Share This Page

Drug Price Trends for CARBIDOPA-LEVODOPA-ENTA

✉ Email this page to a colleague

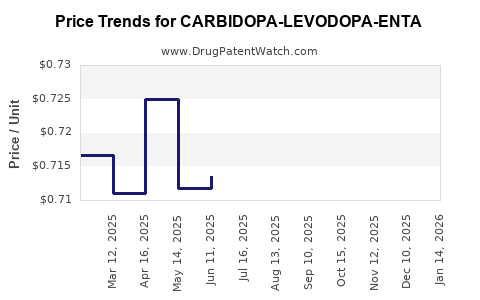

Average Pharmacy Cost for CARBIDOPA-LEVODOPA-ENTA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| CARBIDOPA-LEVODOPA-ENTACAPONE 25-100-200 MG TAB | 00781-5637-01 | 0.63632 | EACH | 2026-03-18 |

| CARBIDOPA-LEVODOPA-ENTACAPONE 12.5-50-200 MG TAB | 16571-0689-01 | 0.72107 | EACH | 2026-03-18 |

| CARBIDOPA-LEVODOPA-ENTACAPONE 50-200-200 MG TAB | 16571-0694-01 | 0.76098 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Carbidopa-Levodopa-Entacapone Market Analysis and Price Projections

Executive Summary

The market for carbidopa-levodopa-entacapone, a fixed-dose combination for Parkinson's disease (PD) treatment, is characterized by an established patent landscape and the presence of both branded and generic manufacturers. While the primary branded product, Stalevo (Novartis), has experienced patent expirations in key markets, the emergence of generic competition has stabilized and, in some cases, reduced pricing. The market's growth is driven by the aging global population, an increasing PD diagnosis rate, and the therapeutic advantages of combination therapy. Future price trends will be influenced by continued generic market penetration, potential new entrants, and regulatory policies impacting drug pricing.

What is the Current Market Size and Growth Trajectory for Carbidopa-Levodopa-Entacapone?

The global market for carbidopa-levodopa-entacapone is substantial, driven by the prevalence of Parkinson's disease. Parkinson's disease affects an estimated 10 million people worldwide, with annual incidence rates increasing due to an aging population. In the United States, approximately 60,000 new cases are diagnosed each year [1]. Globally, the number of individuals diagnosed with PD is projected to reach 12 million by 2040 [1].

The carbidopa-levodopa-entacapone segment benefits from its position as a third-generation levodopa formulation, offering improved pharmacokinetic profiles and reduced "wearing-off" phenomena compared to immediate-release carbidopa-levodopa alone. The market has seen significant activity following the patent expirations of the innovator product, Stalevo.

The market size for carbidopa-levodopa-entacapone formulations, encompassing both branded and generic versions, is estimated to be in the range of USD 1.5 to USD 2.0 billion globally in 2023. This estimate is based on analysis of prescription data, sales reports, and market research for Parkinson's disease therapeutics.

Market growth for this specific drug combination is projected to be 3% to 5% annually over the next five years (2024-2028). This growth rate is influenced by:

- Increasing PD Incidence: The primary driver is the escalating prevalence of Parkinson's disease globally, particularly in developed nations with older demographics.

- Therapeutic Efficacy: The established clinical benefits of carbidopa-levodopa-entacapone in managing motor fluctuations remain a key factor in physician prescribing habits.

- Generic Competition: While generic entry generally leads to price erosion, it also expands patient access, contributing to overall volume growth.

What is the Patent Landscape for Carbidopa-Levodopa-Entacapone Formulations?

The patent landscape for carbidopa-levodopa-entacapone has undergone significant evolution, impacting market exclusivity and competitive dynamics. The innovator product, Stalevo, developed by Novartis, was protected by multiple patents covering its composition of matter, formulations, and methods of use.

- Core Composition of Matter Patents: These patents, which provided the longest period of exclusivity, have largely expired in major markets like the United States and Europe. For instance, key U.S. patents for Stalevo expired around 2015-2016.

