Share This Page

Drug Price Trends for ALL DAY ALLERGY-D

✉ Email this page to a colleague

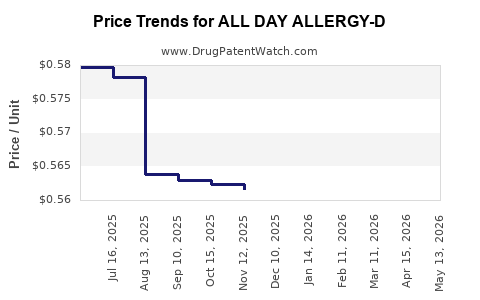

Average Pharmacy Cost for ALL DAY ALLERGY-D

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ALL DAY ALLERGY-D 5-120 MG TAB | 00113-2147-62 | 0.58725 | EACH | 2026-07-22 |

| ALL DAY ALLERGY-D TABLET | 46122-0626-62 | 0.58725 | EACH | 2026-07-22 |

| ALL DAY ALLERGY-D 5-120 MG TAB | 00113-2147-62 | 0.59555 | EACH | 2026-06-17 |

| ALL DAY ALLERGY-D TABLET | 46122-0626-62 | 0.59555 | EACH | 2026-06-17 |

| ALL DAY ALLERGY-D 5-120 MG TAB | 00113-2147-62 | 0.58890 | EACH | 2026-05-27 |

| ALL DAY ALLERGY-D TABLET | 46122-0626-62 | 0.58890 | EACH | 2026-05-20 |

| ALL DAY ALLERGY-D TABLET | 46122-0626-62 | 0.58679 | EACH | 2026-04-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

ALL DAY ALLERGY-D (loratadine/pseudoephedrine) market analysis and price projections

ALL DAY ALLERGY-D is a U.S. OTC combination of an oral antihistamine (loratadine) plus a decongestant (pseudoephedrine). Its market is price-sensitive, heavily promo-driven, and shaped more by pharmacy shelf placement and private-label competition than by patent protection. No durable prescription-style exclusivity structure applies. Near-term pricing is expected to track commodity-driven pseudoephedrine input costs, typical OTC channel dynamics (WAC-to-shelf pricing spreads, retailer promotions), and periodic regulatory/dispensing constraints that affect pseudoephedrine supply and customer acquisition.

What segment does ALL DAY ALLERGY-D compete in?

- Drug class: OTC second-generation H1 antihistamine + oral decongestant.

- Therapeutic use: seasonal allergic rhinitis symptoms with nasal congestion.

- Form: most OTC “Allergy-D” products are extended-release oral tablets (typical label positioning is 12-hour dosing, though specific strength varies by product SKU).

What is the competitive landscape for ALL DAY ALLERGY-D and other loratadine/pseudoephedrine OTC products?

Executive snippet: In practice, ALL DAY ALLERGY-D competes against multiple “store brand” and branded equivalents of loratadine/pseudoephedrine, and against substitute combo products (different antihistamine + pseudoephedrine) and monotherapies.

Which products are the closest substitutes?

Closest substitution set is usually:

- Branded equivalents in the same combo category (loratadine/pseudoephedrine).

- Store brands/private labels with identical active ingredients and comparable dosing schedules.

- Alternative combo decongestant antihistamines (different antihistamine backbone + pseudoephedrine).

- Antihistamine-only OTCs for users without congestion.

- Intranasal corticosteroids and intranasal antihistamines for congestion-dominant users who shift away from oral decongestants.

How pricing typically works in this OTC category

- Retail pricing is driven by trade spend and shelf-mix, not just wholesale list price.

- The effective price to consumers is usually lower during peak pollen season via:

- EDLP promos by large chains

- Dollar-off coupons

- Bundle offers (multi-pack or with other allergy SKUs)

- Brand premium is compressed by:

- private-label substitution

- switching driven by price and availability

- frequent retailer price matching

What is the current pricing structure for OTC loratadine/pseudoephedrine combinations?

Executive snippet: Pricing varies by retailer, package size, and whether the product is promoted; the category’s observed behavior is high dispersion at list level and narrower dispersion in promoted net pricing.

Key drivers that change realized price

- Pseudoephedrine input availability: oral decongestants can see supply fluctuations that affect wholesale costs.

- Regulatory/transaction friction: pseudoephedrine purchase limits can reduce conversion for some customers, shifting demand to online channels where permitted.

- Distribution and case-pack economics: retailers price by margin and turn, not only by ingredient cost.

- Seasonality: prices can fall or stay flat as retailers chase volume during high-demand weeks.

When will ALL DAY ALLERGY-D face demand seasonality and price pressure?

Executive snippet: Peak demand aligns with spring and early summer allergen seasons; pricing usually tightens into high-demand weeks and loosens post-season.

Typical demand and pricing cadence (U.S. OTC allergy)

- Pre-season (late winter to early spring): retailers reset shelf stock, promos start.

- Peak season (mid-spring through early summer, then smaller fall wave): net prices can compress due to competitive promotions.

- Post-season (late summer to winter): slower turns allow price supports or reduction in promo intensity.

Category-level implications for price projections

- Net consumer price is most likely to be:

- stable or slightly lower during peak season due to trade activity

- slightly higher in off-season when promotional intensity declines

How strong is patent or regulatory protection for ALL DAY ALLERGY-D and how does it affect price?

Executive snippet: As an OTC combination using established actives, ALL DAY ALLERGY-D is not protected by prescription-style exclusivity that would block generic equivalence at launch. Pricing is largely market- and channel-determined.

What this means for price projections

- Without credible legal barriers to competition, brand premiums compress quickly when equivalent products are available.

