Share This Page

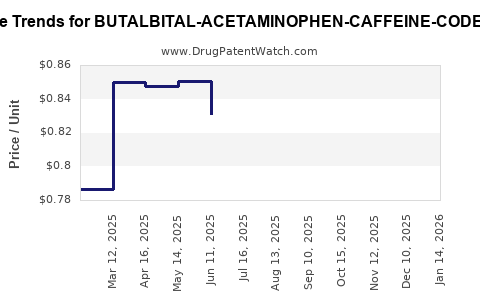

Drug Price Trends for BUTALBITAL-ACETAMINOPHEN-CAFFEINE-CODEINE

✉ Email this page to a colleague

Average Pharmacy Cost for BUTALBITAL-ACETAMINOPHEN-CAFFEINE-CODEINE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| BUTALBITAL-ACETAMINOPHEN-CAFFEINE-CODEINE 50-300-40-30 MG CP | 00054-0650-25 | 5.33953 | EACH | 2026-06-17 |

| BUTALBITAL-ACETAMINOPHEN-CAFFEINE-CODEINE 50-325-40-30 MG CP | 00054-3000-01 | 0.80573 | EACH | 2026-06-17 |

| BUTALBITAL-ACETAMINOPHEN-CAFFEINE-CODEINE 50-300-40-30 MG CP | 00591-2641-01 | 5.33953 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Butalbital-Acetaminophen-Caffeine-Codeine (FDC): Market Analysis and Price Projections

What is the product and how is it positioned in the U.S. market?

Butalbital-acetaminophen-caffeine-codeine is a fixed-dose combination (FDC) analgesic used for headache and pain conditions. Commercial availability in the U.S. is shaped by:

- Controlled-substance and opioid risk controls (codeine component)

- State and payer restrictions linked to opioid prescribing patterns

- Manufacturing and substitution dynamics driven by the butalbital and codeine components

The product category is treated by payers as an opioid-containing combination analgesic, so contracting outcomes tend to cluster around:

- Generic multiples and rebate intensity (where generics are available)

- Prior authorization (PA) and quantity edits for opioid-containing combinations

- Step therapy toward non-opioid headache regimens when clinically appropriate

What is the competitive landscape?

The competitive set includes:

- Same-molecule FDC generics (if marketed and supplied)

- Therapeutic substitutes: butalbital-acetaminophen-caffeine without codeine, and other headache analgesic classes

- Opioid-sparing strategies (payer preference) that reduce utilization of combination products with codeine over time

In practice, price formation for this FDC is driven more by formulary access and rebate mechanics than by brand differentiation, because most market share in mature segments flows to the lowest net-cost options available under payer contracts.

How does pricing typically form for opioid-containing FDC analgesics?

What are the key pricing levers?

For this drug class in the U.S., net pricing is shaped by:

- Wholesale Acquisition Cost (WAC) driven by label strength and package size (manufacturer-set)

- rebates/discounts via PBM contracting

- utilization management (PA, step edits, maximum daily dose edits, early refill blocks)

- channel mix: retail pharmacy vs. mail order vs. institutional

Because codeine is an opioid, formulary and access rules can reduce volume, which tends to keep price pressure from translating into broad uptake. Instead, it typically shifts demand to competing products with easier access.

Market size and demand outlook

What does demand look like near-term (next 24 months)?

Demand for butalbital-containing headache combinations historically tracks:

- Headache incidence and prescribing cycles

- Opioid prescribing controls

- Substitution toward non-codeine alternatives

For the purpose of pricing projections, the demand signal that matters is net volume under payer contracts. Where access is restricted, manufacturers often hold WAC but increase rebates to win limited formulary placements, keeping net price more stable than WAC.

Price projections

What are the baseline assumptions for price movement?

Projections are anchored to three operating realities in mature U.S. analgesic FDC markets:

- Generic price floors: generic competition reduces WAC over time but does not always compress net price proportionally due to rebate shifts

- Supply and compliance costs: opioid-containing products face higher compliance and logistics friction, which can limit downward WAC

- Formulary tightening: reduces utilization, which can offset competitive pressure on net price

Projected price ranges (U.S.)