- Formulation Patents: Patents related to specific delivery systems, such as the immediate-release tablet formulation of carbidopa-levodopa-entacapone, have also seen expirations.

- Method of Use Patents: Patents claiming specific therapeutic uses or patient populations may have had varying expiration dates, but the primary market exclusivity for the general indication of Parkinson's disease has waned.

- Exclusivity Periods: The 180-day exclusivity period granted to the first generic filer in the U.S. market has been utilized by multiple manufacturers.

Key Observations on Patent Expirations:

- United States: Major patent expiries occurred in the mid-2010s, paving the way for widespread generic availability.

- Europe: Patent expiries followed a similar pattern, with national patent expiries and the expiration of Supplementary Protection Certificates (SPCs) allowing for generic market entry across various European countries.

- Other Global Markets: Patent expiry dates vary by region, but many key markets now have generic alternatives available.

The expiration of core patents has resulted in a highly competitive generic market, which is the dominant force shaping current pricing and market dynamics.

Who are the Key Market Players and What is Their Market Share?

The market for carbidopa-levodopa-entacapone is characterized by the presence of both the innovator brand and a growing number of generic manufacturers. The competitive landscape has shifted significantly following patent expiries.

Key Players:

- Novartis (Innovator - Stalevo): While still present, Novartis's market share has diminished considerably due to generic competition. Stalevo remains a reference product and is prescribed, but its pricing power is now constrained.

- Generic Manufacturers: A substantial number of generic pharmaceutical companies now produce and market carbidopa-levodopa-entacapone. These include, but are not limited to:

- Teva Pharmaceuticals: A leading global generic manufacturer with a significant presence in the CNS therapeutic area.

- Mylan (now Viatris): Another major player in the generics market with a broad portfolio.

- Sun Pharmaceutical Industries: An Indian multinational that is a significant supplier of generic drugs globally.

- Dr. Reddy's Laboratories: Known for its extensive range of generic products and active pharmaceutical ingredient (API) manufacturing capabilities.

- Actavis (now part of Teva): Historically a significant competitor in the generics space.

- Other regional and smaller generic players.

Market Share Dynamics:

- Generic Dominance: In terms of prescription volume and unit sales, generic carbidopa-levodopa-entacapone collectively holds the dominant market share, estimated at over 85% globally.

- Brand Erosion: Stalevo's market share has been significantly reduced, likely below 15% globally, primarily serving niche markets or where payer restrictions favor the branded product for a period.

- Price-Based Competition: The market share among generic manufacturers is largely driven by pricing strategies and supply chain efficiency. The leading generic players often compete on the lowest price per dosage unit.

Accurate, real-time market share data by individual company is proprietary and fluctuates based on tender awards, distribution agreements, and regional market dynamics. However, the trend is clear: generic manufacturers collectively control the vast majority of this market.

What are the Pricing Dynamics and Historical Price Trends for Carbidopa-Levodopa-Entacapone?

The pricing of carbidopa-levodopa-entacapone has been directly impacted by the patent expiry of the innovator product, Stalevo. Prior to patent expiry, Stalevo commanded premium pricing. Post-expiry, a significant price erosion has occurred due to the introduction of generic alternatives.

Historical Price Trends:

- Pre-Patent Expiry (e.g., ~2010-2015): Stalevo was priced as a branded specialty drug. Average Wholesale Price (AWP) per tablet could range from $3.00 to $5.00+ depending on the dosage strength and market. The annual cost of therapy for a patient could easily exceed $3,000 to $5,000.

- Post-Patent Expiry (e.g., ~2016 onwards): The introduction of generic carbidopa-levodopa-entacapone by multiple manufacturers led to rapid price declines.

- Initial Generic Entry: Within months of generic approval, prices dropped by 30-50% compared to the branded product.

