Share This Page

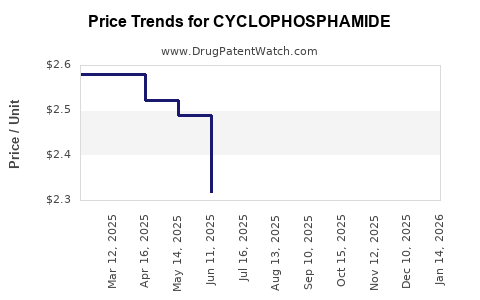

Drug Price Trends for CYCLOPHOSPHAMIDE

✉ Email this page to a colleague

Average Pharmacy Cost for CYCLOPHOSPHAMIDE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| CYCLOPHOSPHAMIDE 50 MG CAPSULE | 69097-0517-07 | 1.69623 | EACH | 2026-03-18 |

| CYCLOPHOSPHAMIDE 50 MG CAPSULE | 00054-0383-25 | 1.69623 | EACH | 2026-03-18 |

| CYCLOPHOSPHAMIDE 50 MG CAPSULE | 62332-0619-31 | 1.69623 | EACH | 2026-03-18 |

| CYCLOPHOSPHAMIDE 25 MG CAPSULE | 62332-0618-31 | 1.12118 | EACH | 2026-02-18 |

| CYCLOPHOSPHAMIDE 50 MG CAPSULE | 62332-0619-31 | 1.71092 | EACH | 2026-02-18 |

| CYCLOPHOSPHAMIDE 25 MG CAPSULE | 69097-0516-07 | 1.12118 | EACH | 2026-02-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for CYCLOPHOSPHAMIDE

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| CYCLOPHOSPHAMIDE 1GM/VIL INJ | A2A Alliance Pharmaceuticals, LLC | 81298-8112-01 | 1 | 303.60 | 303.60000 | EACH | 2024-04-25 - 2027-03-14 | FSS |

| CYCLOPHOSPHAMIDE 2GM/VIL INJ | A2A Alliance Pharmaceuticals, LLC | 81298-8114-01 | 1 | 542.40 | 542.40000 | EACH | 2024-04-25 - 2027-03-14 | FSS |

| CYCLOPHOSPHAMIDE 500MG/VIL INJ | A2A Alliance Pharmaceuticals, LLC | 81298-8110-01 | 1 | 141.60 | 141.60000 | EACH | 2024-04-25 - 2027-03-14 | FSS |

| CYCLOPHOSPHAMIDE 25MG CAP | Hikma Pharmaceuticals USA Inc. | 00054-0382-25 | 100 | 127.15 | 1.27150 | EACH | 2024-01-01 - 2026-08-14 | Big4 |

| CYCLOPHOSPHAMIDE 50MG CAP | Hikma Pharmaceuticals USA Inc. | 00054-0383-25 | 100 | 451.98 | 4.51980 | EACH | 2021-08-15 - 2026-08-14 | Big4 |

| CYCLOPHOSPHAMIDE 50MG CAP | Hikma Pharmaceuticals USA Inc. | 00054-0383-25 | 100 | 994.61 | 9.94610 | EACH | 2021-08-15 - 2026-08-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Cyclophosphamide Market Analysis and Price Projections

Cyclophosphamide, a cytotoxic chemotherapy agent, is projected to experience stable to moderate growth in the global market. Demand is driven by its established efficacy in treating a range of oncological and autoimmune diseases, alongside ongoing research into new therapeutic applications. However, market expansion may be constrained by the emergence of targeted therapies, biosimil competition, and pricing pressures in key markets.

What is Cyclophosphamide and its Primary Applications?

Cyclophosphamide is an alkylating agent used in chemotherapy and as an immunosuppressant. It functions by cross-linking DNA, which inhibits DNA replication and transcription, leading to cell death. Its primary applications include:

- Oncological Indications:

- Breast cancer (adjuvant and metastatic)

- Lymphomas (Hodgkin's and non-Hodgkin's)

- Leukemias (acute and chronic)

- Multiple myeloma

- Ovarian cancer

- Neuroblastoma

- Retinoblastoma

- Mycosis fungoides (Sezary syndrome)

- Autoimmune Diseases:

- Nephrotic syndrome (in children)

- Systemic lupus erythematosus (SLE)

- Rheumatoid arthritis (severe cases)

- Multiple sclerosis (certain forms)

- Wegener's granulomatosis

The drug is available in both intravenous (IV) and oral formulations. The IV form is typically administered in hospital or clinic settings, while the oral form allows for outpatient treatment.

What is the Current Market Size and Growth Trajectory for Cyclophosphamide?

