The cheapest medicines in America are also the most dangerous ones to run out of. Generic sterile injectables — levofloxacin, droperidol, cisplatin, carboplatin, normal saline — cost pennies per unit and form the operational backbone of every ICU, oncology suite, and emergency department in the country. They are also collapsing in supply with increasing regularity, not despite their low prices, but directly because of them.

This is a detailed account of why the generic drug pricing model structurally produces shortages, what that failure looks like at the manufacturing plant level, how the federal government has responded, what is not working, and where durable solutions might actually exist.

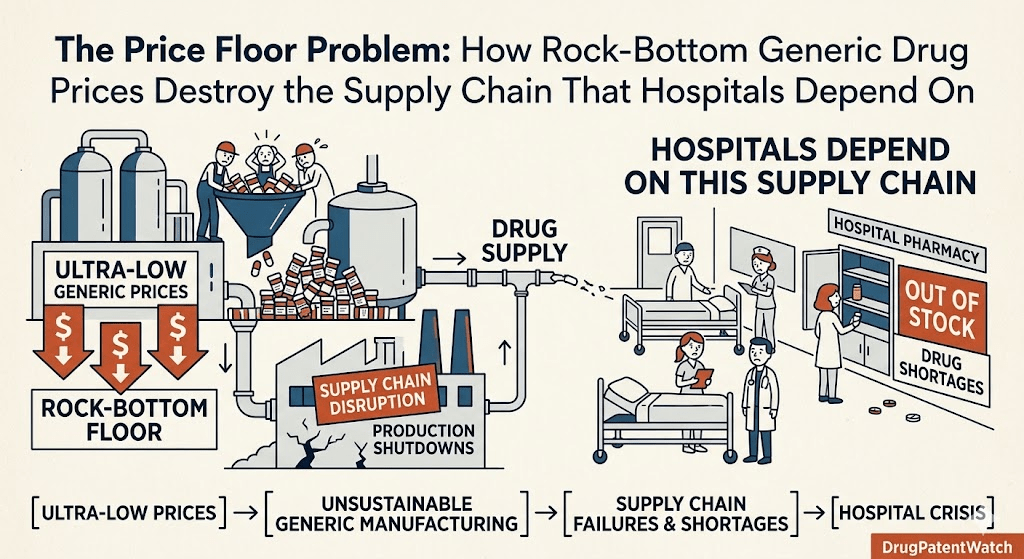

The Core Mechanism: Why Price Competition Breaks Generic Markets

The Bioequivalence Commodity Trap

The FDA’s generic drug approval framework, governed by the Hatch-Waxman Act of 1984 and its abbreviated NDA (ANDA) pathway, certifies that a generic product is bioequivalent to its reference listed drug. That certification is the entire legal product. Once the FDA issues an approval, the agency communicates to the market that all approved generics are therapeutically interchangeable — equivalent in dosage form, route of administration, strength, and quality standard.

That equivalence signal is the structural foundation of the price collapse. If product A and product B are legally and clinically equivalent, the only competitive lever left is price. Hospital group purchasing organizations (GPOs) — Premier, Vizient, Intalere, HealthTrust — run bid processes that select the lowest-cost contracted supplier across their member hospital networks. A GPO representing 4,000 hospitals can deliver essentially the entire demand for a given generic injectable to a single winning bidder. The winning manufacturer captures enormous volume; the losers either exit the product or wait for the next contract cycle.

Erin Fox, associate chief pharmacy officer at University of Utah Health and one of the country’s most credentialed experts on pharmaceutical supply, put the mechanism plainly: ‘Because the FDA says all generics are equal, the only way to compete is on price.’ That competition produces a race to the minimum sustainable price point — and often below it.

Sterile Injectables: Where Commodity Pricing Meets Complex Manufacturing

The pricing dynamics that produce shortages are not uniform across all generic drug categories. Oral solid dosage forms — tablets, capsules — are subject to the same bioequivalence rules, but the manufacturing infrastructure to produce them is relatively low-cost, geographically distributed, and scalable. A tablet manufacturer that loses a GPO contract can pivot to other products, repurpose capacity, or wait out the cycle.