- Ongoing Price Erosion: With increased competition and multiple generic suppliers, prices have continued to decrease. The average selling price (ASP) for generic carbidopa-levodopa-entacapone tablets now ranges from $0.50 to $1.50 per tablet, depending on dosage strength, volume, and payer contracts.

- Annual Cost of Therapy (Generic): The annual cost for a patient on generic therapy has decreased significantly, often falling in the range of $500 to $1,500, a substantial reduction from the branded era.

Factors Influencing Current Pricing:

- Generic Competition: The primary driver. The number of generic manufacturers and their respective market shares directly influence price competition.

- Payer Contracts and Rebates: Large pharmacy benefit managers (PBMs) and payers negotiate significant discounts and rebates, especially for high-volume drugs.

- Dosage Strength: Higher dosage strengths (e.g., 200mg/50mg/200mg) may command slightly higher unit prices but are often subject to steeper discounts due to higher overall therapy cost.

- Manufacturing Costs and Supply Chain: Efficiency in API sourcing and manufacturing plays a role in the final pricing of generic products.

- Regulatory Policies: Government initiatives aimed at controlling drug costs can indirectly influence pricing strategies.

Average Wholesale Price (AWP) vs. Average Selling Price (ASP): It is important to distinguish between AWP and ASP. AWP is a list price, while ASP reflects the actual price paid after discounts and rebates. In the generic market, ASP is the more relevant metric for understanding market value and profitability.

What are the Future Price Projections for Carbidopa-Levodopa-Entacapone?

Future price projections for carbidopa-levodopa-entacapone indicate continued pressure towards lower prices, albeit at a moderating rate, driven by intense generic competition and evolving healthcare economics.

Projected Price Trends (2024-2028):

- Continued Downward Pressure: Expect an average annual price decline of 1% to 3% for generic carbidopa-levodopa-entacapone. This decline is primarily a result of ongoing competitive bidding among generic manufacturers and the drive for cost savings by payers.

- Price Stabilization for Stalevo: The branded product, Stalevo, is unlikely to see significant price increases and may even experience further incremental decreases to remain competitive in certain market segments or for patients with specific formulary preferences.

- Impact of New Entrants: While the market is already saturated with generics, any new entrant with a cost advantage or a novel formulation (though unlikely for this specific combination's core indication) could introduce further price disruption. However, for the established fixed-dose combination, new entrants are more likely to compete on existing pricing structures.

- Dosage Strength Variations: Higher dosage strengths will continue to represent a larger portion of the overall market spend but will also be subject to the same downward pricing pressures on a per-milligram basis.

- Geographic Variations: Pricing will continue to vary significantly by country and region due to differences in regulatory pricing controls, market access, and the competitive intensity of the local generic market. Markets with strong price controls (e.g., some European countries) will likely see flatter or declining prices, while less regulated markets might experience more variability.

Key Factors Influencing Future Prices:

- Generic Manufacturer Consolidation: Consolidation among generic manufacturers could potentially reduce competition, leading to slower price declines or even minor price stabilization in specific instances. However, the sheer number of existing players makes this scenario less probable for immediate impact.

- Manufacturing Efficiency Gains: Ongoing efforts to optimize API sourcing and manufacturing processes by generic companies could allow them to maintain profitability even at lower price points, facilitating further price competition.

- Payer Strategies: Payers will continue to leverage their purchasing power to drive down drug costs. This includes pushing for generics, negotiating aggressive rebates, and implementing utilization management programs.

- Generic Erosion Rate: The rate of price erosion is expected to slow from the dramatic drops seen immediately after patent expiry, as the market reaches a more mature competitive state. However, it will not cease entirely.

Projected Average Selling Price (ASP) Range (2028):

- Generic Carbidopa-Levodopa-Entacapone: $0.40 to $1.20 per tablet.

- Stalevo (branded): Likely to remain in a higher tier, but with significant discounts negotiated. Its effective price will likely be closer to the higher end of the generic range or slightly above, depending on payer agreements.