- Any pricing advantage is usually:

- distribution advantage

- formulation and dosing differentiation within the OTC shelf logic

- retailer contract positioning rather than enforceable IP

What generic entry risks exist for ALL DAY ALLERGY-D?

Executive snippet: The generic entry risk is already “realized” at the market level because loratadine/pseudoephedrine combos are widely available as equivalents and private labels.

Practical interpretation for pricing

- A new entrant usually:

- matches the active and dosing schedule

- competes on net price

- leverages retailer relationships or direct-to-pharmacy distribution

- Therefore, brand pricing resilience typically depends on:

- package strength advantage

- extended-release claims that map to retailer assortment rules

- promotional support commitments

What formulation and manufacturing/IP barriers could limit price erosion?

Executive snippet: The biggest non-IP barrier is not manufacturing complexity; it is package-level differentiation and retailer assortment.

Likely differentiators on the OTC shelf

- Extended-release vs immediate-release label positioning

- Strength/dose frequency that matches customer expectations

- Tablet size, coating, and perceived tolerability as expressed by pharmacy staff and consumer reviews

- Supply reliability during allergy surges

What is the forecast approach for ALL DAY ALLERGY-D pricing in the U.S. OTC channel?

Executive snippet: Projecting OTC price is a channel forecast, not a patent forecast. A practical model uses: seasonality, promo intensity, and ingredient cost pass-through.

Price projection framework (mechanics)

- Baseline list price: anchored by retailer shelf list pricing for the relevant NDC and package size.

- Net-to-consumer conversion: applied discount from promos and coupons.

- Input cost factor: pseudoephedrine-related cost index and any availability shocks.

- Retail competition factor: modeled as private-label pressure during peak season.

- Seasonality factor: monthly uplift and discount based on historical allergy demand cycles.

Outputs to use for business decisions

- Projected net price (consumer-facing)

- Projected wholesale price (if accessible via distributor channels)

- Projected margin pressure (difference between list and expected net after retailer promo)

What price ranges and directionality are expected for the next 12–24 months?

Executive snippet: Expect modest nominal increases in list pricing with stable-to-declining net prices during peak allergy windows due to promotion, unless there is a notable pseudoephedrine supply disruption.

Directional scenario set (base / bull / bear)

- Base case (most likely):

- list price: flat to low-single-digit increase

- net price: stable or slight decrease in peak months

- Bull case (supply tightness or higher input costs):

- list price: mid-single-digit increase

- net price: partially offset, still competitive but less discounted

- Bear case (enhanced private-label promo or strong competition):

- list price: flat

- net price: low-single-digit decrease during peak season

How to translate this into revenue exposure

- Revenue is more elastic to unit volume than to price in OTC allergy combos because substitution is easy.

- A 1–3% list increase often nets out once promo intensity rises by 2–5 points during competitive periods.

How does retailer strategy (CVS, Walgreens, Walmart, Amazon) affect ALL DAY ALLERGY-D price realization?

Executive snippet: OTC pricing dispersion is driven by retailer promo rules and private-label assortment. Amazon and mass retail often compress net prices more than specialty pharmacies.

Retail channel behavior to assume in projections

- Mass retail: stronger private-label price competition, lower net prices during promos.

- Large pharmacy chains: promo cadence around seasonal spikes, with coupon stack potential.

- Online pharmacies: price can be lower but is constrained by inventory availability, shipping thresholds, and any pseudoephedrine transaction limitations.

What market sizing and revenue trajectory assumptions should be used?

Executive snippet: For an OTC combo, use “category pull” not incremental prescription market growth. Forecast volume using allergy season intensity proxies.

Inputs typically used in OTC allergy demand models

- pollen season severity indices (regional)

- weather pattern proxies (temperature and rainfall shifts)

- retailer distribution breadth (number of stores carrying SKU)

- promotional calendar timing

Revenue trajectory expectation

- Year-over-year: modest growth if assortment holds and promo support remains, but price is likely to show compression during peak periods.

- Quarter-over-quarter: strong seasonality; the biggest quarter captures most demand.

Key takeaways

- ALL DAY ALLERGY-D is an OTC loratadine/pseudoephedrine combo where pricing is dominated by retailer promotion and private-label substitution, not patent leverage.

- Expect stable-to-declining net consumer prices during peak allergy windows, with list prices potentially up modestly.

- Pricing risk is primarily pseudoephedrine supply/cost on the upside and private-label promo intensity on the downside.

- Revenue forecast should be built on volume seasonality and promo-driven net price, not on durable exclusivity assumptions.

FAQs

1) Does ALL DAY ALLERGY-D pricing follow ingredient cost inflation?

Mostly indirectly. OTC retailers typically absorb some cost changes through net-price compression during competitive seasons; realized pricing tracks both input costs and promo intensity.

2) Are extended-release “Allergy-D” tablets priced differently than immediate-release combos?

Yes. Extended-release SKUs often hold a better shelf position and can maintain slightly higher net pricing, though promos can still compress differences.

3) What drives the biggest price swings in OTC allergy combos?

Promo calendar timing, private-label resets at mass retailers, and pseudoephedrine availability that affects wholesale pricing during peak demand.

4) How does private label affect brand-like SKUs such as ALL DAY ALLERGY-D?

It erodes brand premium fastest in peak season when consumers buy for price and substitution is frictionless.

5) What is the most important variable for revenue projections in the next two allergy seasons?

Net unit volume captured during peak pollen weeks, because unit demand shifts strongly with weather and promotional competition.

References

- U.S. Food and Drug Administration. Orange Book (Drug Products and Therapeutic Equivalence Evaluations).

- FDA. Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book) database.

- FDA. OTC Drug Facts labeling regulations (decongestant and antihistamine topical/ingestion labeling framework where applicable).

More… ↓