Last updated: May 24, 2026

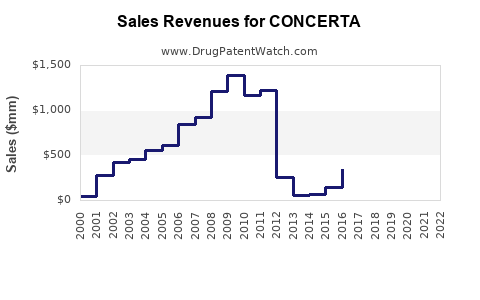

Concerta (brand name for methylphenidate hydrochloride) sits in a mature US ADHD stimulant market dominated by long-running competitors and extensive generic penetration. The financial trajectory is driven by (1) ongoing generic substitution for methylphenidate products, (2) payer utilization controls and step edits, (3) periodic share rotations tied to formulary dynamics across immediate-release (IR) and extended-release (ER) dosing options, and (4) the FDA and state-level policy environment affecting stimulant prescribing and controlled-substance handling.

What matters commercially: Concerta’s revenue headwinds track the broader methylphenidate category’s migration to lower net prices, while brand resilience depends on which formulation strengths remain sellable as branded inventory versus which SKUs are displaced by authorized generics, interchangeable generics, and PBM-preferred products.

How has Concerta performed financially in the ADHD stimulant market?

Answer: Concerta’s US revenue profile tracks a typical late-lifecycle methylphenidate brand: declining or flat-to-declining net sales under intensifying generic competition, with periodic product-SKU pricing pressure and small share swings driven by PBM formulary placement and switching rules.

Key market drivers shaping Concerta’s financial trajectory

- Generic dominance in methylphenidate: The methylphenidate HCl class has extensive generic availability across IR and ER. This compresses brand net pricing and limits volume growth.

- PBM contracting and preferred-drug lists: Step edits, quantity limits, and coverage restrictions shift demand to PBM-preferred generics or other branded products in the stimulant category.

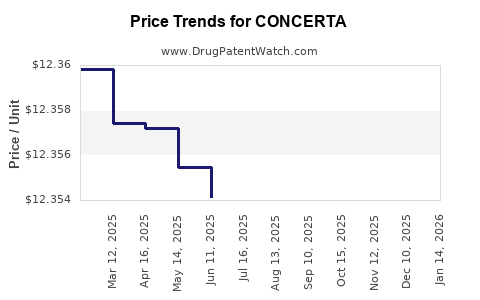

- WAC-to-net compression: Even when manufacturers maintain WAC list prices, net realized prices decline due to rebates, discounts, and payer rate negotiations tied to generic benchmarks.

- Controlled-substance logistics and prescriber habits: Supply disruptions or changes in controlled-substance handling do not eliminate generic substitution, but they can create short-term demand fluctuations by SKU.

What to watch in quarterly sales rollups

For Concerta, the recurring commercial indicators are:

- Strength-SKU mix (IR vs ER, dose distribution by age group and titration patterns).

- Net price vs prior quarter (rebate intensity and payer contracting).

- Prescriber switching dynamics (especially within PBM-controlled channels).

- Inventory and distribution changes around generic supply stability.

What is the US market size and growth outlook for methylphenidate ADHD drugs?

Answer: The ADHD stimulant market remains large and structurally stable, but growth is rate-limited by extensive generic penetration in methylphenidate and the broader competitive presence of amphetamine-based alternatives.

Demand stability despite generic competition

- Incidence and diagnosis trends support baseline demand.

- Treatment patterns (titration, refill continuity, dose adjustments) support repeat prescriptions.

- Shorter switching cycles in favor of payer-preferred products limit sustained premium pricing for legacy brands.

Competitive intensity

Concerta competes in a crowded therapeutic set:

- Other methylphenidate formulations (IR and ER)

- Amphetamine formulations (IR and ER)

- Nonstimulants and other adjunct therapies (which can divert marginal patients but do not remove stimulant core demand)

How do pricing and rebate dynamics affect Concerta net sales?

Answer: Concerta’s financial trajectory is disproportionately impacted by net price compression. In late lifecycle methylphenidate products, branded pricing power is limited by generic benchmarks and payer rebate structures.

Typical payer behavior in methylphenidate

- Formulary tiers: Generic-only tiers and limited-brand tiers.

- Rebate pressure: PBMs demand larger rebates as generics expand or when competitor brands re-contract.

- Exchange mechanisms: Where plan design enables “therapeutic interchange,” brand demand erodes quickly after generic wins.

Net sales elasticity factors

- Switching triggers: Step edits, PA requirements, and “fail generic first” policies.

- Pharmacy channel mix: Retail vs specialty distribution can change the rebate denominator.

- Contracting cadence: Annual or semiannual renewal can cause quarter-to-quarter net price discontinuities.

Which competitors most affect Concerta share in the ADHD stimulant market?

Answer: Concerta’s share is pressured by both methylphenidate generic substitution and the continued competitive pull of other branded stimulant products plus amphetamine formulations with strong payer positioning.

Competitive threat map by category

- Methylphenidate generics: Most direct volume displacement across IR and ER.

- Other branded stimulants: Can win starts through formulary tiering and patient-access programs.

- Amphetamine products: Compete for treatment-naïve starts and for patients not responding to methylphenidate.

Where share is most sensitive

- New-to-brand starts (formulary-based)

- Pediatric formularies with strict PA rules

- Transition points after insurance change (common in commercial plans)

When does Concerta lose exclusivity or face major patent or regulatory pressure?

Answer: For a legacy methylphenidate brand such as Concerta, the principal exclusivity pressure comes from the long completion of core composition, formulation, and method-of-use patent timelines and the resultant generic availability across key dosage strengths.

