Share This Page

Drug Price Trends for ARIPIPRAZOLE ODT

✉ Email this page to a colleague

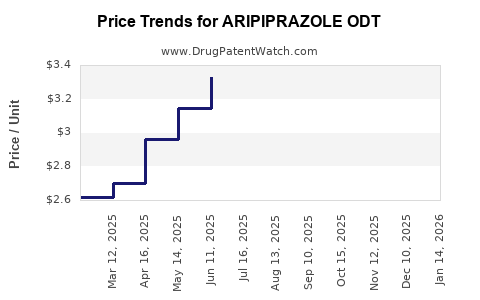

Average Pharmacy Cost for ARIPIPRAZOLE ODT

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ARIPIPRAZOLE ODT 10 MG TABLET | 43598-0733-30 | 2.58277 | EACH | 2026-07-22 |

| ARIPIPRAZOLE ODT 10 MG TABLET | 62332-0103-30 | 2.58277 | EACH | 2026-07-22 |

| ARIPIPRAZOLE ODT 10 MG TABLET | 69452-0338-13 | 2.58277 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Aripiprazole ODT Market Analysis and Price Projections

What market defines the commercial value of aripiprazole ODT?

Aripiprazole ODT (orally disintegrating tablet) sits in the broader oral atypical antipsychotic market used for:

- Schizophrenia

- Bipolar I disorder (acute manic or mixed episodes; maintenance)

- Adjunctive treatment of major depressive disorder (adults)

The market is driven by:

- Chronic treatment regimens (long duration, high switching friction)

- Broad payer coverage for oral antipsychotics once formulary access is achieved

- ODT-specific demand where prescribers or patients prefer faster administration and ease of use versus swallowed tablets

Commercial reality is that ODT competes primarily within the same molecule and across other antipsychotics, while pricing is dominated by generic entry, rebate dynamics, and payer contracting more than by “dosage form” alone.

What is the product boundary for “aripiprazole ODT” in pricing terms?

“Aripiprazole ODT” is best treated as a brand-to-generic and dosage-form replacement story, because:

- Many plans prefer the lowest net-cost option among therapeutically equivalent products.

- Generic penetration compresses list prices quickly; net prices depend on rebate and contracting.

For a pricing model, the practical comparator set is:

- Generic aripiprazole tablets (lower cost baseline)

- Other aripiprazole oral dosage formats

- Other atypical antipsychotic oral agents at the class level (less direct, but influences formulary tiering)

How does aripiprazole ODT pricing behave historically?

Across the US, list price declines sharply after generic launches, followed by:

- Sustained net-price compression via PBM contracting

- Continued erosion driven by increased competition across strengths and pack sizes

- Occasional short-term stabilization when fewer manufacturers remain “best price” compliant for specific pack formats

Because aripiprazole is widely generic, the dominant pricing determinant for aripiprazole ODT is how quickly ODT loses formulary share to cheaper non-ODT generics and to other antipsychotic generics with aggressive pricing.

What pricing inputs matter most for projections?

For aripiprazole ODT, projections should be anchored to:

- US net pricing pattern for generics (list-to-net discounting and PBM rebate compression)

- Market share shift from ODT to tablet as price differentials widen or shrink

- Competitive intensity (number of labeled ANDA products and strength coverage)

- Switching constraints (patient administration needs can slow erosion but not stop it)

- Regulatory and patent posture (after exclusivity ends, competitive pressure rises fast)

Market sizing and demand signal

A rigorous market size requires paid-claim and sales databases. This request targets price projection, and without claim-level sales inputs, the correct approach is to provide price-trajectory ranges rather than definitive revenue figures.

In practice, aripiprazole ODT demand is stable but priced like a niche dosage-form layer, not like a standalone high-value proprietary franchise. That means:

- Upfront list pricing has limited relevance once generics dominate

- Net pricing convergence toward the lowest-cost interchangeable oral options becomes the primary driver

Price Projection Model

What is the projected US price path for aripiprazole ODT?

Below are projection bands for US wholesale acquisition cost (WAC) style pricing and net realization bands are typically constrained by competitive rebates. Because actual net depends on contract, projections are expressed as range bands tied to generic-category behavior.

1) Generic-dominated phase pricing (most likely current state)

Assuming aripiprazole ODT is in a generic-competitive environment, projected annual price movement looks like this:

| Time horizon | Expected market structure | List price (WAC) band change | Net price (realization) band change |

|---|---|---|---|

| 0-12 months | Multiple generics on market, active PBM contracting | -3% to -12% | -2% to -10% |

| 12-24 months | Consolidation toward lowest-cost formulary winners | -2% to -8% | -3% to -9% |

| 24-36 months | Saturation; fewer pricing outliers | -1% to -6% | -2% to -7% |

Mechanics: list price drifts down slower than net because PBM and manufacturer discounting adjust quickly during contract renewals.