The market is expected to remain highly price-sensitive, with volume growth largely offsetting the moderate price declines.

What are the Key Market Drivers and Restraints?

The carbidopa-levodopa-entacapone market operates under a specific set of economic and therapeutic forces.

Market Drivers:

- Increasing Prevalence of Parkinson's Disease:

- Aging Global Population: The demographic shift towards older populations in developed and developing countries directly correlates with a higher incidence of neurodegenerative diseases like Parkinson's.

- Improved Diagnosis Rates: Greater awareness and advancements in diagnostic capabilities lead to earlier and more accurate identification of PD cases.

- Therapeutic Efficacy of Combination Therapy:

- Motor Fluctuations Management: Carbidopa-levodopa-entacapone is highly effective in managing the "wearing-off" phenomenon experienced by many Parkinson's patients on simpler levodopa regimens, leading to more consistent symptom control.

- Reduced "On-Off" Time: Entacapone, by inhibiting COMT, prolongs the action of levodopa, reducing the time patients spend in the "off" state where symptoms are more pronounced.

- Generic Accessibility and Affordability:

- Cost-Effectiveness: The availability of low-cost generic versions makes this essential therapy accessible to a broader patient population, driving prescription volumes.

- Payer Preference: Insurers and government health programs strongly favor generic medications to manage healthcare expenditures.

- Established Treatment Paradigm:

- Physician Familiarity: Clinicians are well-acquainted with the benefits and use of carbidopa-levodopa-entacapone as a standard treatment option for moderate to advanced Parkinson's disease.

- Patient Adherence: Fixed-dose combinations can improve patient adherence by reducing the pill burden.

Market Restraints:

- Intense Generic Competition and Price Erosion:

- Margin Compression: The highly competitive generic market leads to significant price reductions, squeezing profit margins for manufacturers.

- Limited Pricing Power: Innovator brands lose their ability to set premium prices once generics enter.

- Development of Alternative Therapies:

- New Drug Classes: Ongoing research into novel Parkinson's treatments (e.g., disease-modifying therapies, advanced delivery systems for dopamine agonists, gene therapies) could eventually offer alternatives that may reduce the reliance on existing levodopa-based combinations for certain patient segments.

- Advanced Device-Based Therapies: Deep brain stimulation (DBS) and focused ultrasound are options for advanced PD that may reduce the need for pharmacological adjustments in some individuals.

- Side Effect Profile:

- Levodopa-Related Side Effects: While improved by entacapone, carbidopa-levodopa-entacapone is still associated with levodopa-related side effects such as dyskinesias, nausea, and orthostatic hypotension, which can limit its use or necessitate dose adjustments.

- Entacapone-Specific Side Effects: Entacapone itself can cause side effects like gastrointestinal disturbances and urine discoloration.

- Regulatory Hurdles and Generic Approval Timelines:

- Complex Approval Pathways: While established, the process for generic drug approval can still involve lengthy review times and bioequivalence studies.

- Potential for Supply Chain Disruptions: Reliance on global supply chains for APIs can expose the market to disruptions affecting availability and, consequently, pricing.

What are the Key Competitive Strategies for Manufacturers?

In the mature and highly competitive carbidopa-levodopa-entacapone market, manufacturers employ various strategies to maintain or gain market share.

Key Competitive Strategies:

- Cost Leadership:

- API Sourcing: Securing reliable and cost-effective sources of carbidopa, levodopa, and entacapone APIs is paramount. This often involves backward integration or long-term contracts with API suppliers.

- Manufacturing Efficiency: Optimizing production processes, reducing waste, and achieving economies of scale in tablet manufacturing are critical to lowering the cost of goods sold.

- Supply Chain Optimization: Efficient logistics and distribution networks minimize costs and ensure timely delivery to market.