The global cyclophosphamide market was valued at approximately \$600 million in 2023. The market is anticipated to grow at a compound annual growth rate (CAGR) of 3% to 4% over the next five years, reaching an estimated value of \$700 million to \$750 million by 2028. This growth rate is considered moderate, reflecting the drug's mature market status.

Factors influencing market size and trajectory:

- Established Treatment Protocols: Cyclophosphamide remains a cornerstone therapy for several cancers and autoimmune conditions, ensuring consistent demand. Its inclusion in standard treatment guidelines by organizations like the National Comprehensive Cancer Network (NCCN) and the European Society for Medical Oncology (ESMO) underpins its continued use.

- Geographic Penetration: The drug has widespread availability across North America, Europe, and Asia-Pacific. Developing economies, particularly in Asia, are expected to contribute to market growth due to increasing healthcare infrastructure and patient access.

- Generic Competition: Cyclophosphamide is a well-established generic drug. The presence of multiple generic manufacturers intensifies price competition, limiting significant revenue growth potential in developed markets where patent exclusivity has long expired.

- Advancements in Supportive Care: Improvements in managing side effects associated with chemotherapy, such as anti-emetics and colony-stimulating factors, enhance patient tolerance and compliance, indirectly supporting cyclophosphamide's utility.

- Emergence of Targeted Therapies: The development of novel, more targeted therapies and immunotherapies for certain cancers presents a competitive challenge. These newer agents often offer improved specificity and potentially reduced side effects, leading to shifts in treatment preferences for some patient populations. For example, in breast cancer, targeted therapies like trastuzumab and endocrine therapies have become standard, reducing the reliance on broad cytotoxic agents in certain subtypes.

What are the Key Drivers of Demand for Cyclophosphamide?

The persistent demand for cyclophosphamide is driven by a combination of clinical necessity, cost-effectiveness, and evolving treatment paradigms.

Key Demand Drivers:

- Cost-Effectiveness: As a generic medication with a long history of use, cyclophosphamide is significantly more cost-effective than many newer, branded therapies. This makes it a critical option in resource-limited settings and for healthcare systems managing budget constraints. The average wholesale price (AWP) for a standard 500mg vial can range from \$15 to \$30, a fraction of the cost of biologic or targeted therapy agents.

- Broad Spectrum of Efficacy: Its efficacy across a wide range of hematological malignancies, solid tumors, and autoimmune diseases makes it a valuable therapeutic option when other treatments are unsuitable or have failed. Its role in regimens like CHOP (cyclophosphamide, doxorubicin, vincristine, prednisone) for lymphoma continues to be significant.

- Immunosuppressive Properties: Its use in managing severe autoimmune diseases provides a stable demand stream independent of oncology markets. For conditions like lupus nephritis or severe rheumatoid arthritis, it remains a treatment of choice when other immunosuppressants are insufficient.

- Combination Therapy: Cyclophosphamide is frequently used in combination regimens. For instance, in breast cancer treatment, it is often part of anthracycline-based or taxane-based chemotherapy regimens. This integral role in established multi-drug protocols ensures its continued prescription.

- Pediatric Oncology: It is a vital drug in pediatric cancer treatment, particularly for leukemias and solid tumors, where its risk-benefit profile is well-understood and often favorable for younger patients.

What are the Major Restraints on Cyclophosphamide Market Growth?

While cyclophosphamide maintains a strong market presence, several factors are expected to temper its growth trajectory.

Market Restraints:

- Development of Targeted Therapies and Immunotherapies: The oncology landscape is rapidly shifting towards precision medicine. Highly specific targeted drugs and immunotherapies are demonstrating superior efficacy and tolerability in certain cancers, leading to their adoption over broader cytotoxic agents like cyclophosphamide for specific patient groups and cancer types. For example, the advent of PARP inhibitors for BRCA-mutated ovarian and breast cancers offers an alternative to cyclophosphamide in certain settings.

- Adverse Event Profile: As a cytotoxic agent, cyclophosphamide carries a significant toxicity profile, including myelosuppression, nausea, vomiting, alopecia, hemorrhagic cystitis, and an increased risk of secondary malignancies. These side effects can limit patient compliance and lead to treatment discontinuation, pushing physicians to consider alternatives with better tolerability.

- Competition from Biosimil and Generic Drugs: The highly competitive generic market for cyclophosphamide exerts downward pressure on prices. While this benefits healthcare systems, it limits revenue growth for manufacturers. The availability of multiple low-cost generic alternatives means that pricing power is minimal.

- Stringent Regulatory Requirements: While cyclophosphamide is an established drug, regulatory bodies continually review drug safety and efficacy. Changes in prescribing guidelines or heightened scrutiny on long-term toxicities could indirectly impact its utilization.

