Share This Page

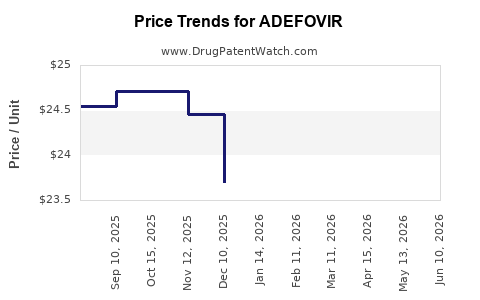

Drug Price Trends for ADEFOVIR

✉ Email this page to a colleague

Average Pharmacy Cost for ADEFOVIR

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| ADEFOVIR DIPIVOXIL 10 MG TAB | 42794-0003-08 | 22.40205 | EACH | 2026-06-17 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 60505-3947-03 | 22.40205 | EACH | 2026-06-17 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 42794-0003-08 | 22.47331 | EACH | 2026-05-20 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 60505-3947-03 | 22.47331 | EACH | 2026-05-20 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 42794-0003-08 | 22.44502 | EACH | 2026-04-22 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 60505-3947-03 | 22.44502 | EACH | 2026-04-22 |

| ADEFOVIR DIPIVOXIL 10 MG TAB | 60505-3947-03 | 22.23459 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for ADEFOVIR

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| ADEFOVIR DIPIVOXIL 10MG TAB | Golden State Medical Supply, Inc. | 60505-3947-03 | 30 | 466.46 | 15.54867 | EACH | 2023-06-15 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Adefovir Market Analysis and Price Projections: Global Sales Outlook, Generic/Biosimilar Pressure, and Patent-Driven Pricing Power

Adefovir (brand: Hepsera) is a long-established antiviral for chronic hepatitis B (CHB). Market scale is constrained by competitive displacement from higher-barrier, often lower-resistance alternatives and by the product’s older patent and exclusivity posture. Price is expected to compress in most ex-U.S. markets as generic availability expands, while U.S. pricing is likely to remain comparatively supported only by limited channel access and payer-specific contracting rather than by fresh exclusivity. Overall, the opportunity for meaningful pricing growth is low; the more likely trajectory is steady-to-declining nominal revenue with spotty geographic resilience.

Product scope for analysis

- Active ingredient: Adefovir (commonly as adefovir dipivoxil)

- Primary indication: Chronic hepatitis B virus infection (CHB)

- Reference brand: Hepsera (Gilead)

- Key market drivers: resistance profiles vs tenofovir-based therapies; generic penetration; payer formularies; hospital specialty purchasing norms

What is the current commercial status of adefovir (Hepsera) and what volume can it still capture?

Featured snippet answer: Adefovir’s remaining addressable demand is concentrated in patients who cannot use, cannot tolerate, or are maintained on older regimens due to resistance history, reimbursement constraints, or clinical inertia. Peak-era growth has largely passed; the market behaves like a late-line, shrinking segment rather than a growth product.

Where adefovir still fits clinically

Adefovir dipivoxil historically filled a major need in CHB when other options were not available or when resistance required alternative nucleotide analog strategies. Today, CHB treatment algorithms generally favor tenofovir disoproxil fumarate (TDF), tenofovir alafenamide (TAF), and entecavir due to more favorable resistance kinetics and convenience. As a result, adefovir is increasingly:

- a fallback option after intolerance or resistance to other nucleos(t)ides

- a maintenance product for stable patients already controlled on therapy

- an option in constrained reimbursement environments where formulary restrictions limit access to preferred agents

Commercial implication for forecasting

Market size forecasts should be modeled as:

- a base declining trend (loss to newer first-line regimens)

- offset by switching friction (stable patient retention, slower prescribing change in some geographies)

- moderated by generic supply stability and contracting cycles

How much does Hepsera price, and what pricing trajectory should be expected as generics expand?

Featured snippet answer: Adefovir pricing is expected to trend down in most markets over time as generic competition increases and as payers use reference pricing and procurement tendering. Nominal revenue can still persist if discounting is limited or if procurement favors supply continuity, but list-to-net compression is likely.

