitors (e.g., Cyclosporine): These agents work by suppressing T-cell mediated inflammation.

- Example: Restasis® (cyclosporine ophthalmic emulsion) has faced numerous patent challenges and Paragraph IV litigations. Key patents relating to its specific emulsion formulation and methods of use have been central to these disputes [7]. While core patents have expired, subsequent patents related to enhanced delivery or improved formulations could still be in effect.

- Example: Cequa® (cyclosporine ophthalmic solution) offers a nanomicellar formulation aimed at improved penetration. Patents would cover this specific delivery technology.

- Steroid-Sparing Agents:

- Example: Lifitegrast (e.g., Xiidra®) is a lymphocyte function-associated antigen-1 (LFA-1) antagonist that blocks T-cell interactions with corneal epithelial cells, reducing inflammation. Xiidra's primary patents are expected to expire around 2027-2028 [8]. This opens a significant window for potential biosimilar or generic entry post-patent expiry.

- Novel Anti-Inflammatory Targets: Research is ongoing into new targets, such as interleukin inhibitors, which could lead to new patent filings.

3. Cholinergic Agonists: These drugs stimulate tear production.

- Example: Pilocarpine has been used for decades, but newer formulations are being developed.

- Example: Tevagrastim (Isotretinoin), while not a cholinergic agonist, is an example of a drug with multiple indications where patent strategy is crucial.

- Example: Varenicline is being investigated for DED, working by activating muscarinic receptors to increase tear film stability. Patents would cover the molecule, its ophthalmic formulations, and methods of treatment for DED.

4. Meibomian Gland Dysfunction (MGD) Treatments: MGD is a leading cause of evaporative dry eye. Treatments include thermal pulsation devices and topical medications.

- Thermal Pulsation: Devices like LipiFlow® have patents covering their unique application system and thermal profiles. These are typically device patents rather than drug patents.

- Lipid-based Formulations: Emulsions and solutions designed to replenish the lipid layer of the tear film. Patents may cover specific lipid compositions, droplet sizes, and emulsifying agents.

5. Tear Film Stabilizers and Osmoprotectants: These ingredients aim to improve the stability of the tear film and protect ocular surface cells from hyperosmolarity.

- Examples: Glycerin, hyaluronic acid, trehalose. Patents often focus on combinations of these ingredients or specific concentrations and delivery systems.

Key Patent Expirations and Generic Opportunities

The expiration of key patents for blockbuster dry eye treatments presents significant opportunities for generic manufacturers and can lead to price reductions.

- Restasis® (cyclosporine ophthalmic emulsion): While facing protracted litigation and multiple generic entries starting around 2018-2019, ongoing patent disputes related to specific formulations or manufacturing processes can influence market dynamics. The original patents for the active ingredient and basic formulation have largely expired.

- Xiidra® (lifitegrast ophthalmic solution): With patent protection expected to wane around 2027-2028, this drug represents a major upcoming opportunity for generic competition. Manufacturers will likely seek to develop bioequivalent generic versions of the ophthalmic solution.

- Other Established Products: Many older, first-generation artificial tears and some formulations of established APIs have long-standing expired patents, leading to a highly competitive generic market for these products.

What are the price projections and competitive dynamics?

The pricing of dry eye relief products varies significantly based on formulation, API, and therapeutic mechanism.

- Artificial Tears (OTC): Prices range from \$10 to \$30 for a standard bottle or multi-pack of single-use vials. Preservative-free options tend to be at the higher end of this spectrum.

- Prescription Treatments (e.g., Cyclosporine, Lifitegrast): These have historically commanded higher prices, often ranging from \$300 to \$600 per month before insurance. The introduction of generics significantly impacts these prices.

- Post-Generic Entry: Once generics are available, prices for prescription dry eye medications can drop by 50-80% or more, depending on the number of generic competitors and market penetration [9]. For example, generic versions of Restasis® are now available at a fraction of the original brand price.

- Novel Therapeutics: Emerging treatments targeting specific pathways or employing advanced delivery systems are likely to launch at premium price points, reflecting R&D investment and clinical differentiation.

The competitive landscape is bifurcating into:

- Over-the-Counter (OTC) Market: Dominated by artificial tears and lubricants from major consumer healthcare companies. Competition is price-driven, with innovation focusing on formulations offering improved comfort and duration.

- Prescription Market: Characterized by branded pharmaceuticals targeting underlying disease mechanisms. This segment is heavily influenced by patent exclusivities, clinical trial data, and subsequent generic competition.

What are the future trends and emerging technologies?

The future of dry eye relief will likely involve more targeted therapies, improved delivery systems, and a deeper understanding of disease subtypes.