Sterile injectables are categorically different. A sterile fill-finish facility requires Class ISO 5 cleanrooms, specialized aseptic processing equipment, validated sterilization systems, and layers of in-process and release testing that add months and millions to any production run. The FDA’s Current Good Manufacturing Practice (cGMP) requirements for sterile drug products under 21 CFR Part 211 are among the most stringent in pharmaceutical regulation. Qualifying a new sterile line from site selection through FDA inspection and product approval realistically takes 24 to 48 months under favorable conditions.

The capital intensity of sterile manufacturing, combined with the price suppression of generic competition, produces a market where the return on investment for maintaining a compliant sterile facility is deeply unattractive. Manufacturers strip cost wherever they can — deferred maintenance, reduced staffing, compressed quality control timelines — until the facility fails an FDA inspection or simply becomes uneconomic to operate. At that point, they exit the market, and because the market often had only two or three qualified manufacturers to begin with, their exit immediately converts into a national shortage.

HHS data confirm the pattern: the median shortage duration for generic sterile injectable drugs is 4.6 years. For oral solids, it is 1.6 years. The extended duration reflects the physical reality that replacement capacity cannot be turned on quickly.

The Single-Source Concentration Risk

The FDA reported in 2020 that 40% of generic drug markets have a single manufacturer supplying the entire U.S. market. For shortage-prone drugs, that concentration is even more extreme. IQVIA Institute data show that 56% of all molecules in shortage price below $1.00 per unit. Pharmaceutical Commerce’s 2026 analysis of the U.S. generics market found that 44% of injectable products in shortage price below $5.00 per unit. At those price points, the economics of maintaining multiple competitive suppliers in a capital-intensive manufacturing category simply do not work.

The concentration has a compounding effect. When a single-source manufacturer of a sterile injectable experiences a quality failure, a natural disaster, or a business failure, there is no second qualified site to absorb the volume, no contracted surge capacity, and no meaningful federal strategic reserve. The shortage is immediate and, given the timeline for qualifying replacement supply, long.

Between 2013 and early 2024, 37% of all FDA-approved generic drugs had never been commercially launched. For drugs actively in shortage, 84% had at least one approved-but-unlaunched generic. The regulatory approval exists, but the economics do not justify launching it. This is not a regulatory failure — it is a market failure that regulation cannot solve without structural pricing intervention.

Key Takeaways

The Hatch-Waxman bioequivalence framework, combined with GPO contracting that selects on price alone, forces generic sterile injectable manufacturers to compete below the cost of sustainable cGMP-compliant production. Single-source market concentration converts any manufacturing disruption into a national shortage. The median shortage for a generic injectable drug now exceeds four and a half years.

The Akorn Collapse: A Facility-Level Autopsy

Akorn’s Business Model and IP Asset Profile

Akorn Pharmaceuticals was founded in 1971 and grew into one of the country’s more significant producers of specialty generic injectables, ophthalmic products, oral liquids, and inhalants. Its product line at the time of closure covered approximately 100 SKUs out of its Decatur, Illinois facility alone, with additional manufacturing in Vernon Hills, Illinois, and a corporate headquarters in Gurnee.

From an IP perspective, Akorn’s portfolio was ANDA-dominant — a collection of FDA-approved abbreviated new drug applications that conferred the legal right to manufacture and sell generic versions of off-patent reference listed drugs. ANDAs are transferable, licensable assets with defined regulatory value, but they carry no patent exclusivity. Their commercial value depends entirely on the manufacturer’s ability to maintain cGMP compliance at an approved facility and sustain a manufacturing cost structure that survives in a price-competitive market.

Akorn’s IP assets were not trivial. The company held Paragraph IV certifications on several branded drugs, meaning it had actively challenged innovator patents to secure first-generic exclusivity under the 180-day exclusivity provision of Hatch-Waxman. First-generic exclusivity, when it attaches to a high-revenue reference drug, can produce gross margins above 70% for the exclusivity window. Akorn captured several of these windows historically, which funded the company’s expansion into sterile manufacturing. But the sterile injectable core of the business — lower-priced, compliance-intensive, GPO-contracted — generated insufficient margin to sustain operations as competition intensified.

