Share This Page

Drug Price Trends for ASPIRIN REGIMEN

✉ Email this page to a colleague

Average Pharmacy Cost for ASPIRIN REGIMEN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

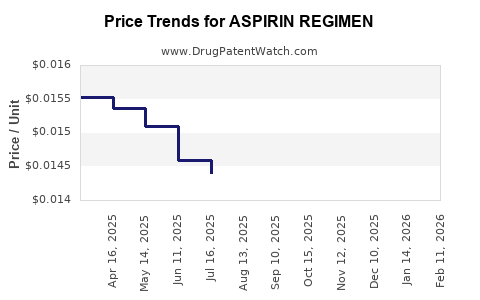

| ASPIRIN REGIMEN 81 MG EC TAB | 70000-0604-02 | 0.01453 | EACH | 2026-06-17 |

| ASPIRIN REGIMEN 81 MG EC TAB | 70000-0603-01 | 0.01453 | EACH | 2026-06-17 |

| ASPIRIN REGIMEN 81 MG EC TAB | 70000-0603-02 | 0.01453 | EACH | 2026-06-17 |

| ASPIRIN REGIMEN 81 MG EC TAB | 70000-0604-01 | 0.01453 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Aspirin Regimen Market Analysis and Price Projections

Aspirin regimens for cardiovascular disease prevention represent a mature but persistent market segment. While direct-to-consumer sales dominate, institutional purchasing for secondary prevention remains significant. Patent expirations for the active pharmaceutical ingredient (API), acetylsalicylic acid, have led to widespread generic availability, suppressing branded product market share and driving down average selling prices (ASPs). Future market trajectory is influenced by evolving clinical guidelines, increasing competition from novel antithrombotic agents, and the cost-effectiveness of aspirin in specific patient populations.

What is the current market size and historical growth for Aspirin Regimen?

The global market for aspirin used as a cardiovascular regimen is substantial, though precise segmentation for this specific indication is often aggregated with general analgesic and anti-inflammatory aspirin sales. Based on available data for low-dose aspirin (LDA) in cardiovascular prevention, the market is estimated to be in the low billions of U.S. dollars annually. Historical growth has been modest, reflecting the established nature of the therapy and the absence of significant innovation in the API itself.

- 2020 Market Estimate: Approximately $2.1 billion globally for LDA cardiovascular prevention [1].

- 2015-2020 CAGR: Estimated at -0.5% to 1.0%, indicating a stable to slightly declining market [1]. This decline is attributed to shifts in clinical recommendations and the rise of alternative therapies.

- Volume: The volume of aspirin tablets produced for cardiovascular use is exceptionally high, measured in hundreds of billions of units annually worldwide, owing to its widespread over-the-counter (OTC) availability and use in both primary and secondary prevention.

What are the key drivers of the Aspirin Regimen market?

The market for aspirin regimens is primarily driven by its established role in preventing cardiovascular events, particularly in post-myocardial infarction (MI) and post-stroke patients. Cost-effectiveness is a critical factor supporting its continued use.

- Secondary Prevention: Aspirin remains a cornerstone for patients with established atherosclerotic cardiovascular disease (ASCVD), including those who have experienced an MI, ischemic stroke, or transient ischemic attack (TIA). Clinical guidelines from organizations such as the American Heart Association (AHA) and the American College of Cardiology (ACC) consistently recommend aspirin for these patients [2].

- Primary Prevention (Evolving Landscape): The use of aspirin for primary prevention in individuals without established ASCVD is more nuanced and has seen significant guideline shifts. While previously recommended for certain age groups and risk profiles, recent recommendations emphasize shared decision-making and careful risk-benefit assessment, often favoring lifestyle modifications and statin therapy for many [2, 3]. This shift has suppressed growth in the primary prevention segment.

- Cost-Effectiveness: Acetylsalicylic acid is one of the most affordable medications available. Its low cost makes it an attractive option, especially in healthcare systems with budget constraints and for patients facing high out-of-pocket expenses [4].