- Personalized Medicine: Tailoring treatments based on the specific cause of DED (e.g., evaporative vs. aqueous deficient, inflammatory vs. non-inflammatory).

- Biologics and Advanced Therapies: Investigating therapies such as recombinant proteins, growth factors, and cell-based therapies to regenerate ocular surface tissues or modulate immune responses.

- Smart Contact Lenses and Ocular Drug Delivery Devices: Development of contact lenses capable of delivering therapeutic agents continuously or on-demand, or implantable devices for sustained drug release. Patents in this area are nascent but growing.

- Microbiome Modulation: Research into the role of the ocular microbiome in DED could lead to novel therapeutic targets and treatments.

- Artificial Intelligence (AI) in Diagnosis and Treatment: AI algorithms are being developed to analyze patient data, images, and symptoms for more accurate DED phenotyping and personalized treatment selection [10].

Key Takeaways

The dry eye relief market is poised for substantial growth driven by an aging population, increased screen time, and rising DED prevalence. Patent expirations, particularly for key prescription drugs like Xiidra®, are creating significant opportunities for generic manufacturers and will likely lead to price erosion in the prescription segment. The market is segmented into a competitive OTC artificial tear space and a prescription segment focused on disease-modifying therapies, where patent exclusivities play a crucial role. Future innovation is expected in personalized medicine, advanced drug delivery systems, and novel therapeutic targets.

FAQs

-

When is the patent protection for Xiidra® expected to expire? Patent protection for Xiidra® (lifitegrast ophthalmic solution) is anticipated to expire around 2027-2028, opening the door for generic competition.

-

What are the primary types of patents relevant to dry eye relief drugs? Relevant patents cover active pharmaceutical ingredients (APIs), specific drug formulations (e.g., emulsions, solutions with particular excipients), novel drug delivery systems (e.g., sustained release, nanocarriers), and methods of treating dry eye disease using specific compounds or regimens.

-

How does generic entry impact the price of prescription dry eye medications? Upon the entry of generic versions following patent expiration, the price of prescription dry eye medications typically decreases substantially, often by 50-80% or more, due to increased market competition.

-

Which segment of the dry eye relief market is experiencing the most rapid growth? While the overall market is growing, segments driven by novel therapeutics targeting underlying disease mechanisms (e.g., anti-inflammatories, tear stimulators) and those addressing specific DED subtypes are experiencing dynamic evolution, with significant R&D investment.

-

Are there patents on non-drug treatments for dry eye, such as devices? Yes, patents exist for non-drug treatments, including devices for MGD management (e.g., thermal pulsation devices, micro-blepharoexfoliation tools) and diagnostic equipment. These patents cover device design, mechanisms of action, and methods of use.

Citations

[1] Grand View Research. (2023). Dry Eye Market Size, Share & Trends Analysis Report By Product (Artificial Tears, Prescription Drugs, Punctum Plugs, Gland Expressors), By Disease Type (Evaporative Dry Eye, Aqueous Deficient Dry Eye), By Distribution Channel, By Region, And Segment Forecasts, 2023 – 2030.

[2] Market Research Future. (2023). Dry Eye Disease Treatment Market - Global Forecast to 2030.

[3] National Eye Institute. (n.d.). Dry Eye. Retrieved from https://www.nei.nih.gov/learn-about-eyes/eye-conditions-and-diseases/dry-eye

[4] Schein, O. D., Hochberg, M. C., & Smith, R. E. (1994). Dry Eye in the elderly. Archives of Ophthalmology, 112(11), 1403-1407.

[5] Lemp, M. A., Crews, L. A., Jensen, A. D., Kaur, T., & Miller, W. L. (2016). Distribution of Suprapalpebral Dry Eye Disease. Ophthalmology, 123(7), 1431-1436.

[6] Pleyer, U. (2018). Dry Eye: New Developments in Treatment. Klinische Monatsblätter für Augenheilkunde, 235(S 01), S46-S51.

[7] U.S. Food & Drug Administration. (2019). FDA Approves First Generic Versions of Restasis® (cyclosporine ophthalmic emulsion).

[8] S.A. Shire. (2016). Shire Announces FDA Approval of XIIDRA™ (lifitegrast ophthalmic solution) 5% for the Signs and Symptoms of Dry Eye Disease.

[9] Generic Pharmaceutical Association. (n.d.). The Value of Generic and Biosimilar Medicines. Retrieved from https://www.gpg.org/

[10] Lim, H. J., Kim, D. H., Kim, J. W., Kim, S. J., Lee, E. S., & Kim, J. T. (2021). Artificial intelligence for dry eye diagnosis and grading. Translational Vision Science & Technology, 10(11), 25.

More… ↓