- Shifting Treatment Paradigms in Autoimmune Diseases: In autoimmune disorders, newer biologic agents and targeted small molecules are increasingly being developed and approved, offering alternative mechanisms of action and potentially improved safety profiles for specific conditions, thus gradually eroding cyclophosphamide's market share in these indications.

What are the Pricing Trends and Projections for Cyclophosphamide?

The pricing of cyclophosphamide is characterized by stability with slight downward pressure due to generic competition.

Pricing Trends:

- Generic Price Erosion: Due to the presence of numerous generic manufacturers, prices for cyclophosphamide have stabilized and are subject to ongoing negotiation between buyers (hospitals, pharmacies, distributors) and sellers. The average AWP for a 500mg vial has remained relatively consistent, fluctuating within a \$15-\$30 range.

- Volume-Based Purchasing: Large hospital networks and group purchasing organizations (GPOs) leverage their purchasing power to negotiate volume discounts, further intensifying price competition among generic suppliers.

- Regional Price Variations: Significant price variations exist across different geographic regions, influenced by local regulatory policies, reimbursement landscapes, and the competitive intensity of generic manufacturers in those markets.

- Formulation Costs: While the active pharmaceutical ingredient (API) cost is low, manufacturing, packaging, and distribution costs contribute to the final product price. The oral formulation may carry a slightly higher price per milligram compared to the injectable form due to different manufacturing and packaging complexities.

Price Projections:

- Stable to Slight Decline: Over the next five years, the price of cyclophosphamide is projected to remain largely stable, with a potential for a slight decline of 1% to 2% annually, primarily driven by continued generic competition and the purchasing power of large healthcare entities.

- No Significant Price Increases Expected: Given its generic status and the availability of therapeutic alternatives, substantial price increases are not anticipated.

- Impact of Supply Chain Fluctuations: While not a primary driver, minor price fluctuations could occur due to unforeseen supply chain disruptions affecting API availability or manufacturing capacity, although these are generally short-lived in the context of a mature generic drug.

What is the Competitive Landscape for Cyclophosphamide Manufacturers?

The cyclophosphamide market is highly fragmented and dominated by generic manufacturers. The barriers to entry are relatively low for producing generic versions of off-patent drugs.

Key Characteristics of the Competitive Landscape:

- Numerous Generic Players: The market includes a large number of companies that manufacture and market generic cyclophosphamide. These include both large multinational pharmaceutical companies with generic divisions and smaller regional manufacturers.

- Focus on Manufacturing Efficiency: Competition primarily centers on cost-effective manufacturing, efficient supply chain management, and meeting regulatory quality standards.

- Geographic Distribution: Manufacturers operate globally, with significant production capabilities located in India and China, known for their cost-effective API and finished dosage form production.

- Key Manufacturers (examples, not exhaustive): Companies that are active in the generic cyclophosphamide market or have historically been significant suppliers include (but are not limited to) Teva Pharmaceutical Industries Ltd., Mylan N.V. (now Viatris), Fresenius Kabi AG, Hikma Pharmaceuticals PLC, and various Indian and Chinese API manufacturers. Specific product availability may vary by region.

- Limited R&D Investment: As a mature, off-patent drug, there is minimal investment in research and development for novel formulations or new indications by most manufacturers. The focus is on maintaining cost competitiveness and supply reliability.

- Acquisitions and Consolidations: The generic pharmaceutical industry has seen a trend of mergers and acquisitions. This can lead to consolidation among manufacturers, potentially altering the competitive dynamics for specific drugs like cyclophosphamide.

What are the Future Outlook and Emerging Trends for Cyclophosphamide?

The future of cyclophosphamide is one of sustained, albeit modest, utility, with its role evolving rather than expanding dramatically.

Future Outlook and Trends:

- Continued Role in Combination Therapies: Cyclophosphamide will likely remain an integral component of established chemotherapy regimens for certain cancers where its efficacy and cost-effectiveness are well-proven. Regimens like CMF (cyclophosphamide, methotrexate, fluorouracil) for breast cancer, although older, may still see use in specific patient populations or regions.

- Niche Applications in Autoimmune Diseases: Its use as an immunosuppressant in severe autoimmune conditions is expected to persist, particularly in areas where access to newer biologics is limited or where cyclophosphamide has demonstrated long-term efficacy.

- Potential for Repurposing (Limited): While significant investment in exploring new uses for older cytotoxic agents is limited due to the preference for targeted therapies, ongoing research in areas like microbiome modulation or novel drug delivery systems could, in the long term, identify niche applications or improved administration methods. However, this is not a significant market driver in the near to medium term.