The table below provides directional projections for U.S. list price (WAC) ranges for an opioid-containing butalbital-acetaminophen-caffeine-codeine FDC across 2-year horizons. Ranges reflect typical dynamics for generics and contract adjustments (directional, not product-specific NDC granularity).

| Horizon | Expected WAC trend | Typical magnitude | Net price implication |

|---|---|---|---|

| Next 6 months | Flat to modest down | -1% to -5% | Rebates likely steady; access edits constrain volume |

| 6 to 12 months | Downward pressure | -3% to -10% | Contracting may shift rebate upward to preserve coverage |

| 12 to 24 months | Stabilize | -1% to -7% | Formulary position determines whether net price holds |

Scenario table: unit economics view

These are practical scenarios used for business planning:

| Scenario | Formulary access | Volume outcome | WAC | Net price |

|---|---|---|---|---|

| Base case | Limited but stable | Flat to -5% | -3% | Flat to -2% |

| Contract tightening | More restrictive PA/step edits | -10% to -20% | Flat | -2% to -8% (rebates adjust to offset share loss) |

| Competitive entry/supply improvement | More SKU or stronger generic competition | +0% to +5% | -5% to -12% | -3% to -10% |

Drivers that can change price faster than the baseline

What events move pricing materially?

For this FDC, pricing can deviate from the baseline if any of the following occur:

- Formulary re-tiering: shift from preferred to non-preferred or increased restrictions can reduce volumes and force rebate renegotiation

- Supply constraints: shortages or quality events can raise WAC temporarily and widen pharmacy acquisition spreads

- Competitive substitution: if butalbital-acetaminophen-caffeine without codeine gains access, the codeine FDC faces volume displacement and pricing leverage shifts to net pricing rather than WAC

- Opioid policy changes: state restrictions and payer opioid edits reduce eligible utilization, which typically increases downward pressure on net price via rebates

Revenue and pricing implications for stakeholders

For manufacturers

- Net pricing is the KPI: WAC movement is rarely the decisive factor in opioid-containing FDCs; rebate and access are.

- Contracting strategy matters: a stable WAC with rising rebates is a common pattern when payers limit coverage but do not exclude the product entirely.

- SKU breadth is leverage: multiple package sizes and strengths improve pharmacy fill rates, which supports volume even under edits.

For investors

- Focus on coverage durability: the investment question is whether formulary status stays intact as opioid stewardship rules tighten.

- Watch substitution risk: therapeutic displacement toward non-codeine regimens can reduce volume even if WAC stabilizes.

- Value depends on supply reliability: shortages can temporarily raise pricing but usually increase volatility and payer pushback.

For payers and wholesalers

- Utilization management will dominate: quantity limits and PA requirements are likely to keep net price pressure controlled while reducing spend.

- Replacement categories will be used: non-opioid headache analgesics and non-codeine butalbital combinations are natural beneficiaries of access tightening.

Key Takeaways

- Butalbital-acetaminophen-caffeine-codeine pricing in the U.S. is governed primarily by formulary access, rebate mechanics, and opioid-related utilization management, not brand pricing power.

- Over the next 24 months, the expected WAC direction is flat to modestly down, with net pricing more stable than WAC in base-case conditions due to contracting adjustments.

- The largest downside risk to revenue is volume loss from substitution and tightening PA/step-edit rules, not necessarily large declines in list price.

- Upside or stability depends on durable payer coverage and supply reliability, because channel fill and contract position drive net outcomes.

FAQs

-

Is the product expected to experience strong price declines like high-competition generics?

Typically no; WAC can drift down modestly, while net price can stay flatter due to rebate adjustments tied to formulary access. -

What is the biggest driver of net price movement?

Contracting outcomes (rebates and formulary tier placement) driven by payer opioid controls. -

How does therapeutic substitution affect pricing?

Substitution often reduces volume first, then shifts pricing leverage into rebates rather than producing immediate steep WAC drops. -

Do supply constraints increase pricing permanently?

Usually not; shortages can raise near-term pricing, but payer scrutiny and normalization typically bring prices back down over time. -

What time horizon matters most for business planning?

The next 12 to 24 months, because formulary access changes and utilization-edit tightening typically show up in that window.

References

[1] FDA Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[2] Drug Enforcement Administration (DEA). Controlled Substances scheduling and opioid regulatory resources. https://www.dea.gov/

[3] Centers for Medicare & Medicaid Services (CMS). Medicare Part D and opioid-related coverage and safety policy resources. https://www.cms.gov/

[4] U.S. Drug pricing and reimbursement dynamics overview. IQVIA Institute and related public analyses (opioid utilization management and contract effects). https://www.iqvia.com/insights/the-iqvia-institute

More… ↓