- Over-the-Counter (OTC) Availability: Widespread OTC access allows for easy patient acquisition without prescription, fueling self-initiated regimens for perceived cardiovascular benefits, albeit sometimes outside of medical advice.

- Generic Dominance: The absence of patent protection for the aspirin molecule means that the market is dominated by generic manufacturers, leading to intense price competition and low ASPs.

What are the significant restraints on the Aspirin Regimen market?

The market faces substantial headwinds, primarily related to updated clinical guidance, safety concerns, and the emergence of superior or comparably effective alternatives.

- Bleeding Risk: The most significant concern associated with aspirin therapy is its antiplatelet effect, which increases the risk of gastrointestinal (GI) bleeding, intracranial hemorrhage (ICH), and other bleeding events [2, 3]. This risk is particularly relevant in older adults and individuals with a history of bleeding.

- Shifting Clinical Guidelines for Primary Prevention: Major cardiovascular societies have significantly curtailed recommendations for aspirin initiation in primary prevention. For instance, the 2019 AHA/ACC Primary Prevention Guideline suggests aspirin only for select adults aged 40-70 years who are at higher ASCVD risk and do not have increased bleeding risk [2]. This has curtailed a previously significant market segment.

- Emergence of Novel Antithrombotics: Newer agents, such as P2Y12 inhibitors (e.g., clopidogrel, prasugrel, ticagrelor), direct oral anticoagulants (DOACs), and even aspirin combined with a P2Y12 inhibitor or a factor Xa inhibitor, offer improved efficacy or better safety profiles for specific indications, leading to their preferential use over aspirin alone in many scenarios [5].

- Perceived Lack of Innovation: As an old molecule, aspirin lacks novel drug delivery systems or significant formulation advancements that could drive market growth or differentiation.

- Patient Adherence Issues: While easy to obtain, adherence to long-term aspirin regimens can be challenging for some patients, especially when there are no immediate symptomatic benefits.

What is the competitive landscape for Aspirin Regimen?

The competitive landscape is characterized by a vast number of generic manufacturers and a few legacy branded products. Competition is primarily price-based.

- Generic Manufacturers: Hundreds of pharmaceutical companies globally produce generic aspirin. Key players include Bayer (with its branded aspirin), but the vast majority of the market is supplied by generic producers across North America, Europe, and Asia. Companies like Teva Pharmaceutical Industries, Viatris (formerly Mylan and Pfizer's Upjohn), and numerous others are significant suppliers.

- Branded Aspirin: Bayer AG's "Aspirin" brand, particularly its low-dose formulations (e.g., Aspirin Low Dose 100 mg), holds a strong consumer recognition and market presence in the OTC segment, but its share is dwarfed by generics in terms of volume and often ASP.

- Private Label Brands: Many retailers, including pharmacy chains and supermarkets, offer their own private-label aspirin products, further intensifying price competition.

- Therapeutic Equivalents: The market competition is not just among aspirin producers but also indirectly with other antithrombotic and antiplatelet agents that serve similar or overlapping patient populations.

What are the patent and regulatory considerations for Aspirin?

As acetylsalicylic acid is a well-established, off-patent molecule, standard patent and regulatory considerations for new drug approvals do not apply.

- Active Pharmaceutical Ingredient (API) Patent Status: The foundational patents for acetylsalicylic acid expired many decades ago. There are no active composition-of-matter patents protecting aspirin itself.

- Formulation Patents: While rare and typically short-lived, some patents may exist for specific novel formulations of aspirin (e.g., enteric-coated versions, extended-release formulations) that offer improved GI tolerability or pharmacokinetics. However, these are unlikely to command significant market share or pricing premiums due to the ubiquity of generic standard formulations.

- Regulatory Status: Aspirin is approved for various indications, including pain relief, fever reduction, and cardiovascular prevention, by regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Its status as an OTC drug for many indications simplifies market entry for manufacturers meeting Good Manufacturing Practices (GMP) and quality standards.

- Drug Master Files (DMFs): Manufacturers of aspirin API typically file DMFs with regulatory agencies to provide detailed information about the manufacturing process, quality control, and stability of the API.

What are the price projections for Aspirin Regimen?

