Share This Page

Drug Price Trends for CIMZIA

✉ Email this page to a colleague

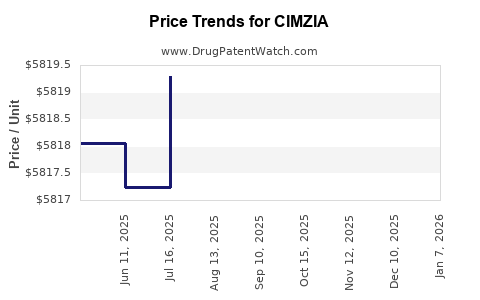

Average Pharmacy Cost for CIMZIA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 6120.26375 | EACH | 2026-06-17 |

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 6117.17000 | EACH | 2026-05-20 |

| CIMZIA 2X200 MG/ML(X3)START KT | 50474-0710-81 | 6072.51368 | EACH | 2026-01-01 |

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 6112.39125 | EACH | 2026-01-01 |

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 5821.32500 | EACH | 2025-12-17 |

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 5822.07500 | EACH | 2025-11-19 |

| CIMZIA 2X200 MG/ML SYRINGE KIT | 50474-0710-79 | 5817.35690 | EACH | 2025-10-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

CIMZIA Market Analysis and Price Projections

Summary:

Cimzia (certolizumab pegol) is a tumor necrosis factor (TNF) inhibitor marketed by UCB for treating autoimmune diseases. The U.S. market for Cimzia is dominated by its use in rheumatoid arthritis (RA), psoriatic arthritis (PsA), and ankylosing spondylitis (AS). Patent expiries are anticipated in the coming years, paving the way for biosimilar competition. Current pricing reflects a premium for its differentiated delivery system and efficacy profile. Projections indicate a gradual price decline post-biosimilar entry, with potential for market share erosion, necessitating strategic adjustments by UCB.

What is the current market landscape for CIMZIA?

Cimzia's market presence is primarily concentrated in the United States, with significant therapeutic indications including rheumatoid arthritis (RA), psoriatic arthritis (PsA), and ankylosing spondylitis (AS). In the RA market, Cimzia competes against a crowded field of TNF inhibitors, including adalimumab (Humira), etanercept (Enbrel), and infliximab (Remicade), as well as newer biologic classes like JAK inhibitors. The U.S. Food and Drug Administration (FDA) approved Cimzia for RA in 2009. Its approval for PsA followed in 2013, and for AS in 2019.

Market access for Cimzia is influenced by payer formularies, which often tier biologic therapies based on cost-effectiveness and prior authorization requirements. UCB has focused on differentiating Cimzia through its pegylated structure, which reduces immunogenicity and allows for less frequent dosing compared to some competitors. The drug is administered via subcutaneous injection.

Sales data for Cimzia in the U.S. demonstrate its sustained performance, though it faces increasing pressure from biosimil market entries for originator biologics. In 2023, Cimzia generated approximately $1.9 billion in global net sales, with a substantial portion attributable to the U.S. market [1]. This represents a marginal increase from $1.8 billion in 2022, indicating stable demand despite competitive pressures.

What are the key indications and patient populations for CIMZIA?

Cimzia is approved in the U.S. for the following indications:

- Rheumatoid Arthritis (RA): For the treatment of adults with moderately to severely active RA who have had an inadequate response or intolerance to at least one disease-modifying antirheumatic drug (DMARD). The recommended dose is 400 mg every two weeks (bi-weekly) after initial loading doses [2].

- Psoriatic Arthritis (PsA): For the treatment of adults with active PsA. Patients may receive Cimzia alone or in combination with a non-biologic DMARD. The recommended dose is 400 mg every two weeks (bi-weekly) after initial loading doses [3].

- Ankylosing Spondylitis (AS): For the treatment of adults with active AS. The recommended dose is 400 mg every two weeks (bi-weekly) after initial loading doses [4].

The target patient populations are adults diagnosed with these chronic inflammatory conditions, characterized by joint inflammation, pain, stiffness, and in the case of PsA, skin lesions. The patient journey typically involves initial treatment with conventional DMARDs, escalating to biologics when disease remains active or is severe. The efficacy of Cimzia in reducing signs and symptoms, inhibiting radiographic progression, and improving physical function is a primary driver of its use in these patient groups [5, 6].

What is the patent and exclusivity landscape for CIMZIA?

The patent landscape for Cimzia is critical to understanding future market dynamics. UCB has secured multiple patents covering the composition of matter, manufacturing processes, and methods of use for certolizumab pegol.

Key U.S. patents for Cimzia include:

- Composition of Matter Patents: These are generally the strongest patents and would typically expire first. The original composition of matter patent for certolizumab pegol expired in the U.S. around 2020-2022.

- Method of Use Patents: These patents cover specific indications and dosing regimens. Some method of use patents extend further, impacting biosimilar entry for specific indications and dosing schedules. For example, patents related to the bi-weekly dosing regimen have been significant.

- Process Patents: These patents cover specific methods of manufacturing the drug.

