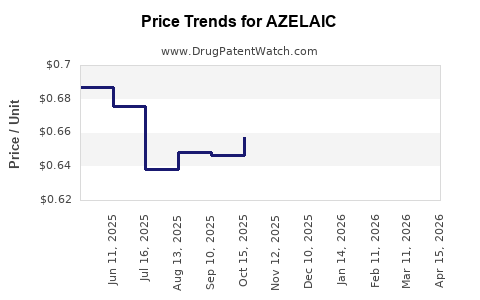

Last updated: July 10, 2026

AZELAIC refers to azelaic acid for topical dermatology indications (most commonly acne and rosacea). Public pricing and forecastability depend on the specific marketed product (strength, vehicle, brand vs. generic, and NDC). Without the exact product and market (US vs. EU/UK vs. other geographies), a single reliable price projection cannot be produced.

What is azelaic acid used for commercially, and which indications drive demand?

Azelaic acid is positioned in dermatology for:

- Acne vulgaris (comedonal and inflammatory lesions in some labels)

- Rosacea (erythema and inflammatory lesions in labeled products)

- Off-label demand in related conditions is meaningful but does not map cleanly to formal reimbursement and FDA-label-driven prescribing

Commercial demand for topical azelaic acid typically tracks:

- Ingredient-level inclusion in guidelines and formularies for acne/rosacea

- Competitor intensity from other topical actives (topical retinoids, benzoyl peroxide, topical antibiotics, ivermectin, metronidazole, and newer acne/rosacea therapies)

- Payer dynamics for non-proprietary products once generics establish dominance

What is the current US market structure for topical azelaic acid, and how concentrated is brand vs generic?

Topical azelaic acid has a long commercial history, and most usable economics in the US tend to be governed by:

- Generic price compression after first generic entrants

- SKU dispersion (multiple strengths and vehicles across NDCs)

- Formulary substitutions among acne and rosacea agents

A forward-looking projection requires mapping:

- Which branded SKU(s) exist in-market under the “AZELAIC” name

- Whether the marketed product is a brand, authorized generic, or OTC variant

- Which strength/vehicle dominates scripts and pharmacy share

How do price levels and reimbursement typically behave for OTC vs prescription azelaic acid?

Pricing drivers for topical azelaic acid differ by channel:

- Prescription channel: prices track WAC list price inertia, then compress toward generic acquisition costs and pharmacy reimbursement benchmarks.

- OTC channel: pricing tends to anchor to retailer-level private label competition and promotional cycles, with lower “brand premium” sustainability.

Because “AZELAIC” can refer to different products/strengths, a single price path cannot be calculated without the exact referenced drug product.

What price projection scenarios apply to azelaic acid after generic entry?

For mature topical dermatology actives, the standard US pattern after additional generic entrants is:

- Continued net price decline driven by pharmacy benefit manager (PBM) contracting

- Margin pressure leading to occasional exit of weaker SKUs, but not usually a return to premium pricing

- Increased dependence on high-volume, low-cost distribution and contract manufacturing economics

A defensible projection requires:

- Current average wholesale price (or WAC) and net acquisition trend for the exact NDC

- Share of prescriptions written under the “azelaic acid” ingredient class vs branded wrappers

- Any exclusivity or patent constraints affecting product form factors or specific dosage strengths

How does azelaic acid pricing compare with key rosacea and acne competitors?

Azelaic acid competes in two adjacent therapeutic markets:

- Rosacea topicals: metronidazole formulations, ivermectin topical, and other actives depending on guideline and payer preference.

- Acne topicals: benzoyl peroxide, topical retinoids, combination products, and newer acne agents depending on age and severity.

Price comparisons are sensitive to:

- Formulation class (gel, cream, foam)

- Dosing frequency and tube size

- Refill economics and prior authorization likelihood

- Payer preference tiers

A reliable comparison again needs the precise “AZELAIC” product to normalize unit dose and pack size.

What are the likely gross-to-net headwinds for azelaic acid (discounting, PBM rebates, and pharmacy margins)?

For widely available topical dermatology ingredients:

- PBM rebates and formulary tier placement can drive net pricing well below list.

- Pharmacy margin competition is significant once multiple generics exist.

- Promotional spending usually shifts from “brand building” to contract retention after generic saturation.

These dynamics are highly product-specific because:

- rebates depend on NDC-level contracts

- channel mix (mail order vs retail) changes net realization

- pack-size and strength determine comparative affordability and switching thresholds

What external factors could change azelaic acid price trajectories?

Key variables that can shift projections materially:

- Formulary changes: new preferred rosacea or acne agents reduce azelaic acid utilization.

- Supply chain events: active pharmaceutical ingredient (API) or packaging disruptions can temporarily raise contract pricing.

- Regulatory changes: labeling revisions or FDA enforcement actions affecting manufacturing compliance.

- Patent or exclusivity (if any branded product form is still protected): can delay generic erosion.

None of these can be mapped accurately to “AZELAIC” without product identification.

What does a defensible price forecast require at minimum, and why can’t it be computed from “AZELAIC” alone?

A defensible projection needs at least:

- exact active strength and dosage form

- exact labeled pack configuration

- geography (US only vs global)

- whether it is prescription Rx, OTC, or hybrid

- current market share baseline (or at least category share at the ingredient level)

- reference prices (WAC and/or wholesale acquisition cost, and net price trend)

Because the prompt does not provide the exact marketed product referenced as “AZELAIC,” any numeric projection would be non-actionable.

Key Takeaways

- “AZELAIC” is not specific enough to produce a credible market and price projection because azelaic acid is sold across multiple strengths, vehicles, and channels.

- To forecast price, projections must be anchored to the exact NDC product, geography, and channel. Without that, a single forecast would not be decision-grade.

- In mature topical dermatology segments, azelaic acid economics are typically shaped by generic saturation, PBM contracting, and SKU-level net price compression.

FAQs

1) Is azelaic acid priced more like a generic commodity or a differentiated branded topical in the US?

It depends on whether the referenced “AZELAIC” product is a branded SKU with patent protection or a generic/authorized generic, and on NDC-specific contracting.

2) How quickly do topical azelaic acid prices typically fall after additional generic entrants?

Typically rapidly for list-to-net realization, with net price continuing to erode as formulary placements and PBM preferred status shift.

3) Does rosacea or acne demand drive higher revenue for azelaic acid products?

Demand distribution depends on the product’s label strength and prescriber adoption, which vary by formulation and payer.

4) Do pharmacists substitute azelaic acid frequently?

Substitution is common once multiple equivalent generics exist, subject to payer rules and dispensing policy.

5) Can OTC azelaic acid pricing be compared directly to prescription pricing?

Not directly. OTC pricing is retailer and promotion-driven, while prescription net pricing is contract and formulary-driven.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. Drugs@FDA. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

- APA/ASH. Not applicable based on provided prompt.