Akorn filed Chapter 11 bankruptcy in 2020, restructured, and emerged with a leaner cost structure. The restructuring did not resolve the underlying unit economics of its sterile injectable business. The company continued to operate at a loss and failed, in early February 2023, to find an acquirer willing to assume its liabilities. It filed Chapter 7 — liquidation, not reorganization — and shut all four manufacturing sites on approximately 24 hours’ notice.

The Closure: Operational and Regulatory Consequences

The Chapter 7 filing triggered a cascade of regulatory and operational consequences that illustrated, in concentrated form, how a single manufacturer’s exit propagates through the hospital supply chain.

Akorn laid off 400 employees in Decatur. Illinois law requires 60 days’ notice of plant closure for companies with 75 or more full-time employees — Akorn did not provide it, prompting an investigation by the Illinois Department of Labor. The abruptness was not simply a labor law violation; it had direct patient safety consequences. Six weeks after the closure, Akorn recalled all 70-plus products it had manufactured. The recall was not because the drugs were defective or expired — they were not. The recall issued because no one remained at Akorn to answer the phone and initiate a product-specific recall if a problem emerged post-distribution. The mere absence of a responsible company to steward the distributed product triggered removal from hospital shelves.

University of Utah Health, one of the more systematically prepared hospital systems in the country, absorbed 250 unplanned labor hours in the immediate aftermath — removing products from shelves, contacting physicians, and sourcing replacement supply. The Mayo Clinic scrambled across its pharmacist network to switch suppliers for products where Akorn had been the sole or primary contracted source. Eric Tichy, division chair of pharmacy supply solutions for the Mayo Clinic and board chair of the End Drug Shortages Alliance, described the situation as ‘definitely a challenging situation.’ That is a clinical understatement. For hospitals that lacked the supply chain infrastructure of a Mayo or University of Utah, the fallout was worse.

The Akorn closure contributed to new drug shortages and deepened existing ones across levofloxacin injection, tetracaine injection, droperidol, and several ophthalmic products. In some categories, Akorn had been the sole domestic manufacturer.

Rising Pharmaceuticals: The Acquisition and Its IP Logic

Rising Pharmaceuticals, a New Brunswick, New Jersey-based generic drug company and portfolio company of Miami private equity firm H.I.G. Capital, acquired the Decatur manufacturing and packaging site for $1.2 million in June 2023. The packaging facility sold for $50,000. The total acquisition cost for a 230,000-square-foot sterile manufacturing complex was $1.25 million — a figure that captures how completely the market had devalued sterile injectable manufacturing capacity.

Rising’s business model at acquisition was primarily asset-light: the company commercialized approximately 180 generic products with manufacturing largely outsourced to a network of roughly 23 contract development and manufacturing organizations (CDMOs). Its IP portfolio consisted of ANDAs and NDAs across therapeutic categories including central nervous system, cardiovascular, anti-infective, and metabolic products. Rising also held branded generic assets through its Casper Pharma subsidiary.

The Decatur acquisition represented a deliberate pivot from the asset-light model — an acknowledgment that domestic sterile manufacturing capacity, even at depressed acquisition prices, has strategic value that the asset-light structure cannot capture. Rising announced the facility’s reopening in September 2023, with a target of commercial production by the second half of 2024. The company committed to restoring levofloxacin injection, tetracaine, droperidol, and a range of former Akorn ophthalmic products.

The IP valuation of the Decatur facility for Rising’s purposes is not in the brick-and-mortar acquisition price — $1.25 million is noise on a pharma balance sheet. The value lies in the ANDAs Rising acquired or is reactivating, the FDA manufacturing site registrations that accompany those ANDAs, and the position those registrations create in shortage markets where competition is limited. A sterile injectable ANDA tied to a shortage market with two or fewer competitors trades at a very different commercial multiple than the same ANDA would in a six-supplier market.

Rising’s CEO Vimal Kavuru, speaking in late 2023, indicated the company was taking a measured approach to bring the facility back into commercial production — a direct acknowledgment that the operational risks of an accelerated restart (failed FDA inspection, product recall, GMP deficiency) could be more costly than the revenue delay of a careful requalification.