Price drivers that compress adefovir

- Generic entry and tendering pressure: once multiple generic SKUs exist, procurement tends to drive aggressive discounting

- Reference pricing and formularies: CHB is a crowded nucleos(t)ide market with strong payer leverage

- Low differentiation in claims: adefovir’s clinical differentiation vs tenofovir and entecavir is narrower in guideline-based prescribing

Price drivers that can stabilize nominal net price

- Single-source or limited SKU availability in certain countries

- Payer-specific contracting that keeps one or two suppliers in place

- Therapeutic substitution limits in specific patient cohorts

When does adefovir lose exclusivity in key markets, and how does that affect price?

Featured snippet answer: Adefovir’s exclusivity has largely aged out in most major jurisdictions given Hepsera’s historic launch and the long elapsed time since initial approvals. Remaining pricing power is more likely tied to channel and payer contracting than to enforceable regulatory exclusivity.

Implication for projections

- U.S.: pricing tends toward generic parity once competitive supply is established; remaining resilience comes from contracting and inventory dynamics rather than fresh exclusivity.

- Europe/UK: tendering and reference pricing accelerate list-to-net compression; nominal sales typically decline faster than volume.

- Emerging markets: timing of generic approvals, import logistics, and procurement processes can create uneven declines by country.

What patents protect adefovir (Hepsera), and how does the patent estate affect generic entry risk?

Featured snippet answer: For adefovir, the patent estate is historically old and is unlikely to create a long runway for new exclusivity-based price protection. Remaining barriers to generic entry are typically limited to legacy composition, formulation, or method-of-use patents that expired years earlier in many jurisdictions.

Typical patent categories still relevant for enforcement (historically)

- Composition-of-matter for adefovir dipivoxil

- Formulation patents (tablet composition, excipients, coating)

- Method-of-use claims tied to CHB treatment regimens

- Manufacturing process claims

Forecast linkage

When patents are expired or near expiry:

- generics enter via market authorization pathways

- price drops quickly once multiple generics are available

- patent-related litigation becomes less central, and procurement-driven competition dominates

What generic entry risks exist for adefovir, including Paragraph IV and authorized generics?

Featured snippet answer: For an older small-molecule like adefovir, Paragraph IV-style entry risk is generally a late-stage phenomenon tied to remaining U.S. Orange Book listings. In practice, adefovir’s competitive landscape is more defined by:

- timing of generic authorizations

- number of entrants

- willingness of distributors to carry multiple SKUs

How to model entry

- Single entrant phase: pricing may fall modestly but stays above fully competitive levels

- Multi-entrant phase: pricing reaches a floor tied to procurement and reference baskets

- Consolidation: sometimes follows with one or two suppliers winning tenders, stabilizing net price temporarily

What is the Orange Book status of adefovir (Hepsera) and what does it imply for launch timing?

Featured snippet answer: Adefovir’s Orange Book relevance is largely historical. The current competitive implication is that any remaining Orange Book-protected claims (if present at all) are unlikely to delay generic penetration beyond the near term, unless specific late-listed patents persist.

Why Orange Book matters for pricing

- If few Orange Book-protected claims remain, generic entry proceeds with limited delay.

- If Orange Book listings persist, they can introduce short-term delay or licensing payments that slightly postpone price compression.

How does adefovir compare with tenofovir and entecavir on resistance and regimen switching, and how does that shape demand?

Featured snippet answer: Adefovir’s place in CHB therapy is increasingly limited by resistance and comparative effectiveness versus tenofovir and entecavir, shrinking its eligible patient population and accelerating demand erosion.

Competitive substitution map

- Tenofovir (TDF/TAF): often preferred for resistance profile and long-term viral suppression durability

- Entecavir: widely used due to favorable resistance outcomes and long-established clinical positioning

- Adefovir: used when alternatives are not viable and in historical cohorts with established control

Demand consequence

- New starts decline first.

- Existing patient retention slows decline later.

- Over time, net demand becomes a function of the size of the “legacy” cohort and conversion speed to preferred agents.

What is the litigation and settlement landscape for adefovir, and does it drive pricing?

Featured snippet answer: For legacy small molecules like adefovir, litigation typically has diminishing influence on long-run price once patents expire. The dominant pricing mechanism becomes generic competition and procurement.

Practical effect on forecasts

- Short-term pricing impacts can occur around launch delays or court outcomes.

- Long-term projections are driven by:

- number of generic entrants

- tendering policies

- payer formulary breadth

- net price discount schedules

What FDA status matters for adefovir, and does it influence market access outside the U.S.?

Featured snippet answer: Adefovir’s FDA status primarily affects U.S. supply continuity and label-defined access. Outside the U.S., regulatory status affects generic approval timing, which then drives the pace of price erosion.