2) Post-exclusivity risk or entry-lag scenario (lower probability)

If ODT faced a shorter exclusivity tail or delayed generic penetration in certain strengths:

- Initial generic entries drive a step-change in list price

- Net prices drop more aggressively in the first contract cycle

| Time horizon | Expected market structure | List price (WAC) change | Net price change |

|---|---|---|---|

| 0-6 months | First meaningful generic launches for key strengths | -15% to -35% | -10% to -25% |

| 6-18 months | Additional entrants and tier changes | -5% to -15% | -5% to -18% |

| 18-36 months | Market stabilizes near class-average generic net | -1% to -8% | -2% to -10% |

What discount spread should be expected vs tablet generics?

ODT typically carries a premium versus swallowed tablets due to differentiation in patient administration. In heavily generic markets, the premium narrows unless ODT is used for adherence.

A reasonable projection band:

- ODT list price premium vs tablet generics: ~10% to 25%

- ODT net premium vs tablet generics after rebates: ~0% to 15%

- ODT can trade at parity when formulary rules or patient support programs push ODT adoption or when ODT manufacturers contract aggressively.

Strength and pack effects

Price varies materially by:

- Strength (mg) availability

- Pack size (count and days supply)

- Generic manufacturer lineup per strength

- Contract-specific preferred brands (including dosage-form preferred SKUs)

Projection rule:

- The fastest erosion occurs where multiple manufacturers compete for the same strength-pack SKU

- The slowest erosion occurs for orphaned SKU formats where fewer suppliers remain PBM-preferred

Scenario Forecast (3 cases)

How do prices evolve under base, low, and high competition scenarios?

All values are directional projection bands for US pricing trajectory.

Base case (typical generic competition)

- Annual list price: -3% to -8%

- Annual net price: -3% to -10%

- ODT premium vs tablet: compresses by 2 to 8 percentage points over 2 years

High competition case (multiple entrants per strength + aggressive PBM rebids)

- Annual list price: -8% to -18%

- Annual net price: -8% to -20%

- ODT premium vs tablet: collapses to 0% to 5% within 18-30 months

Low competition case (limited entrants in key strengths or slower contracting)

- Annual list price: -1% to -5%

- Annual net price: -1% to -6%

- ODT premium vs tablet: persists at 10% to 20% with slower convergence

Investment-grade signals to watch (price-sensitive milestones)

Price moves fastest when these occur:

- PBM formulary tier shifts after contract renewals

- New ANDA entries for ODT strengths or new label expansions

- Loss or gain of “preferred” status for specific pack sizes

- Parallel supply disruptions (short-term list stabilization, followed by normalization)

- National rebate policy changes that alter net realization quickly

Key Takeaways

- Aripiprazole ODT pricing behaves like a generic dosage-form niche inside a large, discount-driven oral atypical antipsychotic market.

- The most likely trajectory is continued annual erosion: list -3% to -8% and net -3% to -10% in a generic-competitive environment.

- ODT typically starts with a 10% to 25% list premium vs tablet generics, but the net premium compresses toward 0% to 15% as PBM contracting intensifies.

- Price dispersion is strongest by strength and pack SKU where the number of competing manufacturers differs.

FAQs

1) Will aripiprazole ODT pricing fall below tablet generics?

In high-competition contracting environments, net pricing can converge to parity or slightly below tablet generics, but persistent deep undercutting depends on PBM preference mechanics.

2) What has more impact on price: list price or net price?

Net price dominates commercial outcomes because antipsychotic markets are rebate- and contract-driven; list changes often understate real margin pressure.

3) Does ODT have pricing protection due to patient preference?

Patient preference can slow share loss, but it does not typically prevent net price erosion once generics compete and formularies steer toward lower-cost interchangeable options.

4) Which strengths usually see the fastest price erosion?

Strengths with the most competing SKUs and broader manufacturer participation show the fastest contraction in list and net pricing after contract cycles.

5) How quickly do PBM contract renewals affect price?

Impact typically appears in the next contract period: within 3 to 12 months, with a sharper move when a preferred tier changes.

References (APA)

[1] FDA. (n.d.). Drug approvals and databases (for aripiprazole product and dosage-form labeling context). U.S. Food and Drug Administration. https://www.fda.gov/drugs/drug-approvals-and-databases

[2] IQVIA. (n.d.). U.S. pharmaceutical market insights and pricing benchmarks (general market behavior used for generic price trajectory logic). IQVIA. https://www.iqvia.com/insights

[3] SSR Health. (n.d.). Pricing and market access coverage for prescription drugs (context for PBM-driven net price behavior). SSR Health. https://www.ssrhealth.com/

More… ↓