- Focus on Supply Chain Resilience: Given its essential medicine status, ensuring a stable and resilient global supply chain for cyclophosphamide will remain a priority for manufacturers and regulatory bodies. Disruptions could lead to shortages, highlighting the importance of diversified manufacturing and inventory management.

- Impact of Biosimilar Development (Indirect): While cyclophosphamide is a small molecule and not a biologic, the general trend towards biosimilarity in other drug classes underscores the competitive pressures faced by all older medications. This environment encourages ongoing cost optimization for cyclophosphamide production.

- Digital Health Integration (Minimal): Direct integration of digital health tools with cyclophosphamide therapy is unlikely to be a major trend. Its use is primarily driven by clinical efficacy and cost, with treatment decisions made by oncologists and rheumatologists based on established protocols.

Key Takeaways

- Cyclophosphamide is a mature generic drug with a stable market, projected to grow at a CAGR of 3-4% to \$700-750 million by 2028.

- Demand is sustained by its established efficacy in oncology and autoimmune diseases, and its cost-effectiveness.

- Market growth is restrained by the emergence of targeted therapies, its adverse event profile, and intense generic competition.

- Pricing is stable with downward pressure from generics and volume-based purchasing, with no significant price increases anticipated.

- The competitive landscape is dominated by numerous generic manufacturers focused on cost efficiency and supply reliability.

- Future trends indicate continued use in combination therapies and niche autoimmune applications, with a focus on supply chain resilience.

Frequently Asked Questions

1. What is the typical treatment duration for cyclophosphamide in oncological indications?

Treatment duration varies significantly based on the specific cancer type, stage, and treatment protocol. For adjuvant breast cancer, it might be part of a regimen lasting several months. For lymphomas or leukemias, treatment courses can extend over weeks to months, often involving cyclical administration.

2. How does cyclophosphamide's immunosuppressive mechanism differ from other immunosuppressants used in autoimmune diseases?

Cyclophosphamide's immunosuppression is a consequence of its cytotoxic action on rapidly dividing cells, including lymphocytes. It depletes lymphocyte populations. Other immunosuppressants may target specific immune pathways (e.g., TNF inhibitors, JAK inhibitors) or have different mechanisms of B-cell depletion (e.g., rituximab).

3. What are the primary side effects that healthcare providers monitor during cyclophosphamide therapy?

Key side effects monitored include myelosuppression (leading to neutropenia, anemia, thrombocytopenia), nausea and vomiting, alopecia (hair loss), hemorrhagic cystitis (bladder inflammation, managed with hydration and mesna), and potential long-term risks like infertility and secondary malignancies.

4. Are there any significant differences in efficacy or safety between oral and intravenous cyclophosphamide?

Oral and intravenous cyclophosphamide are generally considered bioequivalent in terms of systemic exposure. The primary difference lies in administration convenience and potentially absorption variability with the oral form, which can be influenced by food intake. IV administration ensures precise dosing and is often preferred in acute settings or for higher doses.

5. What is the expected impact of emerging cancer immunotherapies on the long-term demand for cyclophosphamide?

Emerging immunotherapies are primarily shifting treatment paradigms for specific cancer types where they offer superior outcomes or better tolerability. While they may reduce cyclophosphamide's use in those specific indications, cyclophosphamide's broad utility in other cancers, its role in combination regimens, and its cost-effectiveness are expected to ensure its continued demand in the broader oncology market, albeit potentially at a slower growth rate.

Citations

[1] National Cancer Institute. (n.d.). Cyclophosphamide. Retrieved from https://www.cancer.gov/drug-dictionary/cyclophosphamide [2] L. P. P. N. B. L. B. P. V. V. L. B. B. B. V. S. P. (2021). Cyclophosphamide in autoimmune diseases. Journal of Autoimmunity, 120, 102617. [3] National Comprehensive Cancer Network. (n.d.). Clinical Practice Guidelines in Oncology. Retrieved from https://www.nccn.org/guidelines (Specific guidelines vary by cancer type and are accessible via subscription or institutional access). [4] European Society for Medical Oncology. (n.d.). ESMO Clinical Practice Guidelines. Retrieved from https://www.esmo.org/guidelines (Specific guidelines vary by cancer type and are accessible via subscription or institutional access). [5] IQVIA Institute for Human Data Science. (Various Years). Global medicine spending and promotion: Outlook and methodology. (Reports cited for general market trends and drug spending analysis). [6] U.S. Food & Drug Administration. (n.d.). Drug Approval Database. Retrieved from https://www.fda.gov/drugs/informationondrugs/approved-drugs/ (Used for verifying drug approval status and historical context).

More… ↓