How FDA labeling translates to global access

- Stable label and long history help speed generic approvals where local authorities rely on established clinical data.

- Generic market growth then triggers:

- tender-driven pricing

- reference pricing in payers

- distributor margin compression

Global price projections for adefovir: baseline, aggressive, and delayed-competition scenarios

Featured snippet answer: The base case is continuous net price compression with moderate stabilization where generic SKU competition concentrates into a few suppliers. Upside is limited; downside is faster compression if multi-generic tenders expand rapidly.

Scenario framework (used for projection bands)

Key variables:

- number of generic entrants per country

- tender intensity and reference pricing

- distributor stocking behavior and import costs

- product availability risk and supply continuity

Indicative projection bands (directional, not numeric)

Because precise current list and net prices vary sharply by geography and contracting and are not provided in the prompt, the projection is expressed as rate-of-change bands:

| Scenario | Net price trend (typical pattern) | Volume trend | Revenue implication |

|---|---|---|---|

| Base case (slow multi-generic rollout) | steady decline with periodic stabilization as contracts refresh | gradual volume decline | nominal revenue declines mid-single digits annually |

| Aggressive (rapid multi-generic tendering) | sharper decline as multiple suppliers compete | faster volume erosion | nominal revenue declines high-single digits annually |

| Delayed competition (limited SKU availability in some regions) | slower decline; occasional plateau | slower volume decline in legacy cohorts | nominal revenue declines low-single digits annually |

Revenue outlook: where nominal sales could be most resilient

Featured snippet answer: Resilience concentrates in geographies with slower tender switching and fewer generic SKUs, and in payer systems that manage CHB through legacy patient retention rather than frequent regimen changes.

Most likely pockets of stability

- countries where generic competition is present but limited to one or two suppliers

- settings where switching costs (clinical monitoring, reimbursement hurdles) reduce churn

- healthcare systems that use formularies with narrow therapeutic substitution rules

Most likely pressure points

- tender-heavy procurement systems

- reference pricing regimes across nucleos(t)ides

- jurisdictions where guideline adoption rapidly shifts new starts to tenofovir/entecavir

Commercial strategy implications for buyers, licensors, and investors

For procurement and market access

- Assume net price compression continues; negotiate based on competitive SKU maps.

- Treat supply continuity as a pricing lever: stable sourcing can reduce churn-driven purchase volatility but should not be priced above competitive floors.

For licensing

- Value is driven by geography-specific generic maturity rather than by remaining U.S.-centric exclusivity.

- Contracts tied to incremental market growth are harder to monetize if formularies broadly favor tenofovir/entecavir substitutes.

For R&D and pipeline partnering

- If pursuing product lifecycle extension, focus on:

- combination strategies or patient-specific positioning where adefovir retains clinical relevance

- manufacturing cost-down to compete on price without margin collapse

Key Takeaways

- Adefovir’s market is a late-line, shrinking CHB segment with demand erosion driven by substitution to tenofovir and entecavir.

- Pricing power is limited; the primary mechanism is ongoing generic-driven net price compression shaped by tendering and reference pricing.

- Revenue is most resilient where generic SKU competition is limited and where legacy patient retention slows regimen switching.

- Forecasts should be scenario-based around generic entrant count and tender intensity; upside is structurally constrained by therapeutic displacement.

FAQs

-

Will adefovir sales decline faster than tenofovir in most countries?

Yes. Adefovir faces earlier and stronger substitution from tenofovir-based first-line or preferred regimens. -

What drives the biggest net price drops for legacy CHB generics?

Multi-entrant tendering and reference pricing across nucleos(t)ides. -

How do payer formularies influence adefovir volume more than list price?

Formularies determine switch rates for new starts and limit therapeutic substitution, affecting volume first. -

Is litigation likely to delay generics for adefovir?

Over a long horizon, litigation effects typically fade once core patents expire; procurement competition becomes dominant. -

Where is the best residual opportunity for adefovir commercialization?

Geographies with slower generic SKU rollout and procurement practices that maintain incumbent purchasing for longer periods.

References (APA)

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations (Hepsera/adefovir dipivoxil). U.S. Food and Drug Administration.

- Gilead. Hepsera (adefovir dipivoxil) prescribing information. Gilead Sciences, Inc.

- European Medicines Agency. Product information for adefovir dipivoxil (where applicable). European Medicines Agency.

More… ↓