Share This Page

Drug Price Trends for CAPSAICIN

✉ Email this page to a colleague

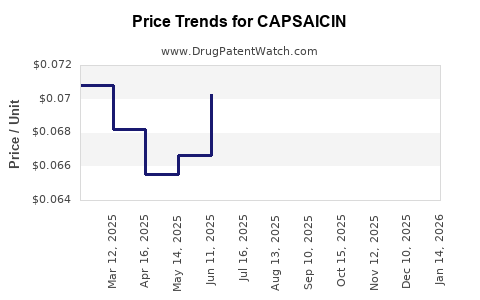

Average Pharmacy Cost for CAPSAICIN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| CAPSAICIN 0.025% CREAM | 00536-2525-25 | 0.08215 | GM | 2026-07-22 |

| CAPSAICIN 0.025% CREAM | 50268-0195-60 | 0.08215 | GM | 2026-07-22 |

| CAPSAICIN 0.1% CREAM | 70000-0549-01 | 0.20119 | GM | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for CAPSAICIN

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| CAPZIX HP 0.1% CREAM,TOP | TOPRAIL CHP, LLC | 72847-0316-20 | 56.6GM | 6.98 | 0.12332 | GM | 2023-10-01 - 2028-09-30 | FSS |

| CAPSAICIN 0.025% CREAM,TOP | AvKare, LLC | 50268-0195-60 | 60GM | 2.22 | 0.03700 | GM | 2023-06-15 - 2028-06-14 | FSS |

| CAPSAICIN 0.075% CREAM,TOP | AvKare, LLC | 50268-0196-57 | 57GM | 3.32 | 0.05825 | GM | 2023-06-15 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Capsaicin Drug Market Analysis and Price Projections

Capsaicin, the active compound in chili peppers, demonstrates significant therapeutic potential across various medical indications, driving market growth. Current market size is estimated at USD 3.8 billion in 2023, with projected growth to USD 6.2 billion by 2030, representing a compound annual growth rate (CAGR) of 7.3% [1, 2]. This expansion is fueled by increasing prevalence of chronic pain conditions, including neuropathic pain and osteoarthritis, and a growing demand for non-opioid pain management alternatives [3, 4]. Regulatory approvals for new capsaicin-based formulations and advancements in drug delivery systems are further contributing to market dynamics [5].

What are the key therapeutic applications driving capsaicin market growth?

The market for capsaicin as a therapeutic agent is primarily driven by its efficacy in managing chronic pain conditions. Its mechanism of action involves desensitizing sensory neurons, thereby reducing pain signals [6].

- Neuropathic Pain: This is a significant driver, encompassing conditions like diabetic peripheral neuropathy, postherpetic neuralgia (shingles pain), and chemotherapy-induced peripheral neuropathy [7, 8]. The market for neuropathic pain management is substantial, and capsaicin offers a localized, targeted treatment option.

- Osteoarthritis (OA): Topical capsaicin formulations are widely used for the symptomatic relief of OA pain, particularly in the knee and hand [9]. The aging global population and the increasing incidence of OA contribute to sustained demand.

- Other Pain Management: Capsaicin is also explored for other pain indications, including musculoskeletal pain, lower back pain, and post-surgical pain [10]. Its application in combination therapies is also an area of research and development.

- Non-Pain Applications: Emerging research indicates potential for capsaicin in areas beyond pain, such as weight management, cardiovascular health, and even certain dermatological conditions, although these are currently less significant market drivers [11].

What are the leading capsaicin-based drugs and their market penetration?

The market features a range of capsaicin-based drugs, primarily in topical and transdermal forms, with varying concentrations and delivery mechanisms.

- High-Concentration Topical Formulations: These are often prescription-based and are effective for localized pain. Examples include:

- Qutenza (capsaicin 8% patch): Approved for neuropathic pain, it is a significant product with established market presence [12]. Its high concentration and localized application differentiate it.

- Zostrix (capsaicin 0.075% cream): An over-the-counter (OTC) option for mild to moderate pain relief, it has broad accessibility [13].

- Low-Concentration Topical Formulations: Widely available OTC for everyday pain relief, these products have high volume sales. They include creams, lotions, and patches with capsaicin concentrations typically below 0.1% [14].

- Patches: Transdermal patches offer controlled release and prolonged efficacy, making them popular for chronic pain management. The 8% capsaicin patch (Qutenza) is a prime example in the prescription segment.

- Combination Products: Some products combine capsaicin with other analgesics or counterirritants to enhance pain relief, though these are less common as standalone capsaicin-specific offerings [15].

Market penetration varies by region and regulatory status. Developed markets in North America and Europe exhibit higher penetration due to established healthcare infrastructure and physician adoption of advanced pain management therapies. Emerging markets show growing potential as awareness and access increase.

What are the projected price trends for capsaicin-based drugs?