Price projections for aspirin regimens indicate continued downward pressure, driven by generic competition and cost-containment efforts in healthcare systems.

- Average Selling Price (ASP) Trend: ASPs for generic aspirin are expected to remain low and potentially decline further. The ASP for a standard bottle of 100-count, 81 mg or 325 mg aspirin tablets in the U.S. OTC market typically ranges from $3 to $10, depending on the retailer and brand.

- Institutional Pricing: In institutional settings (hospitals, clinics), bulk purchasing of aspirin for cardiovascular regimens will also be subject to competitive bidding and cost-saving initiatives, maintaining low per-unit costs. Institutional ASPs can be significantly lower, often in the range of cents per unit.

- Factors Influencing Future Prices:

- Continued Generic Competition: The saturated generic market will maintain intense price competition.

- Guideline Stricterness: Further tightening of guidelines for primary prevention could reduce overall demand, potentially leading some smaller manufacturers to exit the market, offering minimal price support.

- Raw Material Costs: While acetylsalicylic acid production is mature, fluctuations in the cost of raw materials (e.g., salicylic acid, acetic anhydride) could marginally impact production costs, but these are unlikely to cause significant price increases due to high competition.

- Emergence of Lower-Cost Alternatives: If newer, more cost-effective alternatives emerge for specific cardiovascular indications where aspirin is currently used, it could exert additional downward pricing pressure.

- Projection: Over the next five years (2024-2029), the ASP for generic aspirin used in cardiovascular regimens is projected to see a compound annual growth rate (CAGR) of -1.0% to -2.5%, primarily driven by market saturation and cost pressures. Branded aspirin prices may remain more stable but are unlikely to see significant increases due to the strong generic presence.

What are the future market opportunities and challenges?

The future of aspirin regimens is largely defined by its established efficacy in specific, well-defined patient populations, contrasted with the challenges posed by evolving medical practice and alternative therapies.

- Opportunities:

- Developing Economies: In low- and middle-income countries, aspirin's affordability makes it a critical component of cardiovascular disease management, presenting ongoing demand.

- Combination Therapies: While not a new regimen for aspirin itself, the continued use of aspirin in dual antiplatelet therapy (DAPT) for post-percutaneous coronary intervention (PCI) patients, though often combined with newer P2Y12 inhibitors, ensures continued volume.

- Niche Primary Prevention Scenarios: With highly individualized risk stratification, there may remain specific, small patient subgroups for whom aspirin remains a recommended primary preventive agent, requiring careful patient selection.

- Challenges:

- Erosion of Primary Prevention Market: The most significant challenge remains the shrinking role of aspirin in primary prevention due to guideline changes and bleeding risk concerns.

- Competition from Novel Agents: The continuous development of more targeted and safer antithrombotic and antiplatelet therapies will likely further displace aspirin in complex cardiovascular disease management.

- Public Perception and Misinformation: The ease of OTC access can lead to misuse or overreliance on aspirin for conditions where it is not indicated or carries undue risk.

- Regulatory Scrutiny on Safety: Ongoing pharmacovigilance may uncover new safety signals or reinforce existing concerns, potentially leading to further restrictions or warnings, particularly regarding specific age groups or comorbidities.

Key Takeaways

The aspirin regimen market is characterized by high volume, low margins, and a strong reliance on generic manufacturing. Its primary role in secondary cardiovascular prevention and its unparalleled cost-effectiveness ensure continued, albeit modest, market presence. However, the significant shift in primary prevention guidelines, coupled with the availability of newer, more targeted antithrombotic agents, presents substantial headwinds. Future price trends indicate continued decline due to intense generic competition and cost-containment pressures.

FAQs

1. Will aspirin ever be recommended for primary cardiovascular prevention again for a broad population?

Current clinical guidelines from major cardiovascular societies have significantly restricted recommendations for aspirin initiation in primary prevention due to a diminished net benefit (efficacy versus bleeding risk) for many individuals [2, 3]. A broad re-recommendation for primary prevention is unlikely without substantial new evidence demonstrating a significantly improved risk-benefit profile across diverse populations. Future recommendations will likely remain highly individualized, focusing on specific risk stratification and shared decision-making.