Key Takeaways

Akorn’s Chapter 7 bankruptcy exposed the dual fragility of a business model that relies on price-competitive sterile injectable manufacturing without sufficient margin to sustain cGMP compliance. The $1.25 million acquisition price for a 230,000-square-foot sterile facility illustrates how completely the market had marked down the asset. Rising Pharmaceuticals’ acquisition represents a strategic bet that shortage-market ANDA positions in sterile injectables carry durable commercial value — but the requalification timeline and ongoing cost structure must be managed to avoid repeating Akorn’s trajectory.

Investment Strategy

Private equity acquirers evaluating distressed sterile injectable manufacturers should model the ANDA portfolio value on a shortage-adjusted basis — not on normalized competitive pricing. In a two-supplier or single-source shortage market, the relevant pricing comp is not the contracted GPO price; it is the gray market clearing price, discounted for the legal and reputational risk of gray market exposure. Rising paid $1.25 million for a facility whose ANDA portfolio, if successfully reactivated into shortage markets, could generate revenue multiples that make the acquisition highly accretive. The key variable is the FDA inspection outcome. Investors should build 12-to-18-month post-restart FDA re-inspection timelines into any return model for distressed sterile facilities.

The Chemotherapy Parallel: Intas, Cisplatin, and the India Supply Chain Problem

How a Single Indian Plant Created a National Oncology Crisis

The Akorn failure was a domestic story. The Intas Pharmaceuticals failure was a global one, and it illustrated the second structural vulnerability in the generic drug supply chain: geographic concentration of manufacturing in countries with different regulatory cultures and enforcement histories.

In November 2022, FDA inspectors arrived at Intas Pharmaceuticals’ sterile manufacturing plant in Ahmedabad, India — the plant that at the time supplied approximately 50% of U.S. cisplatin and 20% of U.S. carboplatin. The inspection found what internal records described as a ‘cascade of failure’ in the facility’s quality control unit. The most striking finding was hundreds of trash bags containing shredded quality control records being loaded into a garbage truck as inspectors arrived — what FDA’s inspection report characterized as a systematic effort to conceal quality problems.

Intas voluntarily shut the Ahmedabad facility. The FDA posted its inspection findings in January 2023. By February 2023, cisplatin and carboplatin were in national shortage.

The clinical consequences were immediate and severe. By May 2023, 93% of academic cancer centers reported a shortage of carboplatin, per National Comprehensive Cancer Network (NCCN) survey data. Roughly 70% of centers were short of cisplatin. Two-thirds reported methotrexate in short supply. The shortage extended to 5-fluorouracil, fludarabine, and hydrocortisone as demand shifted. Carboplatin that normally sold for $30 per 600-milligram bottle was selling on the gray market for $185 in early May 2023 and $345 a week later.

The FDA approved temporary importation of unapproved cisplatin from Chinese manufacturer Qilu Pharmaceutical to relieve pressure on the supply. The FDA Commissioner declared the cisplatin national shortage resolved in mid-2024, after Intas resumed shipping cisplatin, carboplatin, and 14 other injectables to the U.S. market following a corrective action process.

Structural Lessons From Cisplatin

The Intas crisis made explicit what the generic supply chain academic literature had argued for years: FDA approval of multiple manufacturers for a given molecule does not guarantee supply resilience if most of the approved manufacturing volume sits in a single geographic location or a single facility.

Cisplatin was not a sole-source drug. Fresenius Kabi, Hikma Pharmaceuticals, Teva, and Pfizer all manufactured cisplatin for the U.S. market. But their combined capacity was insufficient to replace the volume that the Intas plant had supplied. And they had no contractual or financial incentive to maintain surge capacity — the economics of generic sterile injectable manufacturing in a competitive contracted market discourage maintaining idle capacity.

The FDA’s own inspection reporting timeline compounded the problem. Warning letters and Form 483 inspection observations often lag the underlying inspection by several months. Premier, which manages wholesale drug purchases for more than 4,400 hospitals, understood in December 2022 that the Intas shutdown threatened U.S. cisplatin supply — but the shortage was not officially acknowledged until February 2023. That two-month gap represents lost preparation time for hospital systems that, had they known, could have built buffer inventory.

Cisplatin sells for approximately $16 per dose. The API manufacturing process is technically demanding — platinum-based coordination chemistry with exacting purity requirements. The combination of low unit price and high manufacturing complexity makes cisplatin a textbook case of a drug the market prices too cheaply to sustain redundant domestic supply.