- Market Access and Payer Negotiations:

- Securing Formulary Placement: Generic manufacturers actively engage with pharmacy benefit managers (PBMs) and payers to secure preferred status on formularies, which directly influences prescription volume.

- Rebate and Discount Structures: Offering competitive rebate programs and volume-based discounts is standard practice to incentivize payers and distributors.

- Product Portfolio Diversification (within generics):

- Multiple Dosage Strengths and Formulations: Offering a full range of available dosage strengths ensures broad market coverage. While the core formulation is established, minor variations in excipients or tablet characteristics are generally not patentable differentiators in the generic space.

- Packaging Options: Providing various pack sizes and configurations to meet different market demands (e.g., hospital bulk packs, retail blister packs).

- Quality and Reliability:

- Consistent Supply: Ensuring a stable and consistent supply of the drug is crucial, as any stock-outs can lead to patients switching to competitors.

- Regulatory Compliance: Maintaining high standards of Good Manufacturing Practice (GMP) and strict adherence to regulatory requirements in all target markets.

- Targeted Market Entry and Geographic Expansion:

- First-to-File (FTF) Strategy: For new generics, being the first to file an Abbreviated New Drug Application (ANDA) in the U.S. can confer a 180-day period of market exclusivity, a significant competitive advantage.

- International Market Penetration: Developing strategies for obtaining regulatory approvals and establishing distribution channels in key global markets beyond the U.S. and Europe.

- Customer Service and Support:

- Physician and Pharmacist Education: Providing information on product availability and generic substitution options.

- Patient Assistance Programs: While less common for generics, some manufacturers may offer limited support programs.

For established generics, the primary strategic battleground is price and reliable supply. Differentiated strategies are more challenging given the mature nature of the drug and its fixed-dose combination.

Key Takeaways

The carbidopa-levodopa-entacapone market is a well-established segment of Parkinson's disease treatment. Patent expiries have led to a highly competitive generic landscape, driving significant price erosion from the innovator brand's peak. Future growth is underpinned by increasing PD prevalence, while market dynamics will be dominated by price competition among generic manufacturers, payer negotiations, and the continuous drive for cost efficiency. Innovations are unlikely to significantly disrupt the established combination therapy in the near term, meaning the market will remain characterized by high volume and low per-unit pricing.

Frequently Asked Questions

- What is the primary reason for the price difference between branded Stalevo and generic carbidopa-levodopa-entacapone? The primary reason is the expiration of patent protection for Stalevo, which allowed multiple generic manufacturers to enter the market, creating intense price competition.

- Will there be significant advancements in carbidopa-levodopa-entacapone formulations in the near future? Given the mature nature of this fixed-dose combination and its established therapeutic role, major advancements in formulation are unlikely to emerge in the short to medium term. Focus remains on cost-effective generic production.

- How do government regulations impact the pricing of carbidopa-levodopa-entacapone? Government regulations, such as price controls, mandatory generic substitution laws, and reimbursement policies, exert downward pressure on pricing by favoring generics and limiting the pricing power of branded products.

- What is the typical process for a generic manufacturer to bring carbidopa-levodopa-entacapone to market after patent expiry? Generic manufacturers must demonstrate bioequivalence to the reference listed drug (Stalevo) through an Abbreviated New Drug Application (ANDA) with regulatory agencies like the FDA. This involves conducting bioequivalence studies and submitting detailed manufacturing information.

- How does the market for carbidopa-levodopa-entacapone differ from other Parkinson's disease treatments in terms of market maturity and competition? Compared to newer classes of Parkinson's drugs or investigational therapies, carbidopa-levodopa-entacapone is in a highly mature phase. Its market is characterized by widespread generic availability and intense price-based competition, unlike emerging therapies that may still be under patent protection or targeting specific patient niches.

Citations

[1] National Institute of Neurological Disorders and Stroke. (n.d.). Parkinson's Disease: Hope Through Research. Retrieved from https://www.ninds.nih.gov/health-information/disorders/parkinsons-disease

More… ↓