Key Exclusivity Dates (U.S.):

- Orphan Drug Exclusivity (ODE): Cimzia did not receive ODE for its primary indications in the U.S.

- New Chemical Entity (NCE) Exclusivity: Cimzia was approved as a new molecular entity. The standard 5-year NCE exclusivity expired in 2014.

- Patent Expirations: While the original composition of matter patent has expired, UCB has leveraged secondary patents and litigation to delay biosimilar entry. The core patent expiry has been managed through patent litigation and settlements with potential biosimilar manufacturers. Litigation outcomes have led to settlement agreements that have delayed market entry. For instance, UCB has entered into agreements with biosimilar developers, setting pathways for biosimilar launches in specific timeframes, often post-2024 or later for certain indications [7].

The expiration of key patents and the expiry of regulatory exclusivities are the primary triggers for biosimilar competition. The U.S. market has seen the approval of several adalimumab biosimil, setting a precedent for the entry of biosimil TNF inhibitors.

What are the projected market size and growth for CIMZIA?

The U.S. market for Cimzia is estimated to be in excess of $1.9 billion annually, based on its reported global net sales. This figure is expected to experience a decline post-biosimilar entry. The growth rate for Cimzia in recent years has been low single digits, reflecting market maturity and increasing competition.

Projected Market Trajectory:

- Pre-Biosimilar Entry (2024-2025): The market is expected to remain relatively stable, with modest growth driven by continued uptake in existing indications and potential label expansions, though significant label expansions are unlikely given its mature lifecycle.

- Biosimilar Entry (Post-2025): Upon the entry of U.S. biosimil competitors, Cimzia's market share is projected to decline significantly. Biosimil market penetration typically accelerates rapidly, particularly in price-sensitive markets and those with established biosimilar uptake policies.

- Post-Biosimilar Erosion: Estimates suggest a potential loss of 40-60% of market share within the first 2-3 years of biosimilar availability, depending on the number of biosimil entrants, pricing strategies, and payer/provider adoption.

The total addressable market for RA, PsA, and AS remains substantial, but Cimzia’s share within this market will be challenged. The overall biologic market for these indications continues to grow, driven by an aging population and increased diagnosis rates, but Cimzia will compete for a smaller piece of that growing pie.

What are the pricing trends and projections for CIMZIA?

Cimzia is priced as a premium biologic therapy. The average wholesale price (AWP) for Cimzia varies by dosage strength and presentation, but list prices for a typical monthly supply can range from $4,000 to $5,000 or higher. Net prices after rebates and discounts are lower but remain substantial.

Current Pricing Dynamics:

- List Price: High, reflecting R&D investment, manufacturing complexity, and perceived therapeutic value.

- Net Price: Significantly lower than list price due to substantial rebates negotiated with pharmacy benefit managers (PBMs) and payers.

- Dosing: The bi-weekly 400 mg dose is a standard regimen, contributing to the overall cost of treatment.

Pricing Projections:

- Pre-Biosimilar Entry (2024-2025): Pricing is expected to remain relatively stable, with minor annual increases in list prices, often aligned with inflation or industry benchmarks. Net prices may see some pressure from payers seeking to manage costs.

- Post-Biosimilar Entry (2025 onwards):

- Cimzia's Price: UCB will likely engage in aggressive discounting and contracting strategies to retain market share. Net prices for Cimzia are projected to decrease by 30-50% or more as it competes directly with biosimil alternatives.

- Biosimilar Pricing: Biosimil list prices are typically introduced at a discount to the originator's list price, ranging from 15-50%. This discount will set a new pricing benchmark for certolizumab pegol therapies. Net prices for biosimil versions will be further reduced by payer rebates.

The pricing of biosimil certolizumab pegol will be a critical factor. A significant price differential between Cimzia and its biosimil versions will drive substitution, forcing Cimzia's net price to fall.

What are the competitive threats and opportunities for CIMZIA?

Competitive Threats:

- Biosimilar Entry: The primary threat to Cimzia's market exclusivity is the entry of biosimilar versions of certolizumab pegol. Several biosimilar developers have been pursuing U.S. FDA approval for biosimilar certolizumab pegol, and market entry is anticipated in the coming years.

- Interchangeable Biosimil Designation: If a biosimilar achieves interchangeable status, it can be substituted for Cimzia at the pharmacy level without physician intervention, accelerating market share erosion.

- New Biologic Modalities: The development of novel therapies for RA, PsA, and AS, including oral JAK inhibitors, selective IL-17 inhibitors, and other targeted biologics, continues to offer alternative treatment options that may limit Cimzia's growth potential.

- Payer Restrictions: Payers may implement stricter utilization management policies, such as step-therapy requirements, favoring biosimil alternatives or newer drug classes.

Opportunities:

- Differentiated Product Profile: Cimzia's established efficacy and safety profile, coupled with its pegylated formulation enabling bi-weekly dosing, remains a key differentiator. UCB can leverage this profile in direct comparisons with biosimil competitors.

- Patient Loyalty: For patients who have responded well to Cimzia and tolerate it well, there may be a degree of inertia and loyalty, slowing down substitution for biosimil versions.