Key Takeaways

The Intas shutdown demonstrated that manufacturer count on an FDA approval list does not equate to resilient supply. Geographic concentration of sterile injectable manufacturing in a single country, or a single facility within a country, converts any quality failure into a national crisis. The cisplatin shortage reached 70% of academic cancer centers. Resolution required FDA exercise of enforcement discretion to temporarily permit importation of unapproved product from China — an outcome that the U.S. regulatory framework is not designed to normalize.

Investment Strategy

Portfolio managers evaluating generic oncology assets should stress-test supply chain geography as a distinct risk variable, separate from product-level patent exposure. A generic oncology injectable with 80% of its manufacturing volume concentrated in a single overseas facility is a credit-risk asset regardless of its ANDA count. Manufacturers that can demonstrate domestic sterile fill-finish capacity for high-shortage-risk molecules — cisplatin, carboplatin, methotrexate, fluorouracil — carry a supply chain premium that is currently underpriced by the market.

The Federal Response: Defense Production Act, DPA Title III, and Their Limits

The November 2023 White House Action

In November 2023, the Biden administration convened the first meeting of the White House Council on Supply Chain Resilience and announced approximately 30 supply chain-related executive actions. The pharmaceutical component centered on invoking the Defense Production Act (DPA) to support domestic manufacturing of essential medicines.

Specifically, HHS’s Administration for Strategic Preparedness and Response (ASPR) received a presidential determination in December 2023 expanding its authority under DPA Title III to invest in domestic production of essential medicines, medical countermeasures, and critical API inputs. HHS identified $35 million for initial investments in domestic production of key starting materials for sterile injectable medicines.

In October 2024, ASPR executed on that authority with a $17.5 million agreement to support domestic manufacturing of API starting materials, managed through the Biopharmaceutical Manufacturing Preparedness Consortium (BioMaP-Consortium) under an Other Transaction Authority agreement with BARDA.

Why $35 Million Is Not a Solution

The DPA investments are directionally correct and strategically inadequate. Building a single compliant sterile injectable manufacturing facility — not an API plant, not a packaging site, but a functional fill-finish operation meeting FDA cGMP requirements — costs between $200 million and $500 million depending on scale, technology platform, and site requirements. The $35 million committed by HHS does not fund a facility; it funds early-stage investments in starting material manufacturing, which is two or three steps upstream from the finished-dose shortage.

The more structurally meaningful challenge is that the DPA does not address the underlying economics. A domestic sterile injectable manufacturer receiving DPA-funded capital for facility modernization still sells into a market where GPO contracting selects the lowest-cost bidder. The manufacturer cannot recover the DPA-subsidized capital cost through pricing if the market clearing price remains at levels that made Akorn’s operations unsustainable.

ASPR’s approach under Title III targets ‘create, maintain, protect, expand, or restore domestic industrial base capabilities’ for national emergencies. That is a defense posture, not a market reform. It can fund capacity; it cannot fix price signals.

The Senate Finance Committee’s 2024 white paper on drug shortages recommended tying reimbursement for generic sterile injectables to manufacturing quality and reliability scores — essentially a reliability-weighted pricing floor. That proposal has not been enacted. Until pricing reform attaches to quality and supply reliability, capital investments in domestic manufacturing will face the same commercial pressure that collapsed Akorn.

The FTC and GPO Middleman Investigation

In February 2024, the FTC and HHS jointly launched an investigation into the role of GPOs and pharmaceutical wholesalers in perpetuating generic drug shortages. The investigation targeted the competitive dynamics that allow GPOs to drive prices below sustainable manufacturing cost — practices that may, on their face, look like procompetitive price pressure but that produce the structural outcomes of single-source concentration, manufacturer exit, and shortage.

The GPO business model depends on rebates and administrative fees paid by contracted manufacturers. Those fee structures can create incentives for GPOs to favor manufacturers offering deeper discounts, compressing margin further. The investigation acknowledged what supply chain researchers have argued for years: the entity selecting on price does not bear the consequences of shortage.