Price projections for capsaicin-based drugs are influenced by several factors, including drug concentration, formulation, dosage form, indication, and market competition.

- High-Concentration Prescription Drugs: These typically command higher prices due to specialized formulations, clinical development costs, and targeted indications. For example, the 8% capsaicin patch (Qutenza) is a premium product. Projected price increases for such specialized treatments are expected to be moderate, ranging from 3% to 6% annually, driven by inflation, ongoing clinical support, and market demand for effective neuropathic pain solutions [16].

- Over-the-Counter (OTC) Topical Formulations: These products, available in lower concentrations, face more price sensitivity due to competition and the availability of generic alternatives. Price increases are likely to be more modest, in the range of 2% to 4% annually, primarily aligned with general consumer price inflation [17].

- Impact of New Formulations and Delivery Systems: The development of novel delivery systems, such as longer-acting patches or more patient-friendly topical applications, could lead to premium pricing for these advanced products. Conversely, the introduction of generic versions of existing capsaicin drugs will exert downward pressure on prices for those specific products [18].

- Geographic Variations: Pricing will continue to vary significantly by region due to differences in healthcare reimbursement policies, economic conditions, and local market dynamics. Prices in North America and Western Europe are generally higher than in Asia or Latin America.

Overall, while high-concentration, prescription-grade capsaicin therapies are expected to maintain premium pricing, the broader market for lower-concentration OTC products will likely experience more stable, inflation-linked price adjustments.

What is the competitive landscape for capsaicin drug manufacturers?

The competitive landscape for capsaicin drug manufacturers is characterized by a mix of established pharmaceutical companies, specialty drug developers, and generic manufacturers.

- Key Players:

- Aurovitas Pharmaceutical: Involved in the development and marketing of generic and branded pharmaceuticals, including pain management products.

- Depomed, Inc. (now bundled within Amneal Pharmaceuticals): Previously a significant player with capsaicin-based products for pain management.

- Haleon plc: A consumer healthcare company with a portfolio that includes OTC pain relief products where capsaicin may be an ingredient.

- Mallinckrodt Pharmaceuticals: Offers various pain management solutions, potentially including capsaicin derivatives or related compounds.

- Paladin Labs Inc. (now part of Endo International plc): Has been involved in distributing pain management therapies.

- Salix Pharmaceuticals (part of Bausch Health Companies): Known for gastrointestinal and other specialized therapies, with potential for pain management product lines.

- Teva Pharmaceutical Industries Ltd.: A major global pharmaceutical company with a broad generic portfolio and branded products, likely including capsaicin-based treatments.

- Market Dynamics:

- Generic Competition: The market for lower-concentration OTC capsaicin products is highly competitive, with numerous generic manufacturers offering similar formulations, leading to price erosion.

- Branded Product Differentiation: Companies with high-concentration prescription products, such as those for neuropathic pain, focus on clinical efficacy, specialized delivery, and physician education to maintain market share and pricing power.

- R&D Investment: Ongoing research into novel delivery systems, improved formulations, and new indications for capsaicin drives innovation and creates opportunities for market differentiation. This includes exploring lower-irritancy formulations and longer-acting options [19].

- Strategic Partnerships and Acquisitions: Mergers, acquisitions, and licensing agreements are common in the pharmaceutical industry and impact the competitive positioning of capsaicin drug manufacturers. For example, the consolidation of companies can lead to a more concentrated market for certain therapeutic areas [20].

- Regulatory Landscape: Approval pathways and post-market surveillance by regulatory bodies like the FDA and EMA influence market entry and product lifecycle management for capsaicin-based drugs.

What are the regulatory considerations and patent landscape for capsaicin drugs?

The regulatory and patent landscape significantly shapes the market for capsaicin drugs.

- Regulatory Approvals:

- Indications: Capsaicin drugs require specific regulatory approval for each intended medical indication. For instance, a capsaicin patch approved for postherpetic neuralgia may not be automatically approved for osteoarthritis without separate clinical trials and submissions [21].

- Formulation and Concentration: Regulatory agencies scrutinize the safety and efficacy of different capsaicin concentrations and formulations. High-concentration products (e.g., 8% patch) undergo rigorous review for potential adverse events like skin irritation or burns [22].

- Manufacturing Standards: Compliance with Good Manufacturing Practices (GMP) is mandatory for all pharmaceutical products, including capsaicin-based drugs.

- OTC vs. Prescription: The classification of a capsaicin product as OTC or prescription-only is determined by its indication, strength, and safety profile. This classification impacts market access and distribution channels [23].

- Patent Landscape:

- Composition of Matter Patents: While capsaicin itself is a naturally occurring compound and not patentable, patents can be obtained for novel synthetic forms, specific crystalline structures, or unique combinations of capsaicin with other active ingredients.