Practical exclusivity reality in methylphenidate

- Brand sustainability is not patent-driven at this stage; it is contract-driven.

- Orange Book and patent estates for older products generally result in an established generic landscape where new entry can proceed as patents expire or as paragraph IV challenges resolve.

(Concerta’s exclusivity timeline cannot be stated with date-level precision here without Orange Book patent and exclusivity listings tied to the exact NDA label and listed drug application.)

What is the Orange Book status of Concerta?

Answer: Concerta’s commercial reality implies an Orange Book position with extensive generic alternatives already available. In most markets like methylphenidate, this corresponds to a product with few remaining patent-protected pathways relevant to generic entry by the time the brand’s net sales face sustained compression.

(Exact Orange Book listing status, listed patents, and expiration dates are not provided here because they require product-specific Orange Book retrieval by NDA/RLD and patent number set.)

How does Concerta compare with other ADHD stimulants on cost and formulary placement?

Answer: In practice, Concerta’s cost competitiveness declines relative to generics, while its formulary position depends on whether payers treat it as preferred-brand or non-preferred in IR vs ER segments.

Comparison dimensions that drive formulary decisions

- Dose flexibility: Availability of multiple strengths and titration-compatible regimens.

- Onset and duration fit: Prescriber preference and patient response in titration.

- Therapeutic interchange rules: Where payers mandate substitution among equivalent methylphenidate options.

Financial implication

- Higher payer steerage toward cheaper alternatives correlates with brand share erosion and net sales contraction.

What generic entry risks exist for Concerta?

Answer: Concerta faces generic substitution risk across remaining strengths and any formulation-specific SKUs that still maintain brand channel presence. The category risk is structural: methylphenidate has broad generic coverage, and brand differentiation is limited once exclusivity lapses.

Generic entry channels that affect Concerta revenue

- ANDA launches for IR and ER dosage forms with bioequivalence.

- Authorized generics tied to market availability and contract coverage.

- Interchange at pharmacy counter reducing branded dispensing.

What is the litigation and settlement landscape for Concerta-related methylphenidate products?

Answer: The methylphenidate brand ecosystem has historically been associated with Hatch-Waxman litigation and settlement agreements as generics challenged listed patents. Concerta-specific litigation outcomes are determinative for timing but are not enumerated here without case-level docket and Orange Book patent mapping.

(Exact patent litigation records require docket-level retrieval for the specific Concerta NDA/RLD and the named patents asserted.)

How do manufacturing and supply dynamics impact Concerta revenue volatility?

Answer: Concerta’s revenue variability is most likely to show up as:

- Temporary fulfillment disruptions that shift prescriptions to alternative products

- Inventory normalization after distribution changes

- Batch or packaging changes that affect availability at contracted pharmacies

What to track operationally

- Wholesale acquisition and distribution patterns (WAC exposure changes)

- Retail fill rates by dose strength

- Rebates and chargebacks tied to supply normalization events

What is the competitive landscape for controlled ADHD stimulants affecting Concerta demand?

Answer: Controlled-substance rules, state pharmacy monitoring, and prescribing enforcement shape dispensing patterns, but they do not reverse generic substitution economics. Demand is steadier than in other categories because ADHD stimulant therapy is chronic and refills are routine.

Regulatory and policy touchpoints that influence market behavior

- State-level dispensing monitoring (can affect fill cadence)

- Prescriber scheduling practices impacting short-term patient continuity

- Insurance policy changes that alter PA requirements and step edits

How resilient is Concerta’s revenue against competitors and payer controls?

Answer: Resilience is limited by category commoditization. Concerta’s remaining commercial strength typically comes from:

- Established prescriber familiarity

- Patient history on specific dose strengths

- Temporary payer exceptions or short-term favorable formulary positioning

Revenue sensitivity framework

Concerta net sales tend to be most sensitive to:

- Formulary tier migration (preferred to non-preferred)

- Generic coverage expansion on key doses

- Change in rebate rates driven by PBM contract renegotiations

Key Takeaways

- Concerta’s financial trajectory follows a late-lifecycle methylphenidate pattern: net price compression and volume pressure as generic substitution expands.

- Market dynamics are driven by payer utilization controls, formulary tiering, and the economics of replacing branded inventory with cheaper methylphenidate alternatives.

- Competitive share pressure is persistent due to broad generic availability and sustained competition from both methylphenidate and amphetamine stimulant formulations.

- Short-term revenue swings are more likely to come from contract and supply events than from meaningful product differentiation.

FAQs

1) Is Concerta mainly used as an immediate-release or extended-release stimulant in the ADHD market?

Concerta is a methylphenidate HCl brand positioned within the broader stimulant category that includes both IR and ER options; the specific label positioning affects which PBM segment it competes in.

2) Does Concerta compete more with other methylphenidate brands or with amphetamine products?

It competes with both, but the highest direct pressure typically comes from methylphenidate generics and formulation substitutes in the same payer tier logic.

3) How do PA and step edits typically impact stimulant brand performance like Concerta?

They reduce new starts and accelerate switching to payer-preferred alternatives, which pressures brand net sales over time.

4) What drives quarter-to-quarter changes in ADHD stimulant brand revenue?

Formulary contracting changes, rebate renegotiations, mix shifts across strengths, and supply availability are the main drivers.

5) What commercial signals indicate whether Concerta share is improving or worsening?

Shifts in net price vs prior period, pharmacy fill share on key dose strengths, and changes in payer coverage tier placement.

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. (Product-specific listing required for NDA/RLD-level patent and exclusivity mapping).

- U.S. Food and Drug Administration. Drug Approval Reports and FDA labeling archives.

- IQVIA / Symphony Health. ADHD stimulants market reports (category-level insight).