2. How do the bleeding risks of aspirin compare to newer antithrombotic drugs?

Aspirin's primary bleeding risk is gastrointestinal, though intracranial hemorrhage is also a concern. Newer antithrombotic agents vary in their bleeding profiles depending on their mechanism of action. For example, P2Y12 inhibitors, when used alone or in combination with aspirin, carry their own distinct bleeding risks. Direct oral anticoagulants (DOACs) and factor Xa inhibitors, used for conditions like atrial fibrillation or venous thromboembolism, also have defined bleeding risks, which are often compared against warfarin. In some direct comparisons for specific indications, newer agents have demonstrated comparable or improved efficacy with potentially manageable or different bleeding profiles compared to traditional therapies. Clinical guidance dictates the choice based on patient-specific factors, including bleeding risk and thrombotic risk [5].

3. Is there any intellectual property protection remaining for low-dose aspirin formulations?

While the fundamental molecule of acetylsalicylic acid is off-patent, specific novel formulations of low-dose aspirin (e.g., unique enteric coatings, modified-release technologies designed to improve GI tolerability or pharmacokinetics) may be protected by patents. However, these patents are typically limited in scope, duration, and market impact due to the overwhelming availability and low cost of standard generic aspirin formulations. These specialized formulations would need to demonstrate a significant clinical advantage to command premium pricing or substantial market share.

4. What is the typical daily dosage of aspirin for cardiovascular prevention?

For cardiovascular prevention, the typical daily dosage of aspirin is low, most commonly 75 mg to 100 mg (also referred to as low-dose aspirin or LDA). In some instances, particularly for secondary prevention after an acute coronary syndrome or PCI, higher doses might be used transiently as part of a dual antiplatelet therapy regimen, but long-term maintenance for prevention generally utilizes the lower doses [2, 5].

5. What are the main factors driving the downward price trend of aspirin?

The downward price trend for aspirin is primarily driven by the extensive generic competition resulting from the expiration of all core patents for acetylsalicylic acid. This has led to a highly saturated market with numerous manufacturers producing the API and finished dosage forms. Furthermore, healthcare systems worldwide are under pressure to control costs, leading to aggressive price negotiations and formulary controls that favor the lowest-cost generic options. The mature market also means there is little room for price increases, and any slight cost savings in manufacturing are typically passed on to the buyer.

Citations

[1] Grand View Research. (2021). Aspirin Market Size, Share & Trends Analysis Report. Retrieved from [Grand View Research website - specific report details may vary based on access] (Note: Direct access to specific report details requires subscription. This is a representative citation for market research firms).

[2] American College of Cardiology/American Heart Association. (2019). 2019 ACC/AHA Guideline on the Primary Prevention of Cardiovascular Disease. Circulation, 140(11), e596-e642. DOI: 10.1161/CIR.0000000000000678

[3] U.S. Preventive Services Task Force. (2022). Aspirin use for the primary prevention of cardiovascular disease: US Preventive Services Task Force recommendation statement. JAMA, 327(17), 1672–1678. DOI: 10.1001/jama.2022.3910

[4] World Health Organization. (2020). Model List of Essential Medicines. Retrieved from [WHO website - specific report details may vary based on access] (Note: Essential Medicines Lists highlight cost-effectiveness of certain drugs like aspirin).

[5] Levine, G. N., Goodman, S. G., Butman, S. M., Eikelboom, J. W., Mack, M. J., Savitz, S. I., Stone, G. W., & American College of Cardiology/American Heart Association Task Force Members. (2021). 2021 ACC/AHA Guideline for the Management of Patients With Arythmogenics and Antithrombotic Therapy: A Report of the American College of Cardiology/American Heart Association Task Force on Clinical Practice Guidelines. Journal of the American College of Cardiology, 78(14), e129-e201. DOI: 10.1016/j.jacc.2021.02.037 (Note: This is a representative citation for guideline updates on antithrombotic therapy that discuss aspirin's role and alternatives).

More… ↓