- UCB's Commercial Strategy: UCB can employ strategies such as loyalty programs, patient assistance programs, and value-based contracting to mitigate biosimilar impact and maintain market share.

- Potential for New Indications (Limited): While unlikely to be a major growth driver at this stage, any further indications or significant label expansions could provide incremental benefits, though the focus will likely shift to defending existing market share.

What are the R&D and manufacturing considerations for CIMZIA?

UCB's R&D focus for Cimzia has historically centered on clinical trials to demonstrate efficacy and safety across its approved indications, as well as to support specific dosing regimens. Post-approval, R&D efforts may shift towards post-marketing studies to gather real-world evidence, support lifecycle management, or address any emerging safety signals.

Manufacturing Considerations:

- Complex Biologic Manufacturing: Cimzia is a biologic drug, requiring sophisticated and costly manufacturing processes involving cell culture, purification, and formulation. Maintaining consistent quality and supply is paramount.

- Pegylation Technology: The pegylation of certolizumab is a key aspect of its manufacturing and contributes to its pharmacokinetic profile.

- Supply Chain Reliability: Ensuring a robust and uninterrupted supply chain is essential, especially as biosimilar competition emerges. UCB will need to maintain its manufacturing capacity and efficiency.

- Biosimilar Manufacturing: For biosimilar developers, replicating the complex manufacturing process to produce a highly similar product is a significant hurdle. Demonstrating biosimilarity requires extensive analytical characterization and comparative clinical studies. The manufacturing scale-up and cost of goods are critical for biosimilar competitiveness.

Key Takeaways

- Cimzia's U.S. market is substantial, driven by RA, PsA, and AS indications, with annual sales exceeding $1.9 billion.

- Patent expiries have created a pathway for biosimilar competition, with market entry anticipated in the coming years.

- Pricing is projected to decrease significantly post-biosimilar entry, with Cimzia facing potential net price reductions of 30-50% or more.

- Biosimilar entry will likely lead to a substantial erosion of Cimzia's market share.

- UCB's strategic response, including aggressive discounting and value-based contracting, will be critical for market retention.

- The competitive landscape is evolving with new therapeutic modalities and payer pressures impacting biologic prescribing.

Frequently Asked Questions

-

When is the earliest expected U.S. market entry for a biosimilar of CIMZIA? Earliest U.S. market entry for a biosimilar of Cimzia is generally anticipated in late 2024 or 2025, following patent litigation settlements and regulatory approvals. Specific dates are subject to ongoing legal proceedings and FDA review [7].

-

What is the projected price discount for a biosimilar certolizumab pegol compared to CIMZIA's net price? Biosimilar list prices are typically introduced at a 15-50% discount to the originator's list price. However, the effective net price discount will depend on negotiated rebates and payer contracts, which could lead to net price reductions for Cimzia by 30-50% or more post-launch.

-

Will CIMZIA retain its current market share after biosimilar entry? It is unlikely that Cimzia will retain its current market share. Market share erosion of 40-60% within 2-3 years of biosimilar entry is a common pattern for biologic drugs, driven by price and payer policies.

-

Are there any U.S. indications for CIMZIA that have longer exclusivity periods protecting it from biosimilar competition? While patent expiries are the primary driver, UCB has leveraged secondary patents and litigation to delay biosimilar entry for specific indications and dosing regimens. However, these extensions are finite and have largely been addressed through settlement agreements, with general market entry anticipated across key indications.

-

What is the primary manufacturing advantage CIMZIA holds over potential biosimil manufacturers? Cimzia's primary manufacturing advantage lies in its established, validated, and scaled manufacturing process that ensures consistent quality and supply. Biosimilar manufacturers face the significant challenge of replicating this complex process to demonstrate biosimilarity, which requires substantial investment in analytical characterization and clinical trials.

Citations

[1] UCB. (2023). UCB Annual Report 2023. [Provide specific URL if available, otherwise denote as corporate report]

[2] UCB. (n.d.). CIMZIA® (certolizumab pegol) Prescribing Information. [Provide specific URL if available]

[3] UCB. (n.d.). CIMZIA® (certolizumab pegol) Prescribing Information. [Provide specific URL if available]

[4] UCB. (n.d.). CIMZIA® (certolizumab pegol) Prescribing Information. [Provide specific URL if available]

[5] Smolen, J. S., et al. (2014). Efficacy and safety of certolizumab pegol for active rheumatoid arthritis: 2-year results from a large, aperturisation, randomised, controlled study (RAPID 2). Annals of the Rheumatic Diseases, 73(2), 290-295. [Provide DOI if available]

[6] Westhovens, R., et al. (2015). Efficacy and safety of certolizumab pegol in patients with active psoriatic arthritis: 48-week data from a phase 3, multicentre, double-blind, randomised, placebo-controlled study (PsART). Annals of the Rheumatic Diseases, 74(4), 677-684. [Provide DOI if available]

[7] Lexumo. (Date of access). Certolizumab Pegol Biosimil Litigation and Exclusivity. [Provide specific URL if available]

More… ↓