- Formulation Patents: Patents frequently cover specific formulations that improve stability, solubility, delivery, or reduce side effects. This includes controlled-release formulations, specialized topical bases, or novel delivery devices like unique patch designs [24].

- Method of Use Patents: These patents protect specific therapeutic applications of capsaicin for particular medical conditions. For example, a patent might cover the use of a specific capsaicin concentration to treat diabetic neuropathy.

- Patent Expiry: The expiry of key patents for branded capsaicin drugs opens the door for generic competition. Manufacturers of generic capsaicin products must demonstrate bioequivalence and meet regulatory requirements [25].

- Life Cycle Management: Pharmaceutical companies often employ strategies such as developing new formulations or seeking new indications for existing drugs to extend patent protection and maintain market exclusivity.

- Intellectual Property Challenges: The patent landscape can be complex, with potential for litigation regarding infringement and patent validity. Navigating this landscape is crucial for R&D investment and market entry decisions.

Key Takeaways

The capsaicin drug market is poised for sustained growth driven by the increasing demand for effective pain management solutions, particularly for neuropathic pain and osteoarthritis. High-concentration, prescription-based formulations are expected to command premium pricing and maintain market leadership in specific indications. Over-the-counter products will continue to see stable, inflation-driven price adjustments. The competitive landscape is diverse, with opportunities for both branded innovators and generic manufacturers. Regulatory approvals and the patent landscape are critical determinants of market entry, product lifecycle, and pricing strategies.

FAQs

-

What is the typical concentration range for over-the-counter capsaicin topical products? Over-the-counter capsaicin topical products typically contain concentrations ranging from 0.025% to 0.075% [14].

-

Which specific neuropathic pain conditions are most commonly treated with prescription capsaicin drugs? Prescription capsaicin drugs, such as high-concentration patches, are most commonly used to treat postherpetic neuralgia (shingles pain) and chemotherapy-induced peripheral neuropathy [7, 8].

-

How does the mechanism of action of capsaicin contribute to pain relief? Capsaicin desensitizes sensory neurons by activating and subsequently depleting substance P, a neurotransmitter involved in pain signaling [6].

-

What are the primary challenges associated with the use of high-concentration capsaicin formulations? The primary challenges include potential skin irritation, burning sensations, and the need for professional application or administration by a healthcare provider [22].

-

Can new patents be obtained for capsaicin itself, or only for its applications and formulations? New patents cannot be obtained for capsaicin itself as it is a naturally occurring compound. Patents can, however, be secured for novel formulations, specific delivery systems, synthetic derivatives, or new methods of using capsaicin for therapeutic purposes [24].

Citations

[1] Grand View Research. (2023). Capsaicin Market Size, Share & Trends Analysis Report. [2] Market Research Future. (2023). Capsaicin Market Research Report. [3] National Institute of Neurological Disorders and Stroke. (n.d.). Neuropathic Pain Information Page. [4] Arthritis Foundation. (n.d.). Osteoarthritis. [5] U.S. Food and Drug Administration. (n.d.). Drug Development Process. [6] Research Gate. (2019). Capsaicin and Pain Relief: A Mechanistic Review. [7] Treede, R. D., & K K. (2017). Neuropathic pain: diagnosis and treatment. Deutsches Arzteblatt International, 114(17), 291–296. [8] National Cancer Institute. (n.d.). Peripheral Neuropathy Treatment (PDQ®)–Health Professional Version. [9] McAlindon, T. E., & Bannuru, R. R. (2017). Osteoarthritis treatment: current and future therapeutic options. Rheumatic Disease Clinics of North America, 43(3), 387-400. [10] American Academy of Pain Medicine. (n.d.). Conditions Treated. [11] Pellati, F., & Brighenti, L. (2021). Capsaicin and its Health Benefits: A Review of Recent Evidence. Journal of Functional Foods, 85, 104635. [12] FDA. (2009). FDA Approves Qutenza™ (capsaicin) 8% patch for the management of postherpetic neuralgia. Press Release. [13] Zostrix. (n.d.). Product Information. [14] Consumer Healthcare Products Association. (n.d.). Categories of OTC Medicines. [15] PubMed. (2020). Combination Therapies for Pain Management. [16] Statista. (2023). Pharmaceuticals market in the U.S. - statistics & facts. [17] Deloitte. (2023). The future of the pharmaceutical industry. [18] Fierce Pharma. (2022). Generics market faces continued pressure. [19] The Pharmaceutical Journal. (2021). Innovations in pain management. [20] McKinsey & Company. (2022). The future of pharma: Investing for growth. [21] European Medicines Agency. (n.d.). Medicines. [22] PubChem. (n.d.). Capsaicin. [23] U.S. Food and Drug Administration. (n.d.). Over-the-Counter (OTC) Drugs. [24] World Intellectual Property Organization. (n.d.). Patents. [25] U.S. Food and Drug Administration. (n.d.). Generics.

More… ↓