Key Takeaways

Federal policy responses since 2023 have been incremental and structurally misaligned with the root cause. DPA Title III investments address manufacturing capacity without addressing the price signals that make domestic sterile injectable manufacturing economically unviable. Without pricing floor mechanisms that reward quality and supply reliability — not just bioequivalence — the cycle of manufacturer exit and shortage will continue.

The Scale of the Current Crisis: ASHP Data and Vizient Cost Estimates

Active Shortage Data Through 2025-2026

ASHP and the University of Utah Drug Information Service maintain the most comprehensive public drug shortage database in the U.S. Active shortage counts peaked at 323 in Q1 2024, the highest level since ASHP began systematic tracking. As of the end of 2025, 216 active shortages remained — down from peak, but still historically elevated.

New shortage creation slowed meaningfully in 2025: ASHP estimated fewer than 100 new shortages would be identified during the year, which would be the lowest new-shortage count since 2006. But new shortage rate is the wrong metric for assessing the burden on hospital systems. Many of the 216 active shortages at end-2025 began in 2022 or earlier. Three-quarters of active shortages as of Q3 2025 started in 2022 or later. Long-standing shortages do not resolve at the same rate that new shortages appear; injectable drug shortages, with their 4.6-year median duration, stack and persist.

The five drug classes with the highest active shortage counts as of Q1 2025 were central nervous system agents (49 shortages), antimicrobials (39), fluids and electrolytes (29), hormone agents, and chemotherapies. Epinephrine — the first-line treatment for anaphylaxis and cardiac arrest — has been intermittently short for years. Normal saline (0.9% sodium chloride injection) and 5% dextrose bags have appeared on shortage lists. These are not niche drugs.

The Hospital Cost of Managing Shortages

The operational burden of shortage management has been comprehensively documented by Vizient. Hospital labor costs tied to shortage management rose from $359 million in 2019 to $894 million in 2024 — nearly a 150% increase over five years. Separately, Vizient estimates hospitals spend an additional $200 million annually on higher-priced substitute products when their contracted generics are unavailable.

In large hospitals of 300 or more beds, shortage management consumes approximately 40 hours of pharmacy staff time per week. In the largest systems, it exceeds 60 hours. ASHP’s Michael Ganio, senior director of pharmacy practice and quality, has characterized this as a ‘full 40-hour job’ for the week in large facilities. That labor is not generating clinical value — it is compensating for a market failure.

IQVIA data from 2026 put the aggregate annual drug shortage burden to U.S. health systems at approximately $900 million in direct labor costs. That figure does not include the cost of adverse patient outcomes, delayed surgical procedures, protocol modifications in oncology, or the downstream legal exposure of shortage-related treatment changes.

Key Takeaways

Active shortages declined from the 2024 peak of 323 but remain historically high at 216 as of end-2025. The cost to hospital systems of managing shortages has nearly tripled since 2019, reaching approximately $900 million annually in labor alone. These costs are not borne by the manufacturers who priced drugs below sustainable cost — they are externalized entirely onto hospital systems and ultimately onto patients.

What a Structural Fix Requires: Policy Options With Specificity

Pricing Floors Tied to Quality and Reliability

The most analytically coherent proposal in the academic and policy literature is a reliability-weighted floor price for essential generic sterile injectables. The mechanism would work as follows: the FDA, using its Quality Management Maturity (QMM) program, certifies manufacturers on a tiered scale of manufacturing quality and supply reliability. CMS or HHS then sets a minimum reimbursement rate for essential shortage-prone generics that reflects the cost of operating a compliant facility — not the marginal cost of the lowest-cost bidder.

This is not a price control; it is a price floor. GPOs could still compete above the floor. But the floor prevents the race to zero that collapses the supplier base for critical drugs. The Senate Finance Committee white paper from 2024 endorsed this structure. The pharmaceutical industry and GPO lobbies have resisted it, for predictable reasons.

Strategic API Reserves and Guaranteed Purchase Contracts

The Intas cisplatin crisis demonstrated that the U.S. has no meaningful strategic reserve of generic injectable APIs or finished-dose product. The Strategic National Stockpile (SNS) maintains reserves of certain medical countermeasures and some branded products, but generic sterile injectables — by definition, low-value and perishable — have not been prioritized.

Guaranteed purchase contracts, structured similarly to Project BioShield contracts for biodefense products, would give domestic manufacturers a committed buyer for a defined volume at a price above the market floor. The committed volume reduces the manufacturer’s revenue risk from GPO contracting cycles; the above-floor price compensates for the cost of maintaining surge capacity. CMS floated a hospital stockpiling incentive program in 2023 but did not move forward with implementation.

Manufacturing Transparency and Early Warning

The FDA’s current early warning system for shortages depends substantially on voluntary manufacturer reporting under Section 506C of the FD&C Act. Manufacturers are required to report anticipated shortages of critical drugs, but the reporting threshold and timing requirements are imprecise. The Intas example — where FDA inspection findings from November 2022 did not translate into a public shortage declaration until February 2023 — illustrates the gap.

A mandatory and granular reporting system, requiring disclosure of inventory levels, qualified supplier count, API source geography, and facility inspection status for drugs on a defined essential medicine list, would give the FDA and hospital systems the visibility to build buffer stock before shortages materialize. Several European countries, including France and Germany, maintain mandatory supply notification systems with shorter reporting windows. The U.S. does not.

503B Compounding as a Shortage Bridge

During active shortages, hospital-based 503B outsourcing facilities — which operate under FDA oversight and can produce compounded sterile drug products for identified patient populations — have served as a partial bridge supply. The FDA has exercised enforcement discretion during shortages to permit 503B production of shortage products whose compounding would ordinarily be restricted.

503B compounding is not a systemic solution. It is expensive, capacity-constrained, and appropriate only for specific patient contexts. But in the absence of adequate supply from approved manufacturers, it fills a real gap. The policy environment around 503B has been volatile, with FDA periodically tightening enforcement in ways that reduce its utility as a shortage buffer at precisely the moments when it is most needed.

Key Takeaways

Durable resolution of the generic sterile injectable shortage problem requires pricing reform that floors essential drug prices at sustainable manufacturing cost, strategic API reserves backed by guaranteed purchase contracts, mandatory supply chain transparency reporting with short disclosure timelines, and a rationalized 503B compounding framework that functions as a genuine shortage bridge. None of these interventions is politically easy. All are technically feasible.

Investment Strategy

Pharma IP teams and portfolio managers evaluating the generic injectable space should track the FDA’s Quality Management Maturity program as a potential market structure variable. If QMM tiering is eventually linked to preferential GPO contracting or CMS reimbursement, manufacturers with Tier 1 or Tier 2 QMM ratings will carry a pricing premium over lower-rated competitors. That premium has not yet materialized in market pricing but is directionally likely as the policy environment evolves. Building QMM readiness into manufacturing investment decisions now positions assets for a regulatory environment that may, within five to ten years, reward quality differentiation rather than simply lowest cost.

The Weather Risk Layer: Natural Disasters as Shortage Multipliers

The structural price-and-concentration problem is the chronic condition of the generic supply chain. Natural disasters function as acute exacerbators on top of that chronic condition.

Hurricane Helene in September 2024 caused a major Baxter International IV fluid manufacturing facility in Marion, North Carolina to flood and halt production. Baxter’s North Cove plant produced approximately 60% of U.S. large-volume parenteral (LVP) IV fluids — basic saline bags, dextrose solutions, and Lactated Ringer’s. Within weeks of the flood, hospitals across the country implemented IV fluid conservation protocols. CNN data from October 2024 showed that some emergency departments were 50% less likely to administer IV fluids to appropriate patients than they had been before the disruption.

The Baxter LVP shortage is distinct from the generic pricing problem — Baxter is a branded medical products company, not a generic manufacturer, and IV bags are not subject to ANDA competition. But the underlying structural issue is the same: extreme geographic concentration of production of a medically critical product with no meaningful surge capacity and no strategic reserve.

Hurricane Katrina, Hurricane Harvey, and winter storm Uri — which knocked offline a Pfizer sterile injectables plant in McPherson, Kansas in February 2021 — have all produced similar short-term shortage spikes for specific sterile products. The pattern is consistent: a concentrated manufacturing base with no slack converts any regional weather event into a national shortage.

What Analysts Should Track in 2025-2026

The regulatory and market environment for generic sterile injectables is more active than at any point since the 2011-2013 shortage wave that prompted Congress to pass the FDA Safety and Innovation Act. Several variables will determine whether the trajectory improves or deteriorates.

The Trump administration’s proposed 200% pharmaceutical tariff on imported drugs — which ASHP and multiple health system associations are monitoring closely — could add significant cost pressure to generic manufacturers whose API supply is sourced from India or China. For shortage-prone drugs where the supplier base is already thin, tariff-driven cost increases without corresponding price relief from GPO contracts would accelerate manufacturer exits. The tariff question is distinct from the existing DPA investment narrative; it could undercut the supply resilience goal that the DPA investments were designed to support.

The FDA’s QMM program, which is voluntary as of 2026, is the regulatory initiative most likely to create differentiation among generic injectable manufacturers. If CMS links QMM certification to favorable reimbursement — a step that has been discussed but not implemented — the market dynamic changes meaningfully. Manufacturers that have invested in quality infrastructure will command a price premium. Manufacturers that have competed on price alone will face a structural disadvantage.

The FTC and HHS investigation into GPO and wholesaler practices, launched in February 2024, has not yet produced enforcement actions or proposed rulemaking as of early 2026. Its output — whether it is a consent order, proposed GPO transparency rules, or simply a report — will signal whether the federal government is prepared to address the market structure problem directly or continue with capital-investment approaches that do not alter price dynamics.

Rising Pharmaceuticals’ Decatur facility reactivation is a practical near-term data point. If the facility passes FDA inspection and returns shortage products to the market at commercially viable prices, it demonstrates that the distressed facility acquisition model works. If Rising encounters the same margin compression that collapsed Akorn, the lesson is that the problem has not changed — just the name on the door.

What Hospitals and Health System Pharmacy Teams Can Do Now

Hospital pharmacy leadership cannot wait for structural policy reform. The shortage environment as it exists today requires active management against a fragile supply baseline.

Shortage-prone drugs should be on formulary with dual-contracted supplier status — two GPO-contracted manufacturers at minimum, verified as separate manufacturing sites. A second contract with the same manufacturer at a different facility provides less protection than the contract language suggests. Formulary committees should require disclosure of primary API source geography and number of qualified API suppliers as part of new generic product contracting.

Buffer inventory policies for high-shortage-risk products — particularly sterile injectables in the CNS, antimicrobial, and oncology categories — have been advocated by ASHP for years. The practical constraint is carrying cost and expiry management for low-cost, perishable injectable products. CMS’s proposed but abandoned hospital stockpiling incentive would have offset this cost. In the absence of federal support, health systems that can absorb the carrying cost of four-to-six weeks of buffer inventory for their highest-shortage-risk products will be materially better positioned during future disruptions than those that cannot.

Therapeutic substitution protocols for shortage-period management — pre-approved by pharmacy and therapeutics committees, with defined clinical decision rules — reduce the time-to-substitution when a shortage hits. University of Utah Health’s infrastructure for shortage response, which includes real-time shortage monitoring, protocol libraries, and a dedicated shortage management team, is the model. Most health systems do not have that infrastructure. Building it is lower-cost than managing shortages reactively.

Conclusion: The Economics Have Not Changed

Every feature of the current generic drug shortage crisis — the price collapse, the single-source concentration, the facility failures, the clinical consequences — was described in the FDA’s 2019 report on drug shortage root causes and potential solutions. The 2011 shortage wave produced legislation. The 2019 FDA report produced analysis. The 2023-2024 shortage peak, driven by Akorn’s collapse and the Intas cisplatin failure, has produced DPA investments, FTC investigations, and Senate white papers.

The economics have not changed. A sterile injectable generic that sells for $1.50 per unit in a winner-take-most GPO contract cannot sustain the capital investment and quality infrastructure that its manufacturing requires. Until the pricing signal reflects the true cost of compliant sterile manufacturing — through floors, guaranteed purchase contracts, or quality-linked reimbursement — the market will continue to produce the outcomes it has reliably produced for two decades.

The question for pharma IP teams, portfolio managers, and R&D leads is not whether the next Akorn will happen. It is which product, which facility, and which hospital